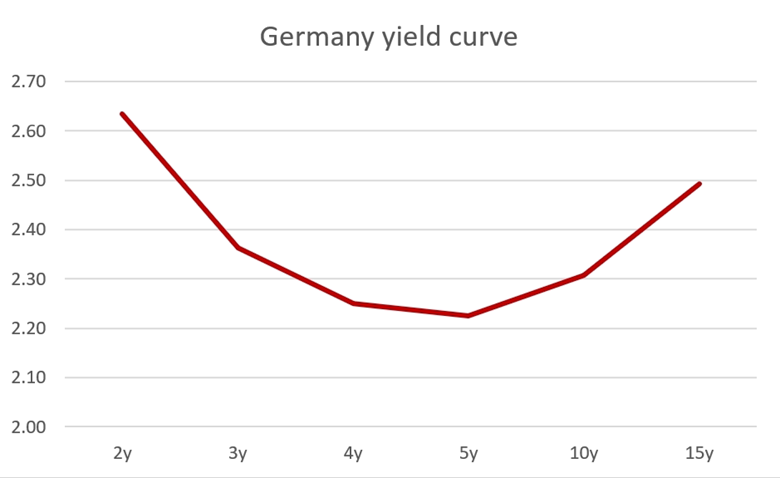

Central banks raised interest rates during the last two years which mainly affected the short end of the yield curve. Schatz (German 2-year bond) entered 2022 with a yield of -0.611% and closed 2022 at 2.764%. Schatz peaked on March 9th last year when it was at 3.382% and today Schatz is at 2.665% with yields falling mainly in the last two months. In the meantime, Bund entered 2022 at -0.570% and closed the same year at 2.571%. Bund peaked on October 4th, 2023, at 3.026% and today is at 2.312%. In this part, we will consider trading a steepening of the yield curve through the 2-10y.

As stated above, today we mainly have inverted yield curves in the EU and in the States. Last month central bankers started to talk about cutting interest rates during 2024 what already reflected in yield curves, so this should be a good moment for trading steepening of the yield curve (i.e. yields on the short end becoming lower than yields on the long end). Yield curve steepening can happen with three different events:

- Yields on the short end are falling faster than on the long end.

- Yields on the short end are falling, while on the long end, they are rising.

- Yields on the short end are rising, while on the long end, they are rising much faster.

Inflation came close to the 2% target, PPIs (i.e. inflation that producers of goods have on their entry of materials) are in Europe in negative territory at -8.8%, while in the US last PPI was 1.0%, the price of energy returned on levels before COVID and war in Ukraine. All those reasons are deflationary. To be fair, on the other hand, we have strong employment that is inflationary per se, but we still see inflation near the 2% target during 2024. Consequently, central banks should cut rates through 2024 when the short end must react and close on lower yields. So, it seems obvious to trade the steepening of the yield curve during 2024.

A simple way to trade the steepening of the yield curve is with futures. The crucial thing is to adjust the duration in total of the short end with the long end. If we think that the steepening of the curve will happen, then we expect one of the three cases that we stated above and to cover all those scenarios we go long the short end and short the long end. Because the short end has a much smaller duration, we must buy more futures on the short end so that the sum of all these durations is equal to the sum of the durations on the long end. We want to be duration-neutral so that the same move in yield on both ends (the whole curve goes up/down for the same amount of bps) doesn’t generate loss.

Example 1. With the <FIHR> function on BBG, we find that at this moment for long 100 futures of Schatz (DUA), we need to sell 18 futures of Bund (RXA) so that we are duration neutral. If we are constantly duration-neutral, on the constant spread of 2-10y, our P&L is also constant. (Here we don’t consider the impact of the cheapest-to-deliver bond on futures.)

With trading the steepening of the yield curve, we should always stay duration-neutral so that we are not exposed to other factors. The first problem is that a duration changes with movements in yields. Nominally, the same movement in yield on both ends will result in the spread staying on the same level, but the duration will change and then the long end will have bigger movements.

Example 2. Let’s look at DUA and RXA, currently cheapest-to-deliver bonds for those futures are BKO 3.1 12/12/25 (YTM 2.674%) and DBR 2.3 02/15/33 (YTM 2.262%), spread is 41.2 bps. The duration is 1.805 and 7.919, respectively. If we change YTM for 500 bps on both bonds (7.674% and 7.262%), the spread is still the same as before, but the new durations are 1.720 and 7.279. After this move, the proper duration-neutral position is long 100 futures on the Schatz and short 32 futures on the Bund.

The last example shows that it is not enough just to look for the spread 2-10y in a trading of a steepening of a yield curve, but the actual movement in yield matters also.

While trading a steepening of a yield curve with futures, a trader should make a position duration-neutral after every greater movement in a yield on any end.

Source: Bloomberg, InterCapital

InterCapital Asset Management to list ICBET and ICASH on the Ljubljana Stock Exchange, trading to start on 23 January 2024.

Ljubljana Stock Exchange has announced the listing of two new open-end funds on its website, the ICBET (BET ETF) and ICASH (Money market ETF), by InterCapital Asset Management. Both ETFs will start trading on 23 January 2024.

But before we get into the specific ETFs, we will emphasize the key benefits of owning an ETF:

- Diversification – the single biggest advantage of owning an ETF is the instant diversification you get just by owning “one” product, at the cost of only that specific single product

- Liquidity – ETF trades on the stock exchange and can be bought/sold throughout the trading day at market prices

- Transparency – Provide transparency into the assets they hold. You can usually see what’s in the ETF on a regular basis.

- Low cost – Typically have lower expense ratios compared to mutual funds.

- Tax benefits – Dividends that the ETFs receive are usually not taxed (or at taxed at lower rates).

ICBET

The Romanian economy has been on a slow and steady growth trajectory since its entrance into the European Union in 2007. Supported by the ever-increasing amount of EU funds and a goal of convergence with the rest of the EU. Through this, the Romanian economy has many opportunities for continued growth. In this environment, the Romanian stock market also expanded, attracting more and more investors, both institutional but also retail.

As a reminder, InterCapital’s ETF that is tracking BET (Romanian index) and Money market ETF have already been trading on the Zagreb Stock Exchange (ZSE) for a part of the previous year. Since the listing (during June 2023!), 7 BET reported a strong double-digit return of 27.8% for each investor that chose to expose its portfolio to the Romanian stock market. And only to remind you, all by owning “just” one, already diversified, security in your portfolio. Romanian stock markets is particularly interesting, even after the aforementioned returns, as Romania might soon become a so-called “Emerging market” (from the current status of “Frontier”) on the back of Hidrielectrica’s listing. Further, around 50% of BET’s weight currently comes from the Energy sector. However, even with Energy making the majority of its weight, we should not forget the Romanian banking sector as a heavyweight.

ICASH

Money market ETFs became very popular in the last three years due to their liquidity advantage. Those kinds of ETFs have lower management costs compared to other classic funds, they are very liquid and transparent. Finally, in the environment of higher interest rates (both from Fed & ECB) they offer attractive yields.

InterCapital’s ETF, 1st money market of its kind in the region, invests in short-term securities of the highest quality issuers from the eurozone. The ones that enjoy a high credit rating. ICASH offers a solid opportunity for an investor wanting short-term securities in their portfolio, especially during the current times of high-interest rates – making him more appealing than usual. Currently app. 72% is invested in Treasuries issued by France, Belgium, Germany and the Netherlands, while the rest is invested in money market instruments or reverse repurchase agreements of bonds. Finally, as with every ETF so far (IC CRO, IC SLO & now IC BET), if an investor is invested in a fund for more than two years, he is exempt from taxation.

Overall, an investor on the Ljubljana Stock Exchange will gain an opportunity to expose its portfolio to both the Romanian stock market & Money market on a cost & tax-efficient basis.

7BET performance on ZSE [since listing]

Source: Bloomberg, InterCapital Research