After yesterday’s ISM print, it’s becoming evident that the American economy is heading for a “Sully Sullenberger“-style soft landing. This scenario was in the cards, but vouches less rate cuts than expected in the previous quarter. Volatility is back and the markets are zig-zagging all over again in pursuit of something elusive: a sense of direction. How to trade the current regime? Find out in this brief research piece compiled by Ivan Dražetić, CFA and Josip Rimac.

Although published on April 1st, yesterday’s US ISM survey was no joke for bond vigilantes. While European investors were enjoying a day off, US players got another assurance that the American economy is going through a “Sully Sullenberger”-style soft landing, bringing three rate cuts into question. Let’s take it step by step. The headline ISM Manufacturing survey came in at 50.3, which is not just significantly above the consensus estimate (48.3), but also way above the last print (47.8) and therefore represents the best reading since September 2022. ISM Prices Paid also came way above the consensus estimate (55.8 versus 53.0), and so did ISM New Orders (51.4 versus 49.8). What does all this mean for the markets?

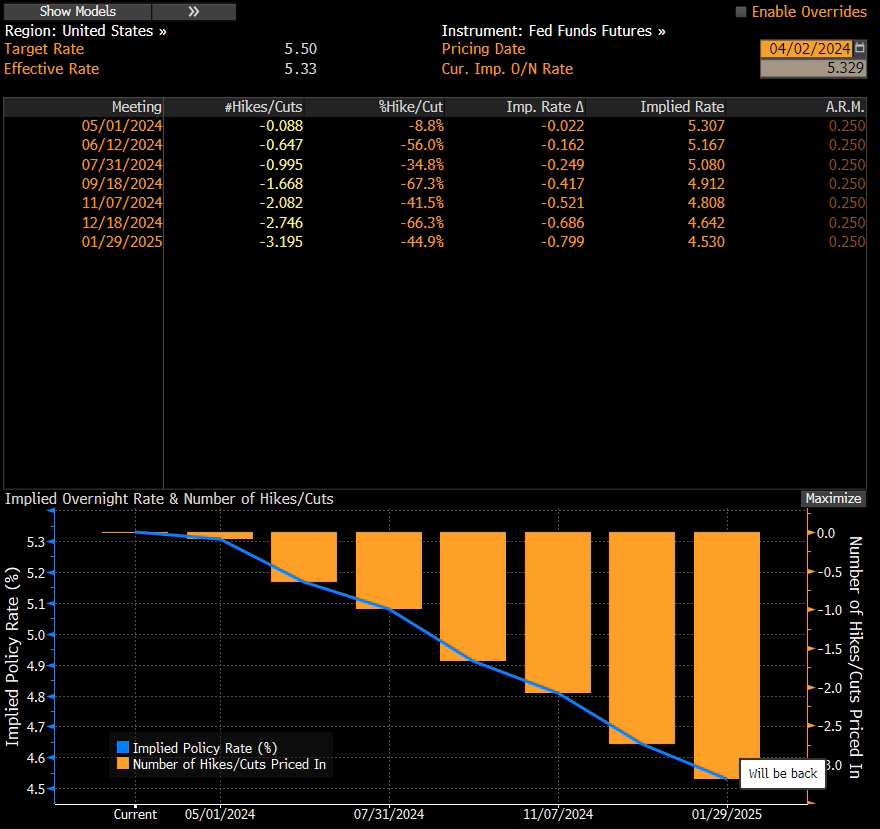

First of all, June rate cut is expected, but now it looks more like a coin toss with roughly 56% of probability:

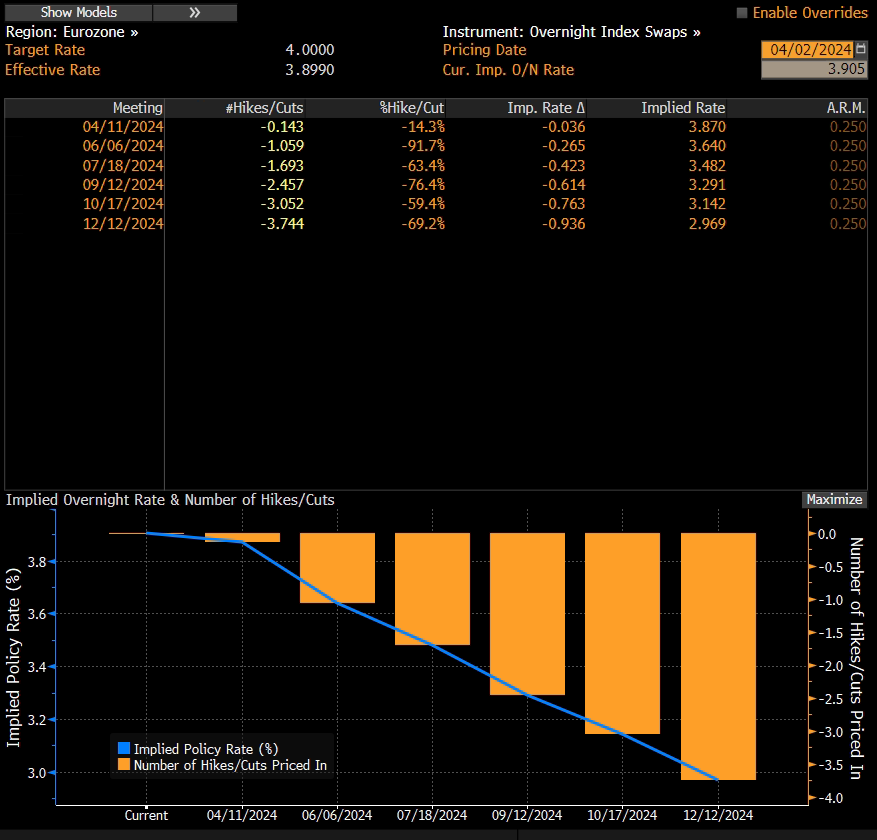

This essentially means that markets are questioning the prospects of three rate cuts this year (2.7 cuts are priced by the last FOMC meeting this year). This is clearly not in congruence with prospects in the euro area and since the ECB has a much different economic blueprint at its disposal, markets are still expecting a cut in June and about 3.6 cuts this year:

In other words, expectations are 2.7 cuts by EOY in US, 3.6 cuts in euro area and naturally, FX markets are selling EURUSD like there’s no tomorrow. ISM is regarded as soft data compared to employment figures and inflation, regarded as hard data. Nevertheless, predictive features of ISM are unquestionable and it’s quite likely that we can expect more strong labor reports and GDP readings. As a matter of fact, one of these readings might come in as soon as on Friday. Just to get a feeling for the market, the consensus estimate for the headline NFP figure due to be published this Friday (April 05th) are 203k (versus 275k in March), unemployment at 3.8% (versus 3.9% in March) and average hourly earnings at 4.1% YoY (versus 4.3% YoY in March). Just look at where the consensus estimate median is positioned and you can expect two things: low volatility on fixed income pre-NFP and surprises after the print.

Speaking about hard data, inflation prints in the US are sending a familiar dovish tune. In the last two months, both US and euro area inflation have proven to be more resistant than previously thought, mostly thanks to sticky service sector inflation. Prints from January and February, which both came in a bit higher than estimated, showed that the path towards the 2% inflation target entered the most challenging phase and that is curbing it down from 3% to 2%. In our last blog, we mentioned that we won’t be seeing first-rate cuts from FED nor ECB before meetings in June. But as time goes by and services inflation isn’t showing firm signs of yielding, we hear more and more often of cuts being pushed later in the year. FOMC voting member Christopher Waller said on Thursday that “there is no rush to lower interest rates” implying that recent economic data isn’t very optimistic in terms of curbing inflation. He later went on to say that inflation figures are disappointing and that he would like to see “at least a couple months of better inflation data” before cutting. The main reasons for this statement are a strong economy and a resilient labor market, which suggest to Waller that the Fed has more room to hold with the first cut.