Last week, the Croatian Government announced a new package of anti-inflationary measures, with the stated aim of reducing inflation in the period ahead. In this blog, we review the potential impact of these measures on the Croatian economy. We try to answer whether they will be successful, and we show why their impact on the Croatian blue chips that could be affected is, at present, almost impossible to measure.

The measures can be split into three categories: A) budget discipline, B) administrative prices, and C) tax-related measures, and in particular, C1, a measure for an extra-profit tax on “disproportionately high profit margins.”

We will start with measure C, and more specifically, the aforementioned C1 measure. According to the proposal, it aims to tax the part of a company’s EBT margin that sits above its own three-year average, adjusted by a 15% “tolerance.” The measure targets medium and large enterprises in Croatia that generate 50% or more of their revenue on the territory of Croatia.

This would apply to 1,740 medium and large enterprises, but again, only those that generate 50% or more of their revenue within Croatia. The qualifying thresholds are three:

- Total assets of EUR 25m or more, in 2026.

- Net (sales) revenue of EUR 50m or more, in 2026.

- An average of 250 or more employees in 2026.

Under the Accounting Act, the classification works as follows. A medium-sized enterprise is one that does not exceed the threshold indicators in two of these three conditions. A large enterprise is one that exceeds the threshold indicators in at least two of the three. In other words, a company becomes large once it crosses the limits on at least two of the three, while a company that stays below the limits on two of them is classified as medium-sized.

A practical example of the extra profit tax would be the following. Take a company that meets the conditions and has an average EBT margin of 10% over 2023 to 2025 (for instance, 9% in 2023, 10% in 2024, and 11% in 2025). The new proposal applies a 15% “productivity tolerance” on top of that average. The tolerance is 15% of the margin, not 15 percentage points, so it adds 1.5 percentage points to the 10% average. This company’s EBT margin could therefore reach 11.5% before any extra profit tax applies, and only the part above 11.5% would be taxed, at a 50% rate.

From the Government’s perspective, the measure appears aimed at discouraging excessive margin expansion in sectors where price increases may have gone beyond cost pressures. In theory, such a mechanism could reduce incentives for opportunistic price setting and support fiscal revenues without directly raising broad-based consumption taxes. However, distinguishing genuine excess margins from productivity, investment, accounting effects, or sector-specific cost normalization is difficult in practice.

In our calculations, we tried to project how this would hit the Croatian blue chips, but we found the task is highly uncertain with publicly available data, for several reasons. First, the taxpayers are the individual legal entities resident in Croatia, so the Tax Office would look at each legal entity rather than the consolidated, group, or holding results. That makes the exercise hard, because it requires a projection of 2026 revenue (for the “more than 50% of revenue in Croatia” test) and of 2026 EBT for each individual legal entity, rather than for the published group results. We note that this is our reading of how the measure is expected to work; the announcement has not explicitly confirmed the consolidated-versus-unconsolidated treatment.

We say published results, because there is a difference between what a company shows in its P&L and what it submits to the tax office. The latter usually reflects deferred tax, investment reliefs, subsidies, and a host of other items to which we do not have access. Even if those figures were published, it is hard to define what is meant by “more than 50% of revenue on the territory of Croatia”. The only hint we have of this are the communications from Government officials, describing it as a measure to protect our exporters.

But even there, it is hard to define what an “exporter” in this case means. Take the hospitality industry as an example. Many hotels and camps earn most of their revenue on the territory of Croatia, yet most of that revenue comes from foreign tax residents, namely tourists. Tourism is itself defined as an export of services, so it isn’t clear how this sector would be treated. Our reading is that hospitality companies would be affected if they met the conditions, because the revenue is generated in the territory of Croatia, but further clarification could clear this out decisively.

So which companies would actually be affected? In the proposal itself, it would be the companies that benefited the most during the period of high inflation. Looking at the largest companies in Croatia, this would mostly relate to sectors such as energy and energy retail, grocery and FMCG retail, tourism and hospitality, and potentially wholesalers, such as pharmaceutical distribution.

The measure’s quantifiable impact itself is unclear, however. As a point of comparison, in 2022 and 2023, when the previous extra-profit tax was introduced, the proposal was explicit about the amount it aimed to raise: HRK 1.5bn, or about EUR 200m. By the later statements made by Government officials, the proposal was able to raise roughly EUR 230m to EUR 236m, depending on the source.

We say unclear because, this time, the proposal has no quantifiable target it aims to raise. The three-year average EBT comparison is also imperfect, and it ignores two important facts. First, margins during that period were, for many sectors, suppressed precisely because of higher inflation and input costs. Inflation has trended down only over the last year to a year and a half, with a recent uptick driven by higher energy prices connected to the war in the Middle East. With a new inflation wave starting in the country, companies are being affected precisely at a time when their situation is stabilizing. This does not take away from the fact that some companies and sectors did take advantage of the situation, passing higher costs through to consumers while widening their margins. However, this does not appear to have been uniform across sectors or companies.

Second, this way of measuring margins does not distinguish why margins grew. Did they grow because companies benefited from the situation, or because they invested in their production, their employees, and their workflow, and so became more profitable? This measure may help the Government in the short term, but it may be counterproductive over the medium to long term. In essence, this could be seen by the companies as a signal that any extra improvement in their margins, whatever its source, could be taxed at very high rates in the future. This makes the future investment environment uncertain, which could stifle investment, one of the key drivers of future economic growth.

On its own, it’s uncertain whether the measure will have a meaningful impact on inflation, due to several dynamics.

Here, we have to separate demand-side and supply-side inflation. On the supply side, inflation has been driven mostly by external factors outside the control of both companies and the Government. If energy commodity prices rise, the Government can cap certain energy items, such as the prices of oil and gas derivatives, but it cannot do so indefinitely. Someone has to bear the cost of higher prices, whether companies, consumers, or the Government through its subsidies. The same holds for food. If the prices of coffee, cocoa, sugar, wheat, or similar items rise, the cost for food producers rises automatically, especially since Croatia imports so much of its food commodities. Services follow the same logic. External factors also shape tourism-related services. If demand for hotels and private accommodation continues, while providers face higher input costs, including wage inflation that is itself supported by minimum-wage increases, then those providers are unlikely to hold their prices flat.

On the demand side of inflation, the Government does have some control. Since public servants make up such a large part of the overall workforce, the Government has direct control over their wage increases. The 2024 wage increases in the public sector (30% on average) directly supported the demand-side inflation. This was recognized in the newest measure package, but as well see below, it isn’t clear how far the measures will go. The subsidies and income support to households also feed into inflation, and that money does have to come from somewhere. The minimum wage increases that we have seen each year also directly feed into higher consumption, one of the key drivers of demand-side inflation.

Now, with inflation being elevated, workers should be able to receive more, especially in the lower-paid tiers; however, that growth has to follow productivity growth, not just increases which affect each sector, no matter whether improvements in productivity were made or not. Another thing also influencing the demand-side inflation, which the Government has little to no control over are the foreign tourist inflows, as they usually come from countries with higher budgets than domestic tourists, and they are more inelastic to price increases of goods and services when in the country.

Finally, because the tax looks at 2026 figures, companies have ample time to influence their margins through accounting policy, for example, by increasing investment or depreciation, raising wages, or any of the many other available levers. At the same time, if inflation falls during 2026 and into 2027, as the proposal’s estimates suggest, then the measure affects companies at a moment when they have little influence over prices, exactly due to those external pressures.

This is visible in the way that the proposal is presented. It says, taking the other measures into account, that the fall in inflation rests mostly on the normalization of energy prices in 2026, something the Government does not control, and which will not be possible if the conflict in the Middle East escalates. For 2027, it aims to lower inflation further through the “base effect,” partly through administrative price restrictions (more on this below) and partly through the base effect of high energy prices.

Two distinct things are at work here, and they are worth separating. The first is the statistical base effect: high energy readings in 2026 make the YoY comparison in 2027 softer, which mechanically lowers the 2027 inflation rate. The second is the price level. Even if inflation falls to a 2% rate in 2027, prices still rise a further 2% on top of an already elevated level. The earlier increases are not reversed; they are built upon. So a low headline rate does not mean relief, because the cumulative jump in the price level stays locked in.

Furthermore, there is a deeper point here. Over the last couple of years, Croatia’s budget has been running in a widening deficit, one that is expected to widen even further, even if Croatia is able to collect more tax revenue each year. This raises the question of whether, besides inflation containment, fiscal consolidation is also an important objective.

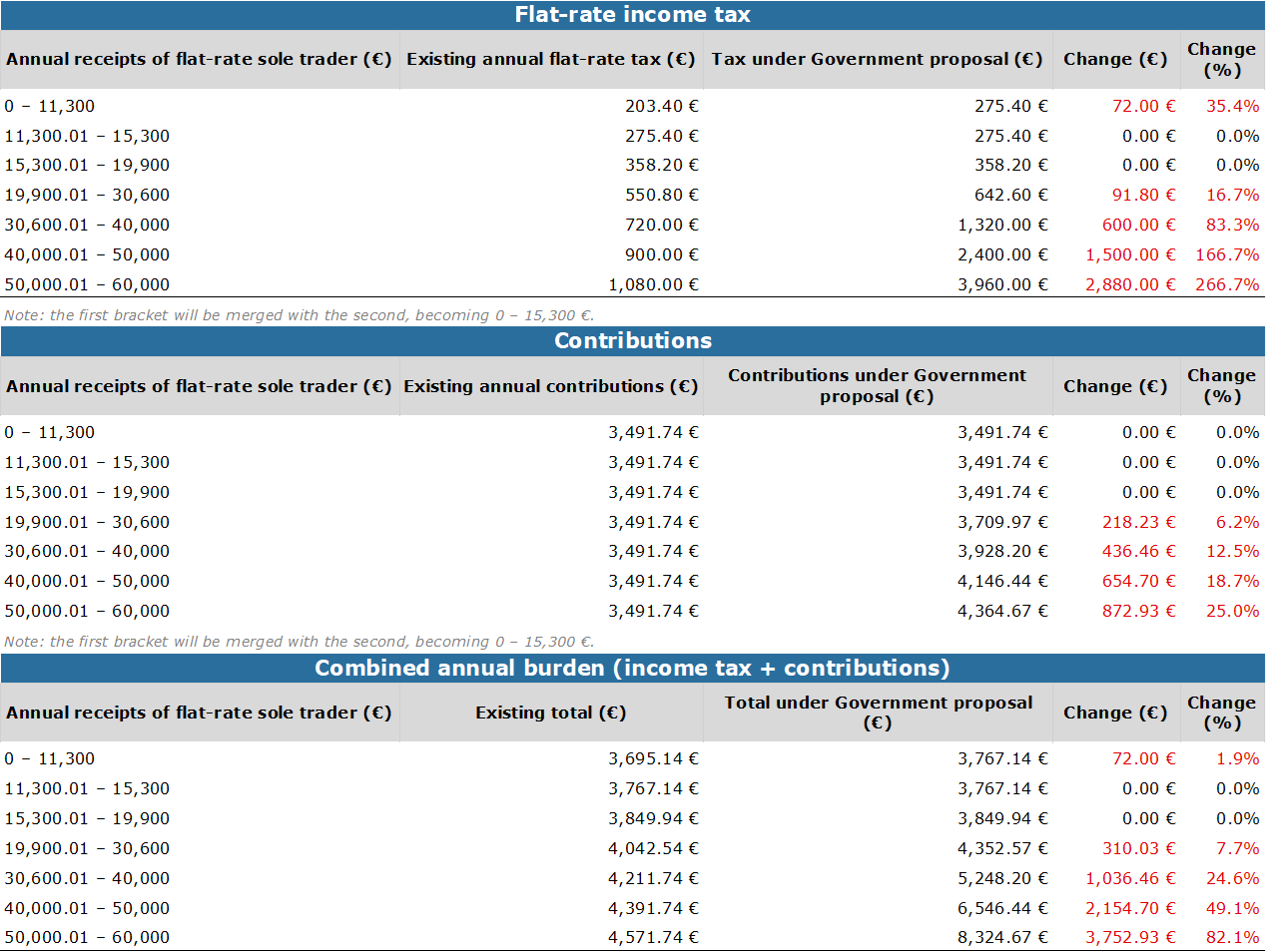

That brings us to the rest of the C measures. Measure C2 concerns “obrtnici” (sole traders), and in particular the “paušalni obrt” (flat-rate sole trader). This was one of the more attractive business forms in Croatia, because it allowed individuals to start a business at relatively low costs and with relatively low administrative overhead. According to the Croatian Tax Office, the number of these businesses rose from about 27.6k in 2017 to about 101.6k in 2025, an increase of roughly 268%, while the number of other company types fell from 72.7k to 62.6k, a drop of about 14%.

The proposed measures contain an argument that says this is true, at least partially, as part of that increase was driven by people using this system inappropriately. However, in the proposal itself, it isn’t clear who did this or by what amount. With the announced measures, the proposal may not fully address the underlying issue, as the measure applies broadly across this business form.

While this is bringing the overall costs for these types of businesses closer to that of other business types, it does not take into account that these types of businesses also face higher costs and have downsides compared to being directly employed. These include being directly responsible for the well-being of the sole-trader business with your own assets as a physical person, not being protected by the Labour Act, which includes items such as no notice period, no protection against dismissal, no severance, no guaranteed minimum paid annual leave, and no wage-protection rules. Furthermore, the system itself (lump-sum trader) is limited to EUR 60k of annual revenue, real business costs are non-deductible, as the scheme assumes a fixed recognized-expense percentage, so if the true costs are high, those businesses are taxed on a base that ignores these factors, and the new proposal isn’t addressing this issue, as it’s cutting that recognized-expense share. On top of that, fiscalization, issuing invoices, keeping the prescribed records, and making monthly contribution payments are also required. In essence, the situation here isn’t black and white, as switching to this type of business from regular employment does present a trade-off.

Changes to the taxes and contributions for flat-rate sole traders in Croatia (2026 proposal vs. previous regulation)*

Source: Croatian Tax Office, InterCapital Research

*Effective from 1st January 2027

With this measure, the Government aims to collect an additional EUR 60m per year. Measure C3 also concerns flat-rate taxation, in this case for the tourism industry, and raises taxes for accommodation providers.

Changes to the flat-rate tax by level of regional tourism development (EUR)*

Source: Ministry of Finance, InterCapital Research

*Effective from 1st January 2027

This measure raises taxes on accommodation providers, especially in the most developed categories. It lifts the lower bound of the range by 50% in category I and by about 43% in category II, while categories III and IV/0 are unchanged.

Lastly, measure C4 abolishes income tax on pensions. The proposal targets approx. 541k pensioners, at a cost of about EUR 180m. This measure is positive and needed for the group most exposed to inflation. But the money has to come from somewhere; even including the EUR 60m gained from higher taxes and contributions on flat-rate sole traders, around EUR 120m has to be found somewhere to fund it.

Returning to the A measures, budget discipline, these are split into A1 and A2. A1 covers budget savings of about EUR 1.1bn, which the Government aims to achieve through material costs, financial costs, transfers within the general budget, and improvements to investment spending. Another EUR 200m would be saved by re-routing financing onto EU sources. In total, EUR 1.3bn, or 1.4% of GDP is expected to be saved by this measure. A2, meanwhile, concerns the collective agreements of state-owned enterprises, under which “material rights” (in practice, higher wages) will not increase until Q1 2027. The second part of A2 keeps all social benefits at current levels until that same Q1 2027.

Budget discipline is the only measure here that is genuinely anti-inflationary, because higher Government spending is one of the drivers of the widening budget deficit, which has to be contained. It is good that in the new proposal, it has been recognized that the higher spending cannot be kept indefinitely, and this represents a positive step in the right direction. The second part of the measure, the freezing of wage increases, is hard to quantify in its impact. The Government has already agreed on wage increases with the trade unions, raising the base by 1% from 1 April 2026, a further 1% from 1 August 2026, and another 1% from December 2026. In other words, the only real “freeze” would fall in Q1 2027, where no agreement has yet been reached.

Finally, the B measures concern administrative prices, defined as prices that the Government or public bodies can set in full or in part, rather than prices set by the market. Here, the Government pledges to freeze any increases until Q1 2027. This would slow price growth until that point, but it remains to be seen how much it actually influences inflation.

In summary, the measures stand as follows. The A measures will partly affect inflation through lower Government spending, while partly having a minimal or unknown impact, as the wage increases were already signed. The effect of the B measures is unknown at the moment. The C measures are hard to quantify in full. Higher taxes and contributions on flat-rate sole traders will help fill the budget, but they will also weigh on businesses, which could lead to more closures and reduced economic activity. The effect of the extra-profit-margin tax is the hardest to quantify, for the many reasons set out above. Even so, it could have an impact on future investments, thus its medium-to-long-term impact could be negative. The abolition of income tax on pensions, while needed for pensioners, is negative for the budget. The higher flat-rate tax on tourism providers, while designated as needed, does not take into account that inflation and higher input costs are also affecting them. At the same time, Government officials made requests to the tourism providers to reduce prices. In other words, the new proposal appears to place additional pressure on a sector already facing rising input costs, while at the same time, asking the providers in the sector to limit their revenue growth, and it is not known whether the providers will be able to support that.

Besides the new measures, the Government also kept the subsidies on gas, electricity, and fuel, kept the price limits on 100 different products and product categories, and kept the reduced VAT on many products.

So what do we make of this?

In general, since Croatia is part of the euro area and cannot influence its currency directly, monetary policy is off the table. That leaves fiscal policy, which is what we see here. It is positive that the Government has started to work on the spending within its ministries and public bodies, as it can directly impact that while having a meaningful impact on inflation. Further measures such as these would represent more positive steps.

However, it would be good to introduce more measures and programs for entrepreneurs, such as reducing regulation or increasing support programs for them, as in the end, they are the ones driving the growth in economic activity, supporting higher employment rates, and in general, increasing innovation and the overall wealth level of the country. Will this happen? Previous track record on this is mixed, but if such measures are introduced, we could see even higher GDP growth rates than we did in the last couple of years.

It is important to differentiate the measures that support the demand side and those that influence the supply side. If higher support is given to the supply side, more products, services, etc. could be created/provided, which would not affect inflation but would raise overall living standards, especially if the industries involved are the higher-output ones. Lastly, as the external measures are mounting, it is hard to say how big of an impact the proposed measures will have on inflation moving forward.