The week ahead of us offers multiple interesting events and upcoming data points as markets digest President Trump’s statements over the weekend. We’ll start by revising some data points we received last Thursday and Friday and then switch back to this week as Trump’s “Liberation Day” on Wednesday nears. Stay with us as we digest the data and statements and analyse the implications for German Bunds as they remain under the spell of the global macro.

The week ahead of us offers multiple interesting events and upcoming data points as markets digest President Trump’s statements over the weekend. Let’s start by revising some data points we received last Thursday and Friday. The third estimate of Q4 GDP and real consumer spending data showed that growth is still robust, even though surveys point to a weaker performance in the future. Weekly initial jobless claims show no apparent signs of deterioration in the labour market, but we are eagerly awaiting the latest non-farm payrolls report coming this Friday. Expectations are centred around 140k, which is not that high, and that might provide more support for bonds if numbers do come a bit lower. The Fed’s preferred inflation gauge, the PCE Price Index, printed 2.8% YoY, but more focus was put on higher personal income and lower personal consumption data points that were interpreted as dovish, leading to the start of the rally in US bonds. CPI data for France and Spain arrived markedly lower at 0.8% and 2.3% YoY, respectively. This led to further increases in expectations that the ECB will cut its deposit rate facility further by 25bps at their April 17 meeting. With German inflation data coming in line, the market now expects the cut to happen with a 90% probability, and with no clear pushback from the most influential governors in their interviews, it seems as if it is a done deal.

Switching back to this week, as Trump’s “Liberation Day” on Wednesday nears, let’s first briefly check how the market interpreted his statements over the weekend. He hinted further at plans of taking over some control of Greenland before “other forces put their hands on it” and said that he “couldn’t care less” if car prices rise as a consequence of 25% tariffs that are due to come into force on Thursday. These statements reverberated in the markets, sending them into risk-off mode and pushing the bond prices higher with the German yield back below 2.70%. As would be expected, American equities are now eyeing the lows in this correction cycle they reached two weeks ago. President Trump also switched the tone of his communication with Russian President Putin. He threatened secondary tariffs on buyers of Russian oil if Putin were to refuse a ceasefire and stated that he is angry at him for casting doubt on President Zelenskiy’s legitimacy. He also sent verbal bombs addressed to Tehran by saying he would bomb them if they didn’t agree to a nuclear deal on his terms. Oil markets reacted with higher prices, and the increasingly less likely prospects of a peace agreement or a ceasefire provide further support to the risk-off tone.

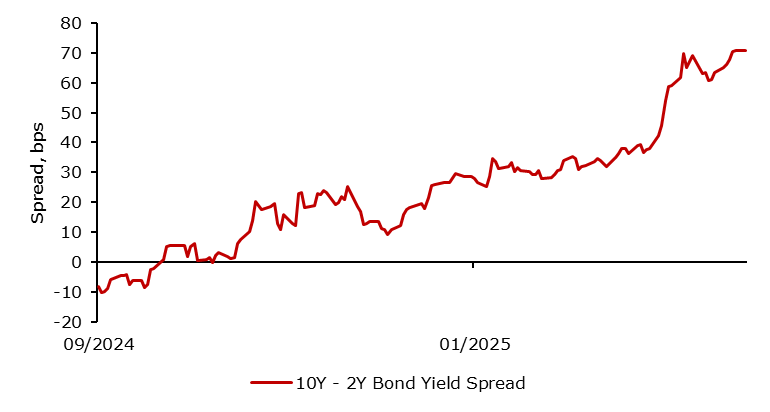

It remains to be seen what the EU’s response will be to the upcoming 25% tariffs and possible extra reciprocal and targeted tariffs on specific sectors (possibly pharmaceutical). Some conflicting statements were made by EU officials, ranging from planned concessions after reciprocal tariffs hit to plans to tighten their grip on American companies in the tech sector with stricter policy regarding fines and possibly introducing tariffs on them. German Bunds remain under the spell of the global macro, and immediate acts take precedence over future implications of higher issuance to fund the defence spending. They are likely to remain supported as the narrative has shifted toward tariffs and political statements. The spread between the American and German 10y yield has remained relatively stable during the past couple of days, but the German curve is poised to steepen further after cloudy tariff-infested skies clear and the narrative switches back towards higher deficits, with the short end supported by the data that remains indicative of further cuts.

Germany 10Y – 2Y Bond Yield Spread

Source: Bloomberg, InterCapital