On the last day of October Croatian government presented draft budget for 2020 and sent it to the parliament for vote. HDZ-led government expects consolidated budget to end 2019 with deficit of 0.1% GDP (ESA 2010 methodology) while presented document envisages surplus of 0.2% and 0.4% GDP in 2020 and 2021, respectively. In this article we are analyzing drafted budget and its consequences for the capital markets.

Croatian budget for 2020 was based on relatively optimistic macroeconomic scenario. Namely, government expects GDP to grow by 2.8% YoY in 2019 and then to deteriorate only modestly to 2.5% and 2.4% in 2021 and 2022. They expect personal consumption to be on the front seat for the next three years while growth of investments should decelerate from 8.5% YoY in 2019 to 6.1% in 2020 and to 5.2% in 2022. However, government expects growth of exports to increase to 3.0% in 2022 (2.3% in 2019) driven by acceleration of exports of goods which could be questioned in case of prolonged economic slowdown or even recession among Croatian main trading partners. On the other side, government expects imports of goods and services to grow at slower pace which Finance Minister stated as one of the goals for the future. Also, worth mentioning is that unemployment is expected to fall further, from 8.4% in 2018 to 6.3% in 2022 while average salary is expected to rise by 3.5% in average in period 2019-2022. Just to put things into perspective, most CEE countries are most likely to see stronger deceleration in the following years due to slowdown of core EU countries and several geopolitical risks. However, one should mention that most of them rose at higher pace compared to Croatia so looking at relative change, modest slowdown of Croatian economy could still be in cards in case no major deterioration takes place in developed world.

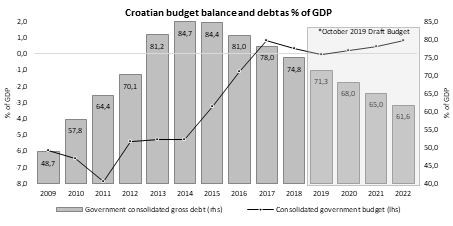

After two years of posting consolidated budget surpluses, Croatia is expected once again to see deficit, although in rather small amount of HRK 582m, i.e. 0.1% of GDP. However, in 2020 Mr Maric expects budget to be in surplus of 0.2% of GDP and 0.4% and 0.8% in subsequent years. Eventually, with above mentioned GDP growth, that should force debt/GDP more South, i.e. to 61.6% in the end of 2022, according to Ministry of Finance.

Source: Ministry of Finance, InterCapital Research

So, what’s in the budget for 2020 and what changes it includes? First, Ministry of Finance expects revenues to increase up to HRK 145,1bn or 5.4% YoY down from 6.4% that we’ll most likely see in 2019. Although government expects tax revenues to increase by 3.1% YoY in 2020, strongest driver of next year’s increase should be EU funds that are expected to increase by 23.2% YoY due to slower withdrawal in 2019 (first plan for 2019 was HRK 17,45bn however only HRK 15,23bn is now expected to be withdrawn). As said above, tax revenues should increase slightly above GDP growth despite 4th round of tax reform that will include decreased income tax for young workers, several tax deductions such as food and housing allowance for workers, higher limit of net income to be taxed at lower corporate income tax and so on. As wages are expected to grow around 3.5% in 2020, social security contributions are also expected to rise, by 3.9% YoY and accelerate to 4.6% and 4.5% in 2021 and 2022.

On the other side, expenditures are expected to rise by 5.0% YoY in 2020 (HRK 147,29bn) and 1.2% in both 2021 and 2022, reflecting slightly optimistic stance of the government, bearing in mind that 2020 is election year. As most likely wages are set to rise further in the following years, wage expenditures are expected to increase by 7.2% in 2020 compared to 3.4% in 2019. It’s worth noting at this moment that proposed budget has already calculated wage increase of 6.12% for all public workers. Although we are still to see how government plans to finance maturing bonds in November, the most obvious cut in expenditure is coming from lower debt burden. Namely, interest costs stood at HRK 9.71bn in 2019 and will decrease sharply to HRK 8.06bn and 7.39bn in 2020 and 2021, resulting in savings of almost HRK 4bn in just two years that we should thank to economic cycle and ex-ECB governor Mr Mario Draghi.

If you were focused on numbers above close enough, you realized that central government is expected to end 2020 with deficit of HRK 2,15bn. However, when consolidated with local government, SOEs and other adjustments consolidated budget should post plus.

And last, looking at Croatian bond market, in case government’s plans go through it seems like both local and Eurobonds could become even more illiquid as government’s financing needs are decreasing meaning that government will just roll existing bonds or decrease its debt stock while Croatian financial industry is becoming bigger and bigger meaning that current situation where Croatian HRK 10Y bond yields 10bps less compared to its EUR denominated Eurobond peer could stay with us for a while.