Here you can find the dates for the upcoming events of the regional companies.

| wdt_ID | Date | Ticker | Announcement | Country |

|---|---|---|---|---|

| 6 | 23.12.2022 | SALR | Salus estimated business plan for 2023 | Slovenia |

Due to the nature of these events, they are subject to change (might be postponed or canceled).

As World Cup in Qatar is drawing to a close, the match between central banks and inflation is going into overtime. After hawkish FED, ECB states that higher for longer is the game they’re playing because the EZ economy is resilient and core CPI remains flat. What are the implications of yesterday’s ECB decisions on CROATI€ (and CEE in general)? Read in this brief research piece.

Although ECB’s Governing Council slowed the pace of rate hikes to 50bps at the December meeting, the Q&A session dropped the bomb with a statement that rates are expected to rise by 50bps for a “period of time”. This statement was further reinforced by this morning’s comment from François Villeroy de Galhau (Banque de France) on BFM Business Forum that market rate expectations fell too far in November and that he was also in the 50bps camp for the December move. To picture the change that has happened in the financial markets, one ought to look at the BBG WIRP function with implied forward interest rates. Here is the chart from December 13th (before FED & ECB speak):

Notice that the implied O/N rate on the 27th July meeting stood at 2.812% and now take a look at where it stands now:

It’s at 3.159%, meaning that markets are now expecting a +35bps higher terminal rate in the summer of next year. This is essentially the only change coming directly from Lagarde’s Q&A session on rate hikes because if you look more closely at the two screens, you can spot that markets were already pricing in another +50bps move in February and additional +25bps in March before pivoting. Now they are seeing +50bps in March on top of February’s +50bps, as well as another +25bps hike in May. With these statements, we see ECB’s terminal rate at 3.25%. However, Villeroy de Galhau reiterated this morning that GC still doesn’t see the terminal rate as a static number (i.e. it’s data-dependent).

Speaking about data dependency – why did the ECB GC do such a thing, this hawkish pivot? EURUSD has been steadily appreciating and energy prices have been gradually declining since peaking in early summer. The main reason in our view is the fact that although US Core CPI has been steadily declining in the past few months, EZ Core CPI remains stubbornly flat at about 5.0% YoY. We can say that after ECB trailed FED on the path to higher rates claiming that US and EZ inflation are two different stories (in the US it’s driven by a tight labour market, in EZ by higher energy costs), it becomes clear that ECB will have “more ground to cover” even after the FED is done with raising rates to make up for the lost time.

Speaking about ground to cover, what about the longer EGB bonds? ECB also announced APP shrinkage of 15bn EUR per month in period March-June, with possible revisiting the QT pace at the June meeting. With Muller’s and de Galhau’s comments from this morning, it’s quite likely that APP reinvestments might completely end after June, which was kind of priced in before the meeting. What is really new here is this three-month period of 15bn EUR/month slower reinvestments, reducing the aggregate demand for EGB’s by 60bn EUR in the aggregate (4 x 15bn = 60bn EUR). One PM correctly said – it comes at the worst possible time since that is when the CEE governments come to the market to borrow. With the current setup of restrictive monetary policy and loose fiscal policy in 2023 across the “old continent” to buffer higher energy costs, we can only support the claim that the only way for the European yields/spreads is up. With this in mind, we would be looking at the first SLOREP€ syndicate early next year (possibly in the first few days of January) to see how deep the markets really are.

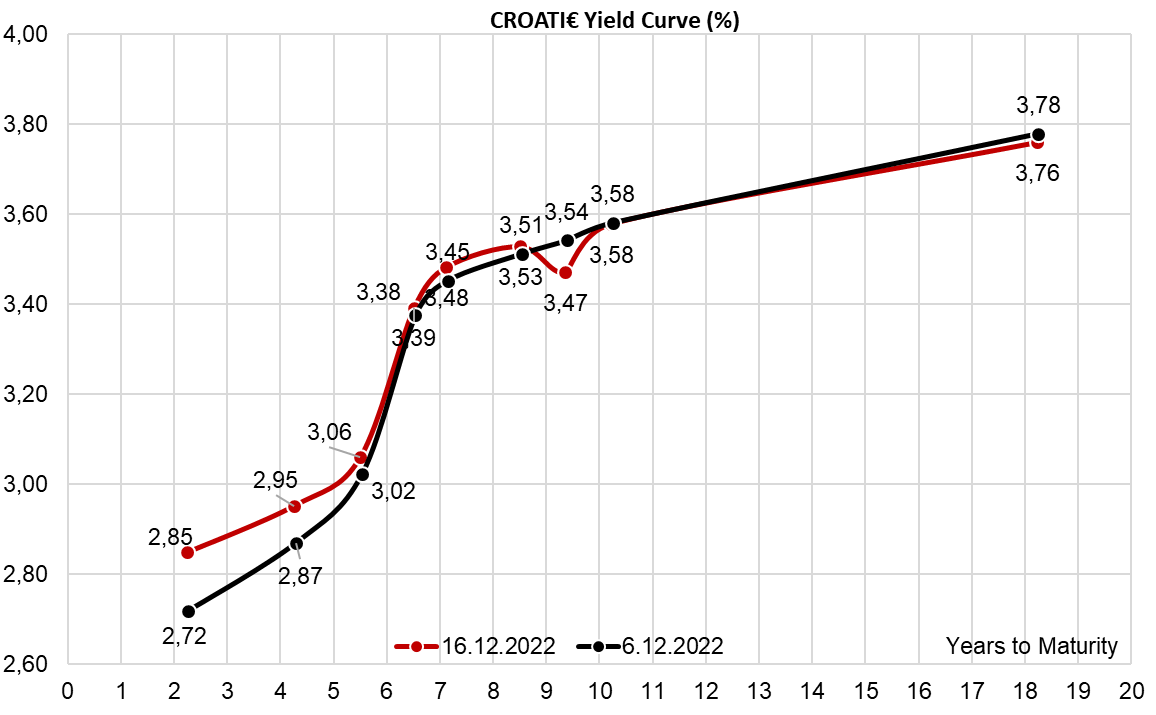

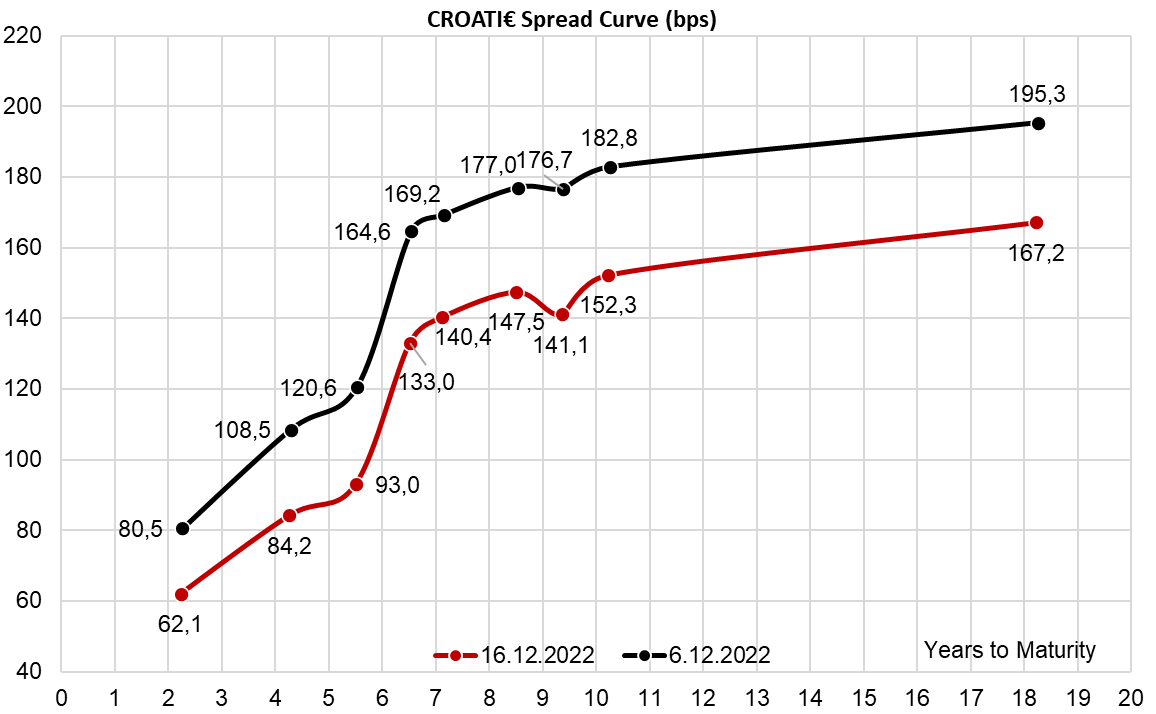

Speaking about Croatian international bonds, when you came to the office this morning your screen probably showed you that nothing has happened, but veteran bond dealers know that screens are mirrors into ancient history. Notice that the lo spread has widened from +183bps to +213bps in the last three trading sessions, so all that you see on CROATI€ on the screens this morning should be taken with a grain of salt.

Končar plans to realize a revenue of EUR 760m in 2023, with the value of backlog at the end of 2022 expected at EUR 1bn. Order intake for 2023 is forecast at above EUR 610m.

At the Supervisory Board session held yesterday, 15 December 2022, the consolidated Business Plan of Končar Group for 2023, at the proposal of the Company’s Management Board. The Company notes that the plan for the next year was prepared in uncertain and complex global circumstances impacted by the pace of the industrial post-Covid recovery, the duration of the Russian aggression against Ukraine, and the ensuing energy crisis and inflation trends. Despite these circumstances, further growth and development are expected by the Company in 2023.

According to the Company, on the basis of good order intake at the end of 2022, Končar Group plans to realize over EUR 760m in income in 2023. The value of the backlog at the end of 2022 is expected to reach EUR 1bn. Order intake for 2023 is forecast in the amount above EUR 610m, indicating that it accounts for 80% of the planned income from sales of products and services. Exports, primarily to European Union countries, continue to dominate in the total income. The majority of the planned EUR 434m income realized in the foreign markets is planned from Sweden, Germany, Spain, and Austria. Compared to the previous years, the export plan to Norway has significantly expanded, primarily as a result of the integration of Dalekovod into the Končar Group.

In addition to growing the income side, one of the four strategic goals set out in the Končar Group 2020+ Strategy is an investment in the development of products, technologies, and manufacturing capacities as the driver for the realization of sales planes. The Company notes that the investment cycle continues in 2023, with a focus on investments in new equipment and machinery. Energy transition and green CAPEX result in investments in improved energy efficiency and working conditions, primarily investments in photovoltaic power plants and the use of renewable energy sources. Investment in research and development is recognized as a long-term investment with the aim of creating a sustainable and profitable business and building up new competencies, which will contribute to the stability and further growth of the Končar Group.

The most significant planned projects include the continued development of environmentally friendly products in power engineering, the development of equipment and components for battery and hybrid trains, and projects in the field of digital technologies. The 2023 investment plan amounts to more than EUR 60m.

Investments in human resources, lifelong learning, professional development, and upskilling remain the Company’s priority goals. In 2023, EUR 1.2m is allocated toward learning and training costs. The Group plans to hire 205 new people, primarily highly educated employees, which would bring the total headcount to 4,885 by the end of 2023.