After yesterday’s ISM print, it’s becoming evident that the American economy is heading for a “Sully Sullenberger“-style soft landing. This scenario was in the cards, but vouches less rate cuts than expected in the previous quarter. Volatility is back and the markets are zig-zagging all over again in pursuit of something elusive: a sense of direction. How to trade the current regime? Find out in this brief research piece compiled by Ivan Dražetić, CFA and Josip Rimac.

Although published on April 1st, yesterday’s US ISM survey was no joke for bond vigilantes. While European investors were enjoying a day off, US players got another assurance that the American economy is going through a “Sully Sullenberger”-style soft landing, bringing three rate cuts into question. Let’s take it step by step. The headline ISM Manufacturing survey came in at 50.3, which is not just significantly above the consensus estimate (48.3), but also way above the last print (47.8) and therefore represents the best reading since September 2022. ISM Prices Paid also came way above the consensus estimate (55.8 versus 53.0), and so did ISM New Orders (51.4 versus 49.8). What does all this mean for the markets?

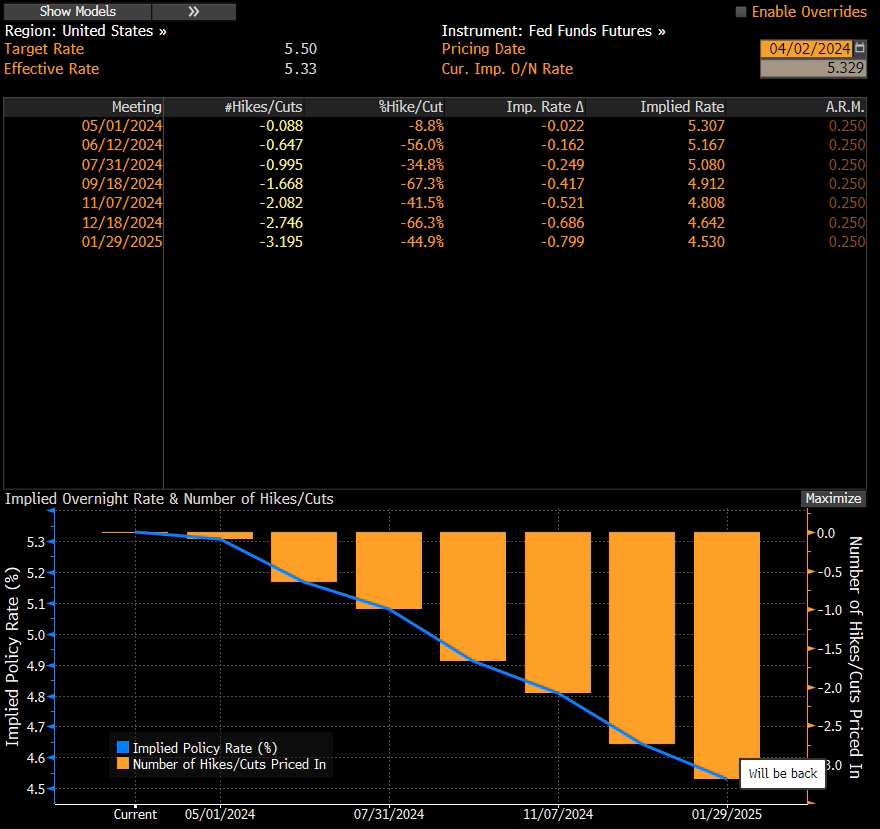

First of all, June rate cut is expected, but now it looks more like a coin toss with roughly 56% of probability:

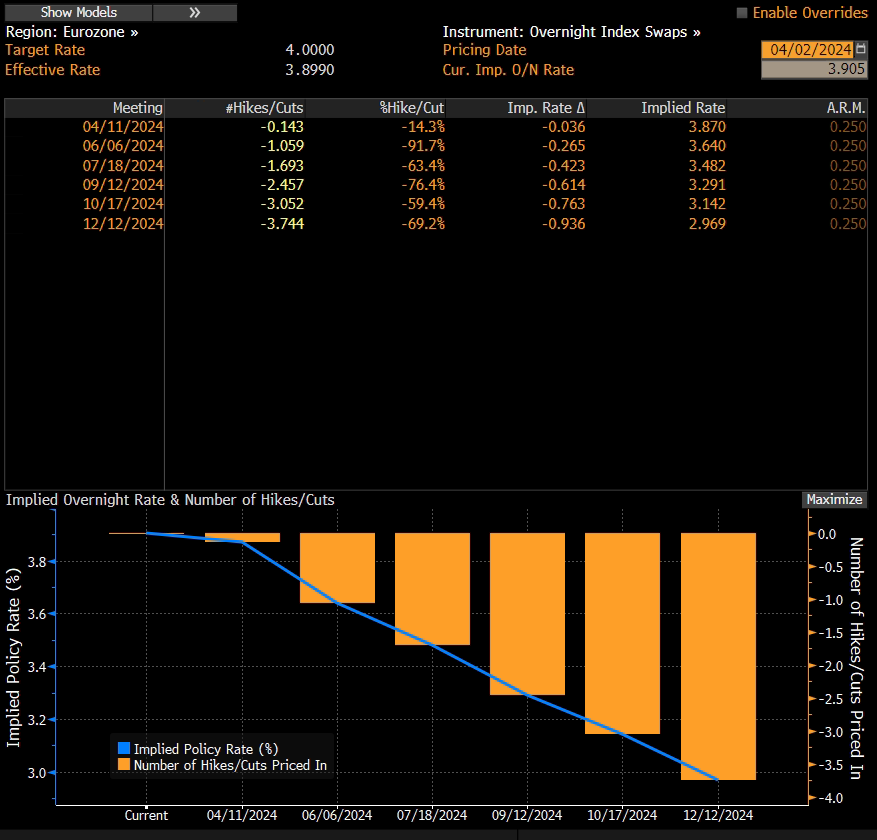

This essentially means that markets are questioning the prospects of three rate cuts this year (2.7 cuts are priced by the last FOMC meeting this year). This is clearly not in congruence with prospects in the euro area and since the ECB has a much different economic blueprint at its disposal, markets are still expecting a cut in June and about 3.6 cuts this year:

In other words, expectations are 2.7 cuts by EOY in US, 3.6 cuts in euro area and naturally, FX markets are selling EURUSD like there’s no tomorrow. ISM is regarded as soft data compared to employment figures and inflation, regarded as hard data. Nevertheless, predictive features of ISM are unquestionable and it’s quite likely that we can expect more strong labor reports and GDP readings. As a matter of fact, one of these readings might come in as soon as on Friday. Just to get a feeling for the market, the consensus estimate for the headline NFP figure due to be published this Friday (April 05th) are 203k (versus 275k in March), unemployment at 3.8% (versus 3.9% in March) and average hourly earnings at 4.1% YoY (versus 4.3% YoY in March). Just look at where the consensus estimate median is positioned and you can expect two things: low volatility on fixed income pre-NFP and surprises after the print.

Speaking about hard data, inflation prints in the US are sending a familiar dovish tune. In the last two months, both US and euro area inflation have proven to be more resistant than previously thought, mostly thanks to sticky service sector inflation. Prints from January and February, which both came in a bit higher than estimated, showed that the path towards the 2% inflation target entered the most challenging phase and that is curbing it down from 3% to 2%. In our last blog, we mentioned that we won’t be seeing first-rate cuts from FED nor ECB before meetings in June. But as time goes by and services inflation isn’t showing firm signs of yielding, we hear more and more often of cuts being pushed later in the year. FOMC voting member Christopher Waller said on Thursday that “there is no rush to lower interest rates” implying that recent economic data isn’t very optimistic in terms of curbing inflation. He later went on to say that inflation figures are disappointing and that he would like to see “at least a couple months of better inflation data” before cutting. The main reasons for this statement are a strong economy and a resilient labor market, which suggest to Waller that the Fed has more room to hold with the first cut.

By the end of February 2024, Croatian mutual funds’ NAV grew by 1% MoM, and 14.6% YoY, recording the largest increase since December 2021. This would mean that the funds’ NAV almost reached EUR 2.4bn, ending February at 2.39bn. Furthermore, if we compare it to the pre-COVID-19 maximum, mutual funds NAV is app. 22.7% lower.

In the latest report on the Croatian mutual funds released by the Croatian Financial Services Supervisory Agency, HANFA, we can see that the Croatian mutual funds recorded continued growth in February 2024. In fact, the mutual funds NAV amounted to EUR 2.39bn, increasing by 1% MoM, and 14.6% YoY, while compared to the pre-COVID-19 maximum, the NAV stands at 22.7% lower levels.

However, this represents a recovery, as the NAV has declined significantly after the start of the war in Ukraine and the subsequent macroeconomic and geopolitical developments. In fact, at one point the NAV was 36% lower than its pre-pandemic high.

To understand what drove the changes in the NAV in February, one should look at the two drivers of growth, i.e. the change in the value of underlying assets, and the net contributions into the funds. Looking at the net contributions first, during January 2024 they amounted to EUR 51.9m, (January 2023: EUR -26.4m), while on the trailing twelve months basis, they amounted to EUR 156.8m (January 2023 TTM: EUR -453.6m). In other words, as there was a large cash outflow in the same period last year, positive net inflows started to be recorded in April 2023, and have been recorded ever since.

This would mean that on a MoM basis, net contributions were actually the only driver of growth, as the MoM 1% increase (or EUR 23.2m) in absolute amounts, was lower than the EUR 51.9m of net contributions. On the other hand, on the YoY basis, net contributions constituted app. 51% of the growth in NAV.

Net contributions of the Croatian mutual funds (January 2021 – February 2024, EURm)

Source: HANFA, InterCapital Research

Moving on to the asset classes themselves, on the MoM basis, bonds recorded the largest change at EUR 31.7m, or 2.3%, followed by shares at EUR 15.2m, or 4%, and the money market holdings, at EUR 4.8m, or 8%. On the other hand, deposits and cash declined by EUR 6.96m, or 2%, while receivables decreased by EUR 6.95m, or 26%.

Meanwhile, on the YoY basis, the largest increase was recorded by bonds, at EUR 161.3m, or 12.9%, followed by shares at 85.5m, or 27.6%, and deposits and cash, at EUR 38.9m, or 12.9%. Receivables and investment funds also recorded increases, at EUR 15m and EUR 12.9m, respectively.

Total assets of the Croatian mutual funds (January 2015 – February 2024, EURm)

Source: HANFA, InterCapital Research

Looking at the current asset structure of the funds, bonds still make up the largest percentage, at 58%, representing an increase of 0.4 p.p. MoM, but a decrease of 1.13 p.p. YoY. Next up, we have shares at 16.2%, with growth of 0.37 p.p. MoM, and 1.59 p.p. YoY, as well as deposits and cash at 13.9%, with decreases of 0.51 p.p. MoM, and 0.26 p.p. YoY. One other noteworthy category to mention is the investment funds, which held 8.3% of the total, and which have decreased by 0.11 p.p. MoM, and 0.65 p.p. YoY.

Current AUM of Croatian mutual funds (% of the total, February 2024)

Source: HANFA, InterCapital Research

As we can see, there is still demand present for the Croatian mutual funds, and the majority of investments are still made into bonds, which given the current interest rates and yields on said bonds, makes a lot of sense. The mutual funds themselves have been on a path to recovery for a while now, and barring extraordinary events in the coming period, this development could continue.

Here you can find the dates for the upcoming events of the regional companies

| wdt_ID | Date | Ticker | Announcement | Country |

|---|---|---|---|---|

| 15 | 26.3.2024 | ATGR | Atlantic Grupa Supervisory Board Meeting | Croatia |

| 16 | 27.3.2024 | ATGR | Atlantic Grupa Supervisory Board Meeting | Croatia |

| 17 | 27.3.2024 | TEL | Transelectrica Annual 2023 results (OGSM material) | Romania |

| 18 | 28.3.2024 | TEL | Transelectrica Meeting for financial analysts, investment advisors, brokers and investors to present FY 2023 results | Romania |

| 19 | 28.3.2024 | H2O | Hidroelectrica financial results for 2023 - materials for Ordinary General Meeting of Shareholders | Romania |

| 20 | 29.3.2024 | ATGR | Atlantic Grupa FY 2023 Audited Report | Croatia |

| 21 | 29.3.2024 | ZVTG | Triglav FY 2023 Audited Report | Slovenia |

| 22 | 29.3.2024 | H2O | Hidroelectrica investor and analyst conference call for FY 2023 financial results presentation | Romania |

Due to the nature of these events, they are subject to change (might be postponed or canceled).