In one of my previous posts (link), we discussed how leveraged ETFs work in theory: total return swaps, daily resets, volatility drag. Today we will discuss a single-stock leveraged ETF scandal that happened in South Korea last week, which provided a real-world illustration far more dramatic than any textbook example.

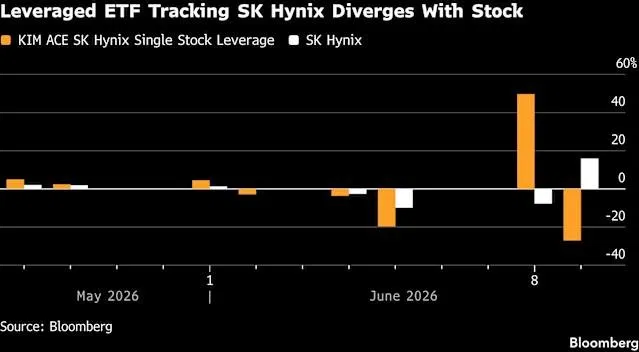

On June 8, SK Hynix (one of the KOSPI index heavy-weights) fell nearly 8% amid concerns about U.S. interest rates and a broader debate about semiconductor valuations. Investors in the ACE SK Hynix Single Stock Leverage ETF, a product designed to deliver twice the daily move, might have expected a decline of around 15%. Instead, it closed up nearly 50%, trading at an 86% premium to its actual net asset value. The next day, as SK Hynix rebounded 16%, the ETF fell 27%. Two consecutive days of moving in the exact wrong direction, by enormous magnitudes.

To understand how this happens, we need to look at one specific piece of the ETF’s plumbing most investors never think about. A leveraged ETF achieves its amplified exposure through derivatives, swaps or futures. However, derivatives alone don’t explain why the market price stays close to the fund’s net asset value throughout the trading day. That is the job of the liquidity provider (LP): a financial institution that continuously posts bid and ask quotes for the ETF. If the ETF drifts above NAV, the LP can sell it short and hedge with the underlying, locking in a risk-free profit and pushing the price back down. This continuous arbitrage is what keeps market price tethered to fair value, and it works reliably, until it doesn’t.

On the Korea Exchange, LPs are explicitly exempt from their quoting obligation during the closing call auction, the 3:20 to 3:30 p.m. window that determines the official closing price. This is not a system failure; it is a deliberate regulatory design, intended to keep market makers from distorting what should be an open, order-driven price discovery session.

The problem is that for thinly traded ETFs, removing LP quoting creates a window where price is set purely by whoever shows up with a market order. On June 8, an already volatile session (KOSPI index fell nearly 9% intraday and triggered a 20-minute trading halt) also triggered a volatility interruption in the ETF itself, pushing the final close to 3:32 p.m. With LP quotes absent and concentrated market-buy orders hitting a near-empty order book, the ETF price was driven to levels completely detached from reality. All six other SK Hynix leveraged ETFs, which did not experience the same thin-book conditions, fell exactly as expected, roughly 15–18%.

The real question is, could this happen to more mainstream ETFs? The structural risk exists wherever LP quoting obligations weaken, but the probability of a large, liquid ETF experiencing anything like this is very low. Products like TQQQ have enormous trading volumes, multiple competing market makers, and deep underlying liquidity across hundreds of stocks. Even if one LP stepped back, the arbitrage opportunity would immediately attract others. The depth of the order book prevents a single wave of market-buy orders from driving prices to 86% premiums.

The risk concentrates in newly launched products with low AUM and few active market makers, single-stock leveraged ETFs whose underlying is highly volatile, and markets where closing auction exemptions are broad. The SK Hynix incident checked all those boxes simultaneously. The ACE fund had only launched days earlier as part of a wave of 16 new single-stock leveraged products that debuted on May 27, rapidly popular, but structurally thin.

The Korea Exchange has indicated it will tighten LP quoting rules for leveraged single-stock ETFs around the closing auction, and the fund issuer has pledged a review of its quoting systems. The regulatory gap that allowed this has been exposed clearly enough that a repeat seems unlikely in the near term.But the broader lesson holds: an 86% premium to NAV is not a story about leverage. It is a story about what happens when the mechanism keeping a price tethered to reality disappears for just ten minutes, in the wrong product, on the wrong day. For well-established leveraged index ETFs in deep markets, none of this changes the fundamental calculus. For anyone exploring newer, thinner products, the lesson is worth internalizing: it is not just the leverage that can hurt you. Sometimes the risks are structural.