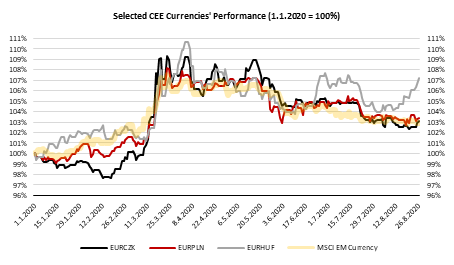

CEE currencies depreciated strongly after corona virus started and recovered after but are still far from the levels seen 6 months ago. Hungarian forint came closest to the levels seen before corona virus but is depreciating again due to macroeconomic data. The data from Q2 showed that economy witnessed the worst period on record (compared to same period last year and quarter before). What are the main drivers behind these moves and what to expect next read in this brief article.

Hungarian forint has seen depreciation trend in the last two weeks due to worse than expected GDP data for Q2 and jump of inflation above MNB’s target. Namely, its GDP plummeted by 13.6% YoY (-10.1% YoY expected by BBG consensus). Although detailed breakdown was not published yet, we assume that significant drop was seen in all parts of GDP while services suffered the most. On the other side, statistical office data showed that inflation jumped more than expected in July, i.e. it stood at 3.8% compared to June’s 2.9% making it more difficult for central bank to react as its mandate involved both price stability as well to support the Government’s economic policy.

Talking about central bank, this week they decided to leave reference rate at 0.6% after cutting by 15bps for the two consecutive months. However, they decided to increase its weekly QE purchases and will provide additional liquidity through repo operations. Central bank stated that they expect inflation to remain around its current level in the coming months before stabilizing close to its target of 3.0% although disinflationary effects of the coronavirus should become even stronger over the forecasting horizon, according to the bank. Regarding last month’s rise, central bank commented that faster rise was mainly caused by change of structure of aggregate supply and demand but also due to changes in indirect taxes and change in fuel and food prices. Also, one should consider that prices increased more than expected in almost all EU countries and one of the explanations was that summer sales were pushed to August meaning that in August inflation should fall back to June levels.

Bearing in mind central bank expects inflation to decelerate while economic recovery should take many more months, it is not excluded that central bank could increase QE even more if needed. In March, CB showed its willingness to fight with economic upheaval and managed to reduce long term yields while lifting short rates (widening the corridor between reference rates, i.e. between reference rate and overnight deposit and overnight collateralized lending rate) to curb depreciation trend of HUF.

Hungarian forint reached 344 for EUR last month but due to worse than expected macroeconomic data and increased QE depreciated above 355 yesterday. Although equity markets around the world are showing signs of prolonged recovery and some of them already being in green in YTD terms, buyers are still hesitating from going into emerging markets and HUF holders will have to wait for some time before risk-on comes in our region.

Looking at the region, CZK has also seen modest depreciation in the last two weeks while PLN, RON and HRK are trading water. CEE bond market is still in the summer mode but considering latest fall in bund prices we expect that to end abruptly. Furthermore, we expect bond supply to increase once again with issuance season reemerging already next week.

Cinkarna Celje published their H1 2020 results yesterday, posting an 4% YoY decrease in sales, 15% YoY decrease in EBITDA and a net profit of EUR 9.9m (-21% YoY).

In H1 of 2020, Cinkarnca Celje recorded sales revenues of EUR 88.7m, which represents a decrease of 4% YoY. The result represents a significant decrease when compared to last quarter’s 5% YoY increase in sales. The reason behind the drop lies in several factors. First, the spread of the COVID-19 pandemic triggered a process of accumulation of pigment inventories by customers at the end of Q1, which positively impacted the top line. Secondly, the absence of Chinese producers in the European market at the beginning of the year added to the rise in demand. However, in Q2 lower production and higher inventories led to a decrease in sales. Still, according to the Management’s estimates, Cinkarna Celje’s decline in sales was smaller than the overall decline in sales in the titanium dioxide market.

EBITDA fell 15% YoY, amounting to EUR 17.7m. The primary reason for the decrease are lower sales and higher operating expenses which went up 3% YoY. Finally, the bottom line amounted to EUR 9.9m, representing a 21% YoY decrease.

However, note that in 2020 Cinkarna Celje changed the method of valuing stocks of finished products compared to previous years. This change increased the operating result of the first half of the year and will reduce the operating result of the second half of the year, while the impact will be nullified on an annual basis. The positive impact of the change on net profit in the first half of the year amounted to EUR 2.35m.

Turning our attention to CAPEX, in H1 2020 Cinkarna Celje invested EUR 5.6m, which is 28.2% of the planned amount. The amount is lower than planned mainly due to the suspension of non-urgent investment and maintenance works during the pandemic due to COVID-19, but also due to the usual dynamics of works falling due for the most part in the second half of the year. The majority of invested funds were intended for the production of titanium dioxide to improve the quality of products, ensure the reliability of individual devices or processes, improve the conditions of safe and healthy work and reduce environmental impacts.

Cinkarna Celje Key Financials (EUR)

Yesterday, Sava has announced notice of Management Board intention to submit evidence to regulator of their ability to pay dividend. To the extent that the Agency has no reservations regarding such dividend distribution, dividends for 2019 may still be paid out this year.

Sava has announced that it intends to send a notification to the regulator declaring their intention to pay out dividends in respect of 2019, supported by qualitative and quantitative evidence. Insurance Supervision Agency, the regulator has given recommendation to insurers on 20 August on suspension of dividends after 1 October 2020 due to deeming the situations in relation to Covid-19 and its impact on the economy and the insurance sector as still uncertain. This recommendation was published by Sava Re on 21 August 2020.

Announcing intention to pay dividend is in line with the option and conditions set out in the regulator’s recommendation. As stated in the recommendation, the regulator will examine such notification and take appropriate measures in accordance with the law. To the extent that the Agency has no reservations regarding such dividend distribution, the management board, subject to approval by the supervisory board, will call a general meeting to consider the proposed distribution of dividends so that dividends may still be paid out this year.

Luka Koper approves EUR 1.07 DPS, DY 5.6%, ex-date Sep 23rd

Luka Koper published a resolution from their AGM yesterday in which the shareholders approved a dividend of EUR 1.07 DPS. Note that the approved dividend came as a counterproposal to the initially proposed EUR 0.92 per share.

At the current share price, the dividend yield is 5.6%, while the ex-dividend date is 23 September.

In the graphs below, we are bringing you the historical overview of the company’s dividend per share and dividend yield.

Luka Koper Dividend per Share (EUR) & Dividend Yield (%) (2013 – 2020)

INA approves HRK 62.27 DPS, DY 2.2%, ex-date Sep 1st.

INA published a resolution from their AGM yesterday in which the shareholders approved to allocate a part of FY 2019’s net profit as dividend. Of the HRK 655.6m of 2019 profit, HRK 622.7m was approved to be paid as dividends. This translates to a dividend per share of HRK 62.27 and is 50% below last year’s dividend of HRK 125 per share.

At the current share price dividend yield is 2.2%. Note that the ex-dividend date is 1st September 2020.

In the graphs below, we are bringing you a historical overview of the company’s dividend per share and dividend yield.

Dividend per Share (HRK) and Dividend Yield (%) (2015 – 2020)