The most important indicator last week was obviously US non-farm payrolls, which managed to deliver a significantly weaker print compared to market consensus. Yet yields went up – how can that be? Also, what do we expect from the new Croatian 5Y local bond placement this week? Read more in this brief research piece.

US June payroll figure crossed the wires on Thursday, July 02nd – one day earlier because Friday (July 03rd) was a bank holiday in the United States, designated for Independence Day observations. First of all, the headline figure was more than half below the consensus (57k reported vs. 115k consensus estimate). May’s figure was revised downward as well, and it’s also worth mentioning that the unemployment rate inched down slightly (from 4.3% in May to 4.2% in June) as more people left the labor market. The figure itself doesn’t tell much since the JOLTS report published a day earlier arrived at a 2Y high, saying enough about the strength of the US labor market. The knee jerk reaction to data was a shallow drop in yields, but these were subsequently reversed in the following trading session and Germany 10Y managed to pull about 3.5bps higher compared to values soon after the NFP print.

Shouldn’t yield move in the opposite direction after weaker than expected NFP prints (i.e. lower instead of higher)? Answer to this question might be traced in recent statements made by Kevin Warsh at Sintra forum. Warsh essentially reiterated his hawkishness based on giving inflation data higher priority and letting labor market take the back seat. This might have surprised FED observers since market consensus was that Kevin Warsh ought to be dovish, not hawkish – that is, agenda pushed by Donald Trump and his fiscal executive arm Scott Bessent focuses on lower yields. As usual in life, there’s more than meets the eye.

Donald Trump remembers quite well that it’s the inflation that helped him to remove the Democrats from essentially all levers of power – nevertheless, inflation is the sword that cuts both ways. So naturally, although White House desires lower FED fund rates and lower UST yields, Warsh’s first job will be to get the inflation figures down and prevent blue sweep in November.

Is it a bit too late since monetary policy works with a lag and they haven’t hiked interest rates at Warsh’s first FOMC meeting? We beg to differ – it’s not hikes that get yields higher; it’s the FED speak (i.e. communication), while hikes are merely tools to prop up the FED’s credibility (i.e. to prove that Washington is talking the talk and walking the walk). In the short term, Warsh can truly speak his way out of inflation, at least to a certain degree. In other words – hawk talks, the market walks (to higher yields). It seems slightly slower NFP data is merely noise, not a signal (that’s literally the essence of Sintra’s remarks).

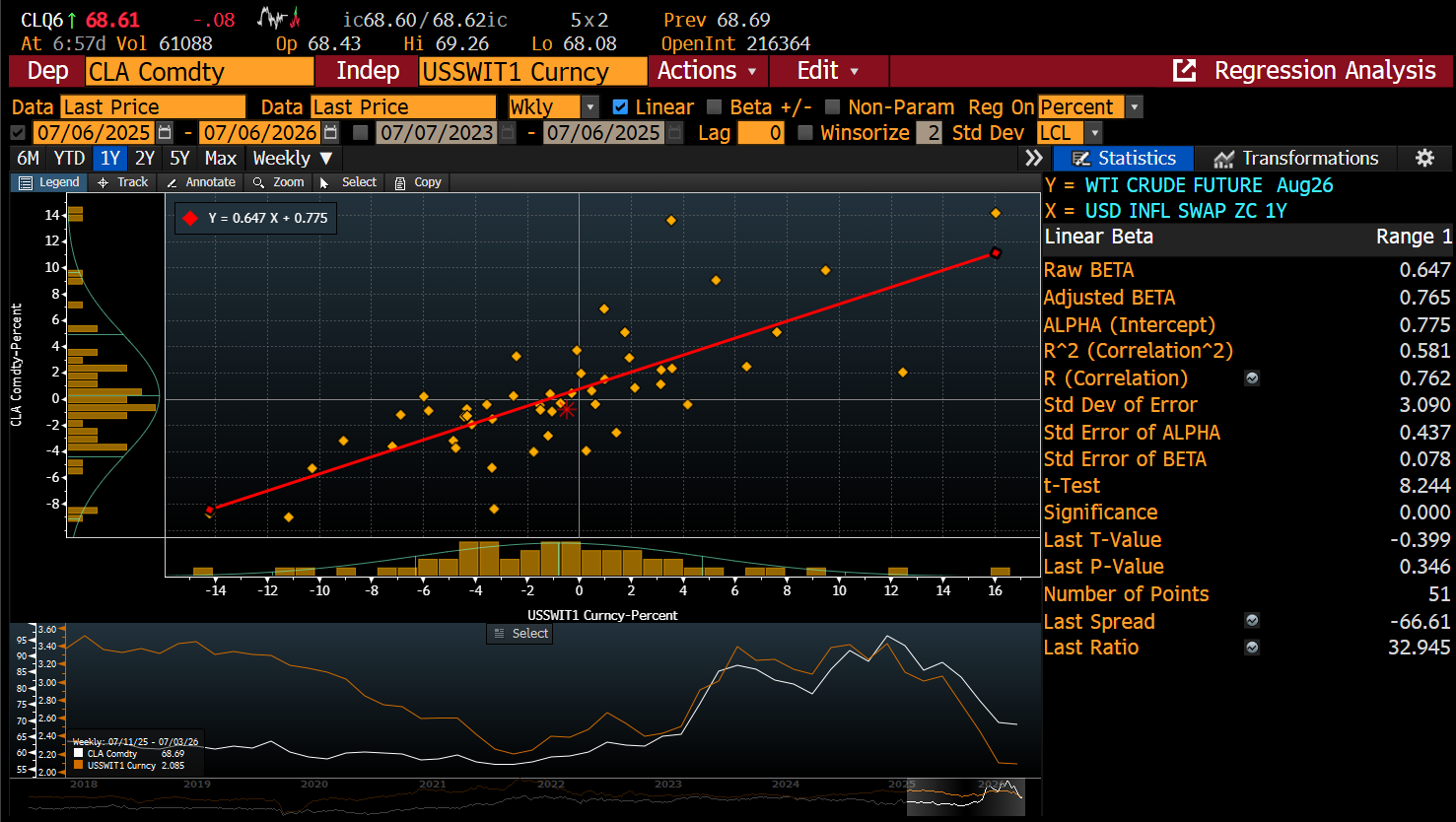

There are pockets of financial markets that might be thinking in the opposite direction. First of all, with Hormuz reopening and the resumption of tanker flows oil prices dropped sharply. Now, these prices are highly correlated with 1Y inflation swaps:

Notice that on a weekly basis, percentage changes in oil prices explain more than half of the variation of percentage changes of 1Y inflation swaps (R-squared = 0.581). This drop in price caused a sudden divergence between 1Y inflation swaps (2.085% today vs. 3.40% April 30th) and USD 2Y yields (4.13%). Be aware of the fact that the difference between the US 2Y yield and the 1Y inflation swap is currently in the 13th percentile (we used 10Y as the time frame). We subscribe to the view that this discrepancy could completely be assigned to hawkish FED. Moreover, if we are right about the purpose of this hawkishness (getting inflation figures in order before Americans head to the polls in November), then this FED speak might reverse its course after the elections move to the rear view. Back to the spread between US 2Y and 1Y inflation swap – something will have to give; since 1Y inflation swap is espoused to the oil price and with all that glut a rise in prices remains elusive, it’s quite likely that 1Y inflation swap might be anchored. Hence, the 2Y yield will have to drop lower, much lower. If the hawk from Washington can talk them up, he can surely talk them down as well.

Speaking about the Croatian local bond market, it’s worth bearing in mind that about 400mm EUR of CROATE 2.125 07/15/2026€ (RHMF-O-267E) will mature on July 15th. These would be refinanced with about 1bn EUR of new local 5Y bond that will probably be placed on Tuesday, July 07th (settlement date July 14th). We expect the yield to maturity to end up 5bps above the interpolated value between CROATI 1.5 06/17/2031€ andCROATI 2.875 04/22/2032€, and with July 14th, 2031 used as the maturity date of the new bond, we calculated 3.024% as the interpolated value, meaning that we expect YTM to get to 3.074% (=3.024%+0.05%). Banks will probably be quite interested in the new paper, and PFs+insurance companies are probably looking to invest the proceeds from the old paper in slightly higher duration (7Y/8Y is our educated guess).

Be mindful, be vigilant. The market never sleeps.