Slovenia, as a value play, has significantly benefited in 2021 from a global rotation to value stocks. However, this trend subsided on global markets recently. Was the rotation to value short lived? Find out in this brief article.

Following the positive vaccine news back in late 2020, global equity markets turned to cyclicals and value stocks, which continued to outperform during the most of 2021. However, we witnessed a slight setback of value in the recent times, so you might be asking yourself – was the rotation to value relatively short lived?

Looking at the Slovenian market, one can observe that financials have recently underperformed, with Triglav and Sava Re dropping by more than 6% in June (partially due to ex date), while NLB ended the month slightly in green.

Does this indicate the end of very strong 2021 rally of value in the region? The short answer to that question is: we do not think so.

Value stocks perform well in economic recoveries

Let’s start with the obvious. If we were to look at how value and growth performed during the outbreak of Covid-19 until late 2020, we reach an interesting conclusion. What is considered as traditionally less risky (low P/E, low P/B, high dividend yield, low growth) has significantly underperformed since the outbreak of the pandemic. In that sense, this crisis is not like the previous ones. However, in late 2020 positive vaccine news and the expectations of economic normalization brought a return to cyclicals and value stocks, which have been lagging growth stocks for the majority of the rebound. With the markets expecting one of the strongest economic expansions in decades, due to the vaccine rollout, healing labour market and pent-up demand, the turn to value and cyclicals seemed reasonable. However, following a very strong YTD performance of value stocks globally, one might argue that the recovery is already priced in and should not provide further tailwind for the coming period. In other words, we should not expect to see big changes in expectations regarding economic growth in Europe. Although there isn’t a full consensus among analysts regarding the aforementioned, it is plausible that the argument for the economic recovery will not be the sole driver of value in the coming periods.

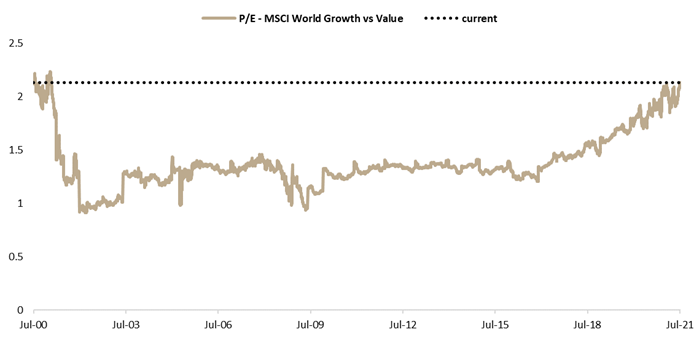

P/E gap between value and growth seems quite large; Slovenia’s gap continues to increase

If we were to look at the forward P/E ratios of MSCI World Growth vs Value indices, we reach a conclusion that the gap between the growth and value is remarkably large, reaching the early 2000s (dot com era). That alone should cast doubt that growth should be outperforming in the coming periods.

Source: Bloomberg, InterCapital Research

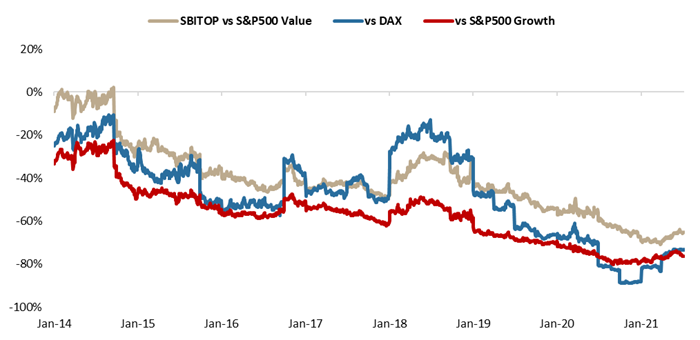

When looking at US and Eurozone, one can see that both markets are traded at quite higher 12m forward P/E’s compared to their 20-year medians. However, that alone should not bring us to the conclusion that these markets are overvalued. On the flip side, Slovenia, which can be considered a pure value play, is traded at a significant discount to developed markets, with SBITOP’s P/E standing at 8.8x. Despite being one of the best performers globally so far in 2021, SBITOP’s discount to developed markets remains to be very large, reaching the largest gap in more than 7 years (observed period). To be specific, according to Bloomberg, SBITOP’s discount to developed market reached more than 70%, while compared to S&P500 Value that discount is at 65%. Taking into consideration that a certain discount is reasonable due to the specificity of the Slovenian equity market, we still deem that the market is very much fundamentally attractive. The fact that we are expecting to see quite strong 2021 results of almost all Slovenian blue chips, further backs the above-mentioned statement.

Source: Bloomberg, InterCapital Research

Rising yields would benefit value over growth

Rise of yields was one of the most scrutinized trades since the beginning of 2021, but that trend somewhat reverted in the last two months. The main driver for yield rise was obviously higher inflation and large bond supply due to enlarged fiscal spending. Furthermore, yields rose rapidly due to investors’ scare that central banks could find themselves behind the curve and then they will have to react abruptly to curb inflation towards their goals. However, central banks were dedicated in ensuring markets that inflation will prove to be transitory and decided not to tighten their policies. Actually, in March, ECB decided to accelerate its PEPP purchases in Q2 and Q3 to ensure lower cost of debt for recovering economies in eurozone. Fast forward to the beginning of July 2021, ECB followed Fed and decided to change its monetary policy strategy meaning that from next meeting, it will adopt symmetric 2.0% inflation target, i.e. ECB’s policy could be looser for longer than previously thought. However, some analysts believe that ECB could decelerate its PEPP program in the beginning of Autumn especially in case yields stay at these depressed levels. In any case, ECB will not have an easy task bearing in mind eurozone’s addiction on negative yields meaning that its standard APP could be enlarged once PEPP ends in March 2022. Talking about QE, Fed is also expected to slower down its asset purchase program and Jackson Hole Symposium in the end of August would be the perfect time for the announcement. Fed could use the opportunity to announce that their USD 120bn a month program could be slowed down from the beginning of 2022 and that should be the first firm sign that central banks could slowly move away from their heaviest tool.

In the last few years, August showed as month in which rates saw their bottom and then started rising in the beginning of Autumn. Bearing in mind all of the above, one shouldn’t be surprised in case yields see start rising soon, as investors see that ‘transitory’ inflation shows to be here longer than previously thought. So what does all of the above mean for value stocks? The higher expected bond yields would relatively favor value stocks over growth, while financials would be one of the beneficiaries. Banks remain strongly positively correlated to bond yields and therefore higher yields could be of a solid benefit to them. The same goes for insurance. All of the above mentioned is one of the reasons why we remain positive on Slovenian financials as well.