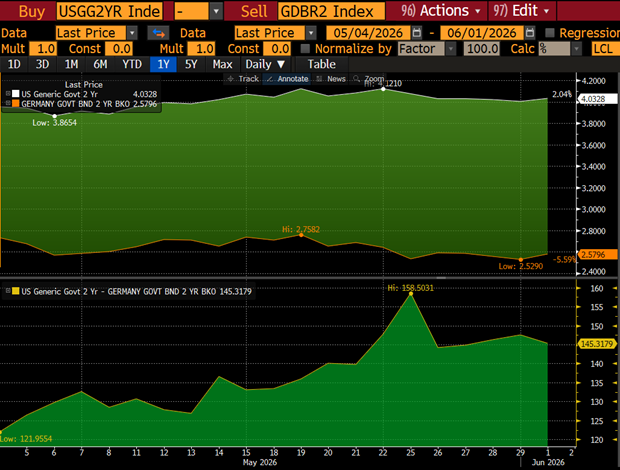

Kevin Warsh was sworn in as Fed Chair on May 22nd, and his first FOMC is less than two weeks away. Schatz yields fell about 24bps over eight sessions, from 2.77% in mid-May to 2.53% on May 29th. The US 2-year ended the month at 4.01%, essentially flat. The US-DE 2Y spread currently sits around 148bps.

The European side is a clean repricing story. Going into May, euro area money markets were fully pricing three ECB hikes by year-end. Barclays and JPMorgan had pencilled in April, June and July (Reuters, March 2026), and the probability of a third hike before December was above 90% (Euronews, May 2026). That pricing rested on Brent above $115, headline CPI moving from 2.6% in March to 3.0% in April, and hawkish commentary from Nagel and Schnabel that treated the energy shock as something the ECB could not look through.

Two things then changed. The Iran ceasefire held and oil retraced, removing the impulse behind the hawkish leg. Core euro area growth remained weak, and hiking into a slowdown became harder to justify. The market first reduced expectations at the back end of the curve.

The third hike, fully priced for the autumn meetings, is now closer to a coin flip. Removing roughly one full hike from the path is consistent with a 24bps move lower in the 2Y.

The US side is harder to summarise in a single repricing. Warsh has been one of the most vocal advocates of what he himself called “regime change” at the Fed, first on CNBC in mid-2025 and later in a November 2025 WSJ op-ed in which he argued the Fed’s balance sheet “can be reduced significantly.” At his confirmation hearing in April 2026 he told the Senate Banking Committee he favours “messier meetings… where we can have a good family fight” (CNBC, April 21). A Reuters analysis (May 22) framed his agenda as a way to “satisfy Trump’s push for lower interest rates while maintaining tighter underlying financing conditions” through a faster balance sheet runoff. The market reaction has been muted. The US 2Y traded as high as 4.14% around the May 13th confirmation vote and drifted back to 4.01% on the swearing-in. The cut path for the rest of 2026 is broadly unchanged from where it was before the nomination.

There are three reasons the front end has not followed the dovish rhetoric. The first is the balance sheet plan itself. Faster runoff — letting maturing Treasuries roll off the Fed’s holdings without being replaced — drains reserves and forces private capital to absorb a larger share of Treasury supply. The textbook effect is concentrated in longer maturities, but it spills into the 2Y. A more dovish rate path and a more hawkish balance sheet path partially offset, and that offset sits squarely on the front end.

The second is inflation. CPI is at 3.8%, with tariff pass-through still working through the goods basket. PBS News (April 22) noted Warsh “came across very much as an inflation hawk” at the hearing and did not mention the employment side of the dual mandate in his opening statement. The market is pricing the possibility that Warsh-the-commentator and Warsh-the-Chair will not behave the same way once 2% is still not in sight. The third reason is the framework change. Less forward guidance means the front end has to absorb more two-way risk between meetings. Fidelity’s Aditi Balachandar put it directly: “I would expect more interest rate volatility, given potentially less signaling from the Fed.” Higher rate volatility lifts the premium investors require to hold a 2Y, and that pushes against the rally that the cuts narrative would otherwise produce.

Both central banks meet in the same week in June — the ECB on the 11th and the Fed on the 18th. The ECB is widely expected to deliver one additional rate hike in June, while the Fed is priced for no change at this meeting. This leaves the current 148bps US-DE 2Y spread largely dependent on the tone and forward guidance from both chairs, particularly how Warsh balances his previous comments on rates versus balance sheet runoff, and whether Lagarde signals a pause after the June hike.