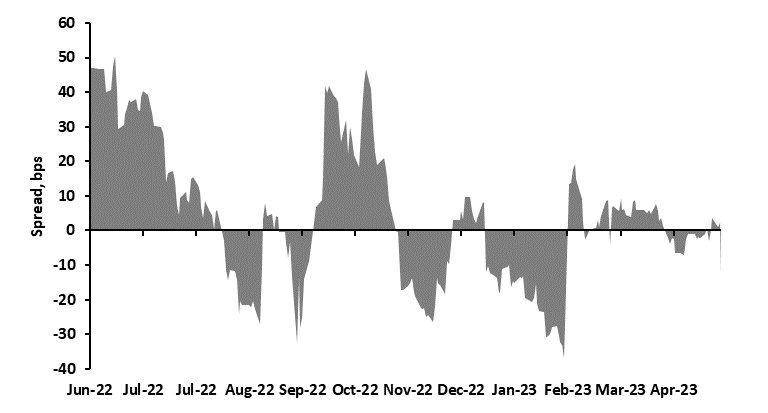

Inflation data in the United Kingdom surprised the market on Wednesday as the YoY inflation rate came worse than expected. In addition to that, on Tuesday the released PMI data indicates that the economic growth should remain solid. Consequently, the Gilt yield curve shifted north. Yields are now approaching levels seen after the announced tax reform of Kwazi Kwarteng which spurred volatility in the market as bond markets quickly penalized expansionary fiscal policy during times of high inflation. Pension funds lived through difficulties back then, but a similar problem in UK financial system may emerge again.

PMI data on Tuesday fueled the depreciation of Gilts as the market expects additional hawkishness of the monetary policy. Also, inflation data pushed yields further up as the expectations were heavily overshot (0.7% MoM expected vs 1.2% MoM actual. The most significant contributor to the headline rate is the food prices which continued their worldwide growth and amounted to 19.1% YoY in April 2023. Core CPI rose from 6.2% YoY in March to 6.8% YoY in April due to the growth in services CPI. The core inflation rate is still at very high levels and is struggling to drop down to sustainable levels. According to OIS, the market priced in more than one rate hike in two days as the data showed a highly resilient headline and core inflation rate in combination with higher expectations of growth. Higher MoM inflation rates last year in April are contributing to the softer YoY rate, but recent MoM inflation data are indicating that the higher inflation rates are going to persevere.

The market reacted swiftly pushing yields up by 30 – 50 bps across the yield curve over the course of just one week. 2-year yield went up from 3.86% to 4.35%, 10-year from 3.85% to 4.23% while the 20-year yield went up from 4.23% to 4.55%. In comparison with Eurozone and US yield curves, the market presumes that the inflation problem in the UK is the hardest to solve. German 10-year yield is currently 32 bps off its highs in this cycle and the US 10-year Treasury yield stands at 60 bps off highs. However, both US and Euro yield curves are heavily inverted, but in the UK the situation is different. Spread between 10-year Gilt and 2-year Gilt amounts to a small -12 bps while in the US and Eurozone is at -60bps and -37bps, respectively. Lighter inversion in the UK points out deeper economic problems that the country is facing such as persistent inflation which indicates that the tightening cycle is still far off its end. Also, this move inverted the 10-year – 2-year spread again as it was not inverted before the data release.

UK pension funds may be in focus again as they were rescued in October last year. Still, other significant financial market participants may emerge as a problem similar to regional banks in the US as the yields approach levels seen in September and October. Portfolios of such banks may be in danger as financial instabilities in US and Eurozone may fuel bank runs in the UK as a result of a chain reaction. Also, one should be aware that BoE will probably backstop any financial difficulties similar to the US (BOE has already done temporary QE to save pension funds) which could be a short-term bullish factor for Gilts. To conclude the analysis, I would argue for longer-term higher interest rates as inflation remains persistent and fiscal policy trying to boost economic growth in the longer term after subdued growth post-Brexit.

Gilt 10-year to 2-year spread

Source: Bloomberg

In Q1 2023, Romgaz recorded a revenue decrease of 25.9%, an EBITDA increase of 53.5%, and a net income of RON 970m, a decrease of 1% YoY.

Starting off with the revenue, Romgaz recorded revenue of RON 2.91bn, representing a decrease of 25.9% (or RON 1.02bn) YoY. Breaking this down further, there was a 5.7% decrease in deliveries in Q1 2023 (as compared to a 6.25% increase during the same quarter last year) Furthermore, natural gas production amounted to 1.24bn m3 in Q1 2023, an increase of 0.73% compared to the plan, but a decrease of 5.4% compared to Q1 2023. Also, the amount of electricity produced was 323.04 GWh, which was 6.46% lower than the production in Q1 2022. Finally, national gas consumption is estimated at 38.72 TWh, a decrease of 12% YoY. Of this, Romgaz contributed 14.84 TWh, representing 38.3% of national consumption and 41.8% of consumption covered by domestic gas. As a result of these developments, revenue from gas sales decreased by 25.5% (or RON 877.3m), while revenue from electricity sales decreased by 62.2% (or RON 199.6m).

In terms of the expenses, they amounted to RON 1.2bn, a decrease of 56.5% YoY, mainly due to lower royalty expenses (RON 146.5m vs. RON 458.4m in Q1 2022), and lower windfall tax expenses from the gas sale activity (RON 476.9m vs. RON 1.84bn in Q1 2022), due to government regulation. In turn, this would mean that even though the revenue dropped by more than a quarter, the EBITDA improved significantly. As such, during Q1 2023 it amounted to RON 1.88bn, representing an increase of 53.5% YoY. This would imply an EBITDA margin of 64.7%, representing an increase of 33.47 p.p. YoY.

Moving on down the P&L, one interesting thing to note is the relative decrease (albeit minor, 1%) in net income. This came as a result of higher net income tax, which in total amounted to RON 815.5m, an increase of 329.7% YoY. Breaking this tax expense apart, we have the current income tax of RON 271.2m, deferred income tax of RON 6.8m, and the contribution to the solidarity fund in the amount of RON 537.5m, which was introduced at the end of 2022. As such, this significantly impacted the net income, which amounted to RON 970m, declining by 1%. Despite this, the net income margin did improve, amounting to 33.3%, representing an increase of 8.4% YoY, but this came mostly as a result of lower revenue, and as mentioned, not higher net income.

Romgaz key financials (Q1 2023 vs. Q1 2022, RONm)

Source: Romgaz, InterCapital Research

In terms of investments, in Q1 2023 Romgaz Group scheduled investments of RON 325.2m but managed to achieve RON 222.6m of total investments, meaning a reduction of 31.6% compared to the plan. Compared to the Annual Investment Plan (in the amount of RON 1.97bn), Romgaz carried out investments in the amount of RON 160.5m, or 8.1% of the total. Compared to the same period last year, investments increased by 77.8%. Of these investments, Romgaz noted several chapters, such as revamping and retrofitting of existing installations and pieces of equipment, geological exploration works, exploitation drilling works, environmental protection works, independent equipment and installation, and expenses with studies and projects.

Here you can find the dates for the upcoming events of the regional companies.

| wdt_ID | Date | Ticker | Announcement | Country |

|---|---|---|---|---|

| 43 | 30.5.2023 | ZVTG | Triglav Q1 2023 Results | Slovenia |

| 44 | 31.5.2023 | ADPL | AD Plastik Supervisory Board Meeting | Croatia |

| 45 | 31.5.2023 | DIGI | Digi 2022 Annual Report | Romania |

| 46 | 31.5.2023 | UKIG | Unior Q1 2023 Results | Slovenia |

| 47 | 31.5.2023 | POSR | Sava Re Q1 2023 Results | Slovenia |

Due to the nature of these events, they are subject to change (might be postponed or canceled).