Nevertheless, as we continue our journey along the yield curve, a lot of things have occurred since our last stroll in early May. We moved from the negotiating table to all-out conflict several times; the last NFP print came in hot, the GDP revision came in higher, and inflation remains stubborn. Cherry on top, newly appointed Fed chair Kevin Warsh was hawkish during his first press conference (or at least the markets perceived him as such), and the published dots pointed the same way.

It is safe to say that the Middle East crisis is moving in the right direction (or is it?), toward a resolution of the conflict. One question remains, is the Strait of Hormuz open, and what is really meant by open? To try to answer this, one can look at the Bloomberg function ECAN HORMUZ, which shows the entry and exit of all tankers in and out of the Persian Gulf (we have indeed been staring at this chart like physician’s stare at a vital signs monitor…). After a sudden increase in tanker traffic, we are back to almost single-digit numbers, most of which are entries into the Gulf, far from the pre-war levels of nearly a hundred tankers in constant transit.

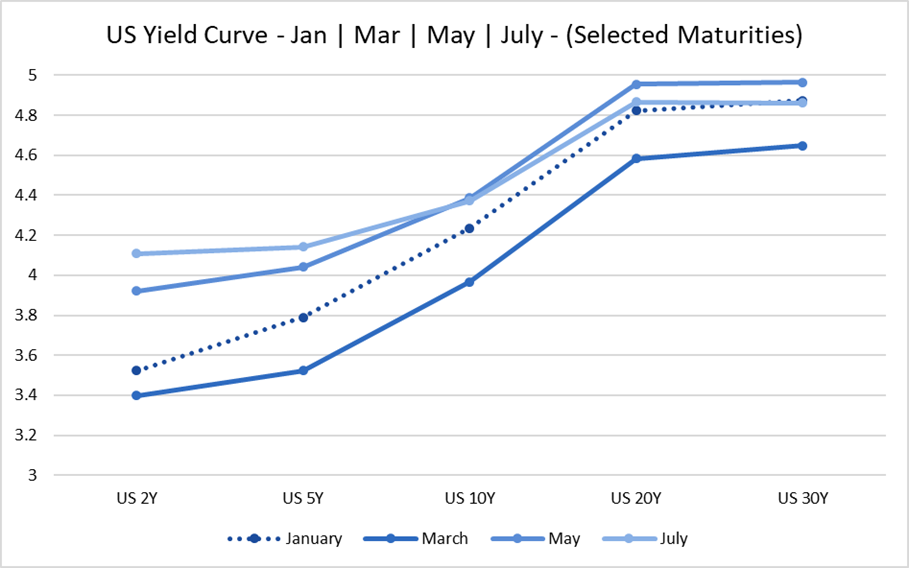

Anyway, enough rambling and on to the yields. During the last month, the yield curve took note of the constant back-and-forth between the US and Iran. Notably, the US yield curve experienced marked flattening on the short end of the curve, after the latest Fed meeting where Kevin Warsh, the newly appointed Fed chair, sounded surprisingly hawkish in his not-so-exuberant speech. Dots also signal that some (9 of 19, almost half) of the committee is on board for at least one new hike this year. The markets took note, and the US 2Y yield jumped by 19 bps to an equivalent of 4.107% since early May, taking the brunt of the beating. The US 10Y increased only slightly, by 10 bps to 4,373%. PCE inflation, the Fed’s preferred inflation measure, came in the same as in April, at 0.4% MoM headline and within consensus 0.3% MoM for core, which did not cause any sudden movements in yields. As headline numbers show a clear impact of energy prices, services still make up most of the print. As this is likely to continue, it will be interesting to see how inflation measures unpack once the backdrop of the Middle East crisis subsides.

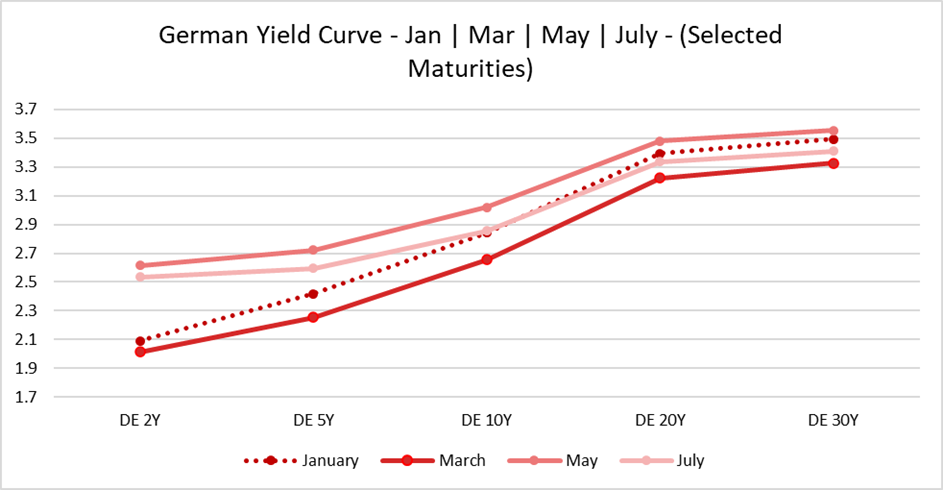

On the other side of the Atlantic, things are looking a bit different. ECB delivered, what seems to be, an insurance hike at its last meeting (we are yet to see if this will end up being a policy mistake). Despite this, the German yield curve remained relatively stable over the period, and in the last weeks showed to be positively receptive to de-escalation news in the Middle East. Incoming data points are still to remain a key driver of the ECB’s monetary policy in the future, as ECB’s Christine Lagarde in her speech last Monday sought to ease concerns over second-round inflation. On this note, Schatz yield remains elevated, tightening slightly by 8 bps, and as of this writing, sits at 2.53% in yield. Bund now firmly trades below the 3% levels seen in April and May, tightening by 12 bps since my last blog, currently sitting at 2.85% in yield, a level which it does not seem to be able to breach.

Despite all of this, we are still in for an interesting week ahead. On Tuesday, we will be getting the German CPI numbers, followed by the US CB Consumer Confidence, which will shed some more light on the status of the US consumer, Chicago PMIs, and JOLTS. On Wednesday, we will see the status of EU CPI, where the Core numbers are likely to remain the same YoY, while the MoM will show us if the momentum in inflation is moderating. And finally (since Friday is a US holiday), we will be getting the highly anticipated US unemployment data with NFP numbers taking center stage, showing us the underlying dynamics of the US labor market.