Starting from today, we’ll start to get a feeling of how much central banks are willing to deliver on their promises to reactivate accommodative monetary measures. The ECB will probably just sketch out a plan of further action, while the FOMC takes the driver’s seat next week.

Inflation expectations in the developed markets have been steadily decreasing since the middle of last year, mostly thanks to slower GDP growth prospects brought about by trade wars, Brexit, and economic expansion entering late cycle. It’s curious to note that for instance EUR 5Y5Y inflation swap dropped all the way down from 1.75% (June 2018) to the current value of 1.29% (FWISEU55 Index on Bloomberg, available here as well). The slide was accompanied by a cyclical weakness in high frequency data, such as PMIs, manufacturing orders, etc. Here’s one interesting indicator of how the perception of economic weakness has been developing: in January the IMF expected German GDP to expand in 2019 by as much as +1.3% YoY; in April this forecast was already cut down to +0.8% YoY; the latest, July forecast puts the figure at merely +0.7% YoY. With the current setup of macroeconomic figures, it wouldn’t surprise us to discover that the German GDP had decreased on a YoY basis in the second quarter of 2019 (GDP data would be published on August 14th).

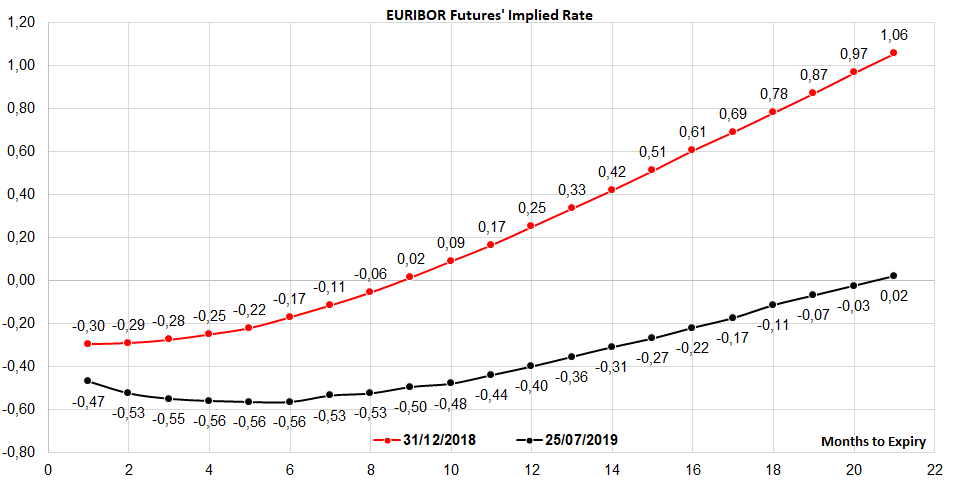

Here’s the funny part: although the growth slows down, the German DAX is up YTD by as much as +18.6%, while Eurostoxx increased by +17.71% since the new year kicked off. The underlying valuations are propelled by expectations of further accommodative measures in the developed countries that might be just around the corner. This is the reason why the financial markets will be listening closely to today’s monetary policy meeting – the interest rate decisions would be published at 13.45 CET, while the statement accompanied by Q&A session would be delivered at 14.30 CET. The chart submitted below (“EURIBOR Futures’ Implied Rate“) suggests markets are still unsure of which muscles the central bank plans to use, but it’s quite possible that a mix of interest rate cuts, asset purchase, and tiering might be introduced to sustain economic expansion and possibly revive inflation expectations higher. The recent central bank speak has been inclined to reviewing the inflation goal, and to understand it here’s a bit of a history lesson.

The EU Treaty only requires the Frankfurt-based institution to “maintain price stability”, without closely defining what that actually means. Until 2003 this objective was interpreted by ECB as keeping inflation below 2.0% figure, and then in 2003 the objective was changed to keeping it “below but close to 2.0%”. The change was decided behind closed doors and contributed to the perception of the ECB as an arcane, autistic institution. Sixteen years later another change in ECB policy might be around the corner, and this time the Chair of the GC pushes for “symmetrical” approach, meaning that the economists in charge could let the inflation move above 2.0% in the short run in order to ensure the stability of price growth.

During the secular period of sluggish inflation numerous ex-central bank officials have suggested different solutions for reviving inflation. For instance, ex-IMF Chief Economist Olivier Blanchard advocated moving the goal from +2.0% to +4.0%, but the ECB has spent the last 20 years building up credibility for being consistent to it’s inflation goal; merely changing the figures might cripple this credibility since it sends out a message that goals would be changed if their start to appear unattainable.

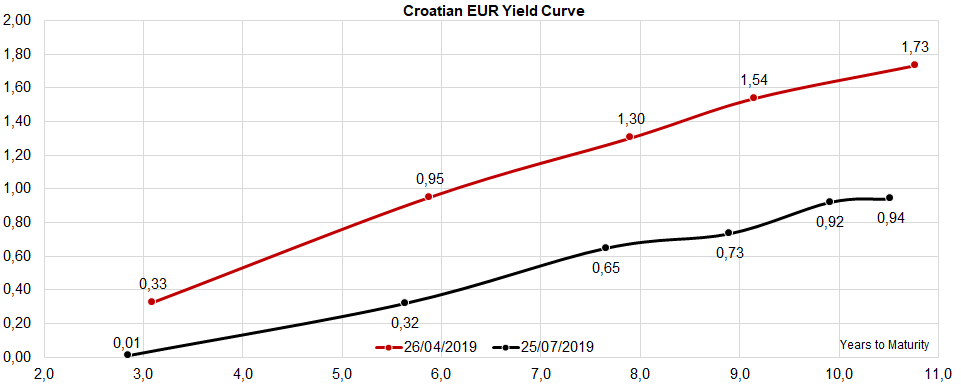

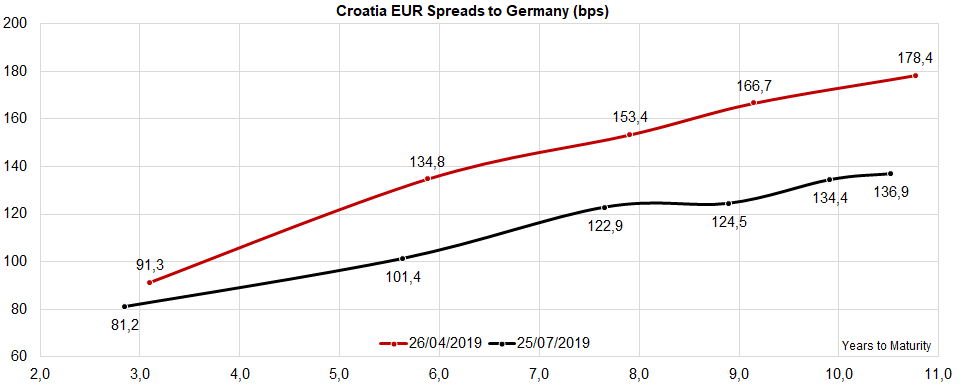

Our baseline scenario for today’s ECB Monetary Policy meeting is that nothing changes in terms of interest rates, but ECB starts sketching out a plan for the introduction of monetary stimulus, expected to be enacted in September. The effects are visible across the board: the euro dropped by about 150 pips in one week’s time, Bund trades at -0.39% YTM, while EURIBOR futures expect a 10bps rate cut in the near future. The effects are spilling over into EMs such as Croatia, although the contraction of the spread also has roots in a shift in credit rating, as well as expectations of entering ERM II as soon as next year. A couple of years will certainly go by before the ECB can purchase Croatian Eurobonds, but the portfolio effects are already here, warranting further contraction of CROATI risk premiums.

Telekom Slovenije published their H1 2019 results yesterday, showing a 5.4% YoY decrease in sales, while EBITDA grew 11.3% YoY & net profit was up 34.7% YoY to EUR 19.6m.

Telekom Slovenije published their H1 2019 results yesterday, showing a 5.4% YoY decrease in sales which amounted to EUR 340.6m. However, one should note that revenues in 2019 no longer include the revenues generated by Blicnet, which was sold in 2018. Meanwhile, revenues from mobile merchandise on the end-user market and revenues from the fixed segment of the end-user market were down in 2019, primarily due to the completion of the project to set up an electronic toll collection system in 2018, and down were also revenues on the wholesale market.

OPEX are down 7.8% YoY as the introduction of the IFRS 16 played an important role in the company’s result. Due to the change in the recognition of costs, the costs of services incurred by the Telekom Slovenije Group were down by 15% or EUR 23.3m. However, one should also note that all expenses were down (except D&A). As a result, EBITDA went up 11.3% YoY, amounting to EUR 112.3m.

Due to the above mentioned, the bottom line improved by 34.7% YoY to EUR 19.6m, despite the deterioration of the company’s net financial loss which doubled when compared to H1 2018 and ended at HRK -2.5m (+137% YoY).

Turning our attention to the balance sheet, the company’s net debt is up 3% since the beginning of the year and now amounts to EUR 378.6m. However, as this translates to 1.92x net debt/EBITDA one can still consider the company reasonably indebted.

One should also note that, in accordance with Telekom Slovenije’s strategy for the period 2019–2023, the company began activities to sell its 100% participating interest in IPKO Telecommunications LLC in Kosovo. However, further detail regarding the sale were not given.

In H1 Kraš posted a 4.1% YoY increase in sales, meanwhile EBITDA is up 1.1% YoY, while net profit amounted to HRK 11.6m (+12.8%).

Kras published their H1 2019 results yesterday, showing a 4.1% YoY increase in sales. Breaking down the company’s top line result, Kras managed to somewhat evenly distribute their sales with domestic sales amounting to HRK 241.7m (53%) and foreign to HRK 216m (47%). In value domestic sales went up 2.8% YoY, while foreign sales went up 5.5%.

EBITDA rose slightly, amounting to HRK 40.3m (+1.1%), while EBITDA margin decreased slightly to 8.7% (-0.3 p.p.). The slim increase in EBITDA can be attributed to rising OPEX which went up 4.1% (just like sales), due to the higher volume of production along with higher prices of certain strategic materials (cocoa, dairy products & candy syrup). However, employee expenses witnessed the highest increase as they went up by 11% YoY.

Below the operating line the company also benefited from an improved net financial result which amounted to HRK -1.2m (-45% YoY). Finally, net profit amounted to HRK 13.9m, representing an 11.2% YoY increase.

According to the report, Kras began their investment cycle at the begging of the year with the aim of improving the technical and technological capabilities of their production plant which will further increase the quality of the company’s final products. As a result, the company’s CAPEX in H1 2019 amounted to HRK 39.3m (+296% YoY).

Optima Telekom published their H1 2019 results showing a flattish top line performance, EBITDA up 19.2% YoY & net profit of HRK 5m (up from last year’s loss of HRK -3.3m).

Optima Telekom released their H1 2019 results yesterday, showing a flattish top line performance as sales amounted to HRK 265.4m (-0.2% YoY). The revenue decrease was mostly caused by a decline from public voice service (10.4%), which has been a global trend for some time now. The effect of these revenues decline was offset by increased interconnection revenues of 11.4%, which is a consequence of an increased volume of low profit international transit, as well as an additional revenue increase from selling equipment and ICT services. Furthermore, there was a slight growth in multimedia revenue of 2.7%, which is alongside Internet one of the two mediums in the focus of the company’s business operations. It is also worth noting that the decrease in revenues from public voice services was significantly lowered in Q2, amounting to just 0.5% (from 4.3% in Q1). Meanwhile, when observing the revenue on a half-year basis, the decrease in revenues from data services is 2.4% lower when compared to the same period last year.

When observing the company’s EBITDA (before one time items after lease), it amounted to HRK 62.5m, which represents an increase of 19.2% YoY. According to the report, for the most part, this is a result of the business operations cost optimization. Note that this EBITDA represents an operational result which is neutralized with IFRS 16 effect. Going further down the P&L, the company reported an increase in EBIT by 130.9% YoY, amounting to HRK 20.6m.

As a result, net profit surged, turning the net loss recorded in Q1 into a net profit of HRK 5m. Furthermore, the improvement is very visible on a YoY basis as well since the company ended H1 2018 with a net loss of HRK -3.8m

Turning our attention to the balance sheet, the company’s net debt amounted to HRK 405.5m (+11.6% since the beginning of the year) which can be attributed to the new debt caused by the introduction of the IFRS 16. If one was to exclude the new lease liabilities, net debt would actually be down 2.7% since the beginning of the year.

In H1 2019 CAPEX amounted to HRK 46.3 million, out of which HRK 14.1m. The mentioned amount was invested in user equipment for providing service to residential and business users. Investments in building optical infrastructure, access network and core network amounted to HRK 9.4m, while HRK 22.8m was invested in expanding of user service and IT system. Within network building, there is an integration of new Internet hub in the Optima Telekom network which also consists of 100Gb/s interfaces. These will enable interconnection with transport networks as well as with networks of other operators with 100Gb/s in the near future.