As of end February, total financial institution’s loans amounted to HRK 275bn, which represents a 4.4% increase YoY.

Croatian National Bank (HNB) published their monthly statistical report on loans placement of other monetary financial institutions. According to the monthly statistical report as of end February, total financial institution’s loans amounted to HRK 275.04bn, which represents a 4.4% increase YoY and a decrease of -0.5% MoM. Such figures do indicate that credit activity, especially certain segments, showed very solid resilience during the pandemic.

Its biggest categories household loans and corporate loans evidenced growth of 1.9% YoY and 4% YoY, respectively. On a monthly basis Corporate loans have once again started seeing slight increases for the 3rd consecutive month (+0.27% MoM) and ended February at HRK 87.1bn.

It is also worth adding that loans to central government witnessed sharp increase of 10.9% YoY to HRK 40.9bn, which was mostly evidenced with the beginning of the pandemic. To be specific, this relates to a HRK 6bn loan to the state (for Covid-19 support) which occurred in parallel to HNB reducing the required reserves for banks freed additional funds. Meanwhile, loans to local government amounted to HRK 6.6bn, representing an increase of 34%.

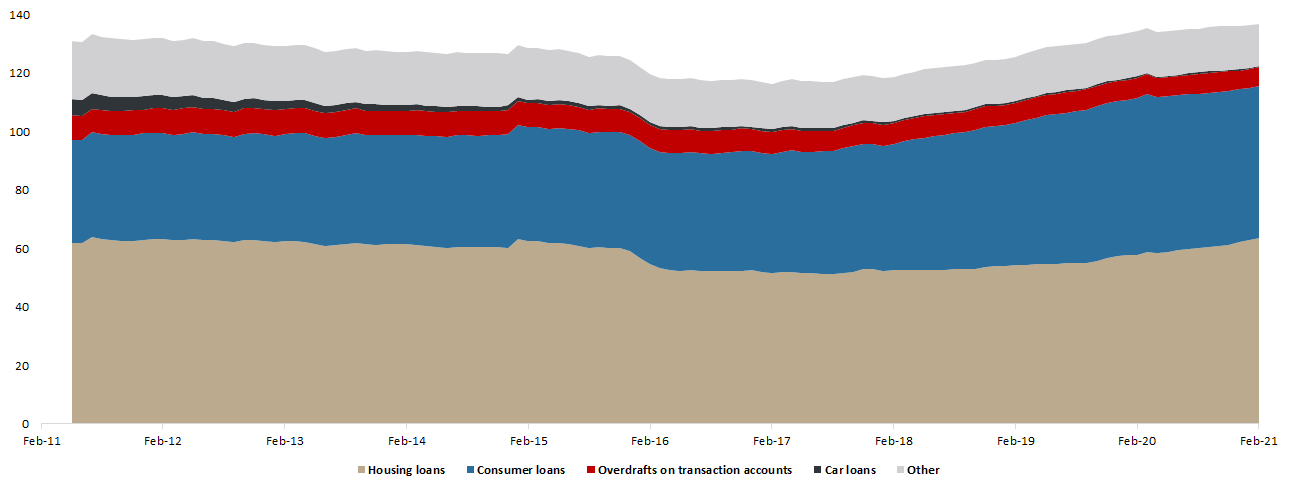

Total loans issued to households amounted to HRK 136.9bn, representing an increase of 1.9% YoY (or HRK 2.6bn). Such an increase was almost entirely driven by a rise in housing loans (+9.7% YoY or HRK 5.6bn), while being somewhat offset by almost every other segment. The second largest item within household loans – consumer loans, did eventually see a slight YoY decrease of 2.9%, or the highest absolute YoY decrease of HRK 1.55bn. We note that these two items account for 84% of the total Loans to Households.

The largest relative YoY drop was witnessed in car loans (-24.7% or HRK 127m).

Loans to Households (HRK bn)

If we were to compare total loans issued to households since the beginning of the pandemic, one can notice a slight increase of 1.1% or HRK 1.53bn. Such an increase could mostly be attributed to a still solid performance of housing loans by 7.9% or HRK 4.63bn, which was partially offset by a 3.4% decrease in consumer loans (or HRK 1.85bn).

Trading statistics for March 2021 show an average daily turnover of EUR 1.5m (-49% YoY). Meanwhile, SBI TOP ended the month with a solid increase of 2.55%.

The Ljubljana Stock Exchange (LJSE) published their trading statistics for March 2021, showing an equity turnover of EUR 34.7m. This translates into an average daily turnover of EUR 1.5m (-49.2% YoY). Such a high decrease could be attributed to a selloff which occurred in March of 2020.

Of the total value traded in the period (excluding block transactions), Krka generated EUR 16.6m (or 53%), followed by NLB Group with EUR 5.3m (or 16.8%). Next come Sava Re with EUR 2.2m (or 7%) and Triglav with EUR 1.9m (or 6.1%). Petrol follows with EUR 1.7m or (5.4%). These 5 shares generated 88% of the turnover recorded by the entire (equity) market.

When observing the total equity market capitalization, it observed a 3.2% MoM increase and currently amounts to EUR 7.52bn.

The main equity index of LJSE observed a very solid 2.5% monthly increase, ending March at 990.21 points. Of the SBITOP constituents, Telekom Slovenije leads the list with an increase of 7.3%. NLB and Petrol follow, with a solid increase of 6.8% and 3.6%, respectively. Krka, as the index heavyweight showed an increase of 2.4%. On the flip side, Sava Re observed a slight decrease of 0.9%.

We also note that SBITOP observed a high increase of 10% in Q1. The last time that the index observed such an increase in Q1 occurred back in 2007.

Performance of SBITOP Constituents in March 2021 (%)