Just three months have passed, yet it feels like an entire year, given the scale and speed of developments. The period has been marked by extraordinary geopolitical and economic shocks—from renewed discussions around a potential U.S. acquisition of Greenland and the rollout of aggressive tariff policies, to the Supreme Court striking down IEEPA-based tariffs.

Renewed bouts of volatility, driven by major geopolitical shifts and recurring TACO dynamics, have made forecasting and trading increasingly difficult. Markets have grown accustomed to sharp reversals, as escalation is often followed by rapid de-escalation. However, the current situation appears different. Iran seems intent on pushing back more forcefully, potentially by prolonging the closure of the Strait of Hormuz—a critical artery for global LNG and oil transport. This adds a layer of uncertainty that markets may not be able to quickly price in or dismiss. The narrative has also become more complex. While the United States claims that negotiations are progressing well, Iran insists that no talks—direct or indirect—are taking place. This disconnect further clouds the outlook and reduces the likelihood of a swift resolution. There is no clear or easy path to de-escalation. Gulf countries, already on edge, have been directly impacted by missile strikes attributed to Iran, leading to significant damage to energy infrastructure and even attacks on several vessels.

The repercussions are particularly severe for both Asian countries and Europe. Many Asian economies rely heavily on fuel shipments passing through the Strait of Hormuz, and the disruption is already leading to rationing and long queues at petrol stations. The issue extends beyond crude oil alone—crack spreads have surged, significantly increasing the cost of refined products. Strategic reserves have already been tapped, but if the disruption continues, they will only serve as a temporary buffer for the real economy. The likely outcome is a classic supply shock: higher inflation combined with weaker growth. In Germany, inflation data is already reflecting this pressure, with month-over-month inflation exceeding 1% as gas prices spike. If the situation persists, the European Union could face another wave of deindustrialization, particularly if it fails to meaningfully reduce regulatory burdens. At the same time, Europe has yet to make substantial moves toward expanding nuclear energy or developing its own oil and gas resources, reinforcing its dependence on external energy sources and contributing to persistently high energy costs. Market reactions have been more muted than one might expect under a scenario where the Strait of Hormuz is closed for an entire month. That said, equity markets have still taken a hit: both the DAX and Nikkei are down over 10% since the start of the conflict. The S&P 500 has proven more resilient, largely due to the United States’ relative energy independence, which reduces its exposure to disruptions in the strait.

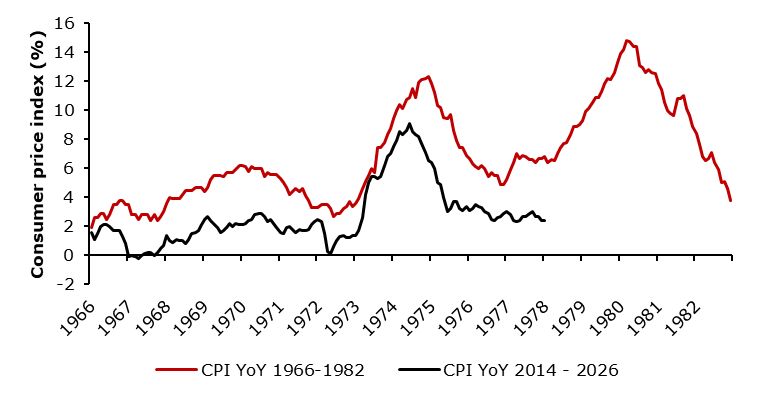

The most pronounced impact has been in European fixed-income markets, which have experienced significant losses over the past month. German Bunds have declined by 4%, with Schatz yields moving similarly, contributing to a flattening of the yield curve. Traders and researchers continue to draw comparisons to historical oil shocks of the 20th century. However, the situation bears a closer resemblance to 2022, when the European Union was the most severely affected. In contrast, the current shock is hitting Asian economies the hardest. If the conflict persists, the risk of a second wave of inflation is rising. Interestingly, those who overlaid 2022 price action onto patterns from the 1970s oil shocks may be proving correct in anticipating renewed inflationary pressure.

US CPI indices YoY change comparison (1996 – 1982 and 2014 – 2026, %)

Source: BLS, InterCapital