On August 17th, 1997 Russian government published its decision to devalue the ruble and postpone domestic debt payments. This ignited a chain of events that in the end caused the collapse of notorious Long Term Capital Management. The genius had failed. On this notorious 25th anniversary Japanese bond auction flopped, precede by an Australian flop and against the backdrop of superficially hawkish FED minutes. What do we make of these events, as well as how do we see the latest Croatian T-bill auction – find out in this brief research piece.

Minutes from the latest FOMC meeting published yesterday afternoon reveal that US rate setters no longer expect the US economy to enter recession, however, they do see upside risks to inflation and are aware of the fact that additional tightening might represent additional slowdown risks. “A gradual slowdown in economic activity … appeared to be in progress …”; on the other hand, inflation is still unacceptably high and requires more tightening ahead (hence the hawkish tilt you might have already read about). Some bits of data such as lower short-term inflation expectations and weaker core goods’ prices point in the direction of inflation gradually cooling off, but there wasn’t enough evidence in the hard data to point out in the direction that FED’s job in curbing inflation is done. Our reading of the statement is neutral because CPI/PCE figures are both pointing to the downside and even core prices are cooling off, albeit at a gradual pace (too gradual for the FED?).

Here is where the story turns bad. Asian trading session started off with a sharp sell-off in Australian bonds – take a look at the YTM of ACGB 3 11/21/2033 which yesterday peaked at 4.32%. Why is this so odd? Well first of all, the rise in Australian yields came against the backdrop of an economic slowdown in China (Australia’s largest trading partner) and an unexpected drop in employment/rise in the jobless rate. In other words, hard data points in the opposite direction compared to the one that bond yields took. One of the notorious explanations for such a move is the fact that the Japanese bond auction tanked, a move coupled with a sharp rise in USDJPY.

And with this, we arrive at the main course of this research piece. Japan placed some 2.92tn JPY 1Y paper at -0.0679%. That’s right, Japan is still placing bonds at negative yields – as a matter of fact, if you check out the BNYDMVU Index on Bloomberg terminal (market value of aggregate global negative-yielding debt in USD), you can see for yourselves that all of the remaining negative-yielding debt is in Japan. And yes, even in a world like this there is still approximately 673bn USD. Just for a bit of context here – the peak was recorded in December 2020 when the figure stood at 18.4tn USD. But back to the main story – even with the negative yield to maturity on 1Y paper, the auction recorded a bid-to-cover of 2.87x, the lowest value in almost a year. The same happened on the 20Y paper as well, which recorded a bid-to-cover of 2.80, also a 1Y low. Naturally, USDJPY skyrocketed (currently at 146.24) and for the time being, everybody is expecting the BoJ to switch from talking the talk to walking the walk and kick off FX auction intended to stabilize the exchange rate. The question of the day remains whether Japanese investors would now switch away from their holdings in French and Australian paper and back not JPY bonds, causing European bonds to sell off as a result. As a matter of fact, European investors are bracing for this.

In times of rising yields across the board, a funny thing happened on yesterday’s Croatian T-bill auction. Against today’s maturity of RHMF-T-333B (146mm EUR), the Ministry of Finance managed to collect 22 bids with an aggregate value of 533.95mm EUR, testifying to the strong demand of money markets. The problem was that investors were looking for returns in the range of 3.30%-4.10% and the Ministry of Finance rejected all of the bids in quite an unexpected move. Instead, the Ministry placed 12.5mm EUR of 6-month paper at 3.20% (only one bid was successfully filled) against a total of 19.59mm EUR of aggregate bids ranging from 3.20% to 4.00%. We were asked by a number of clients what do we make of this since the previous 1Y T-bill auction went by with a 3.50% YTM, so investors were hoping for at least an equal yield. We note that the Ministry of Finance was signaling that it’s time for the placement of retail T-bill, but we are still unaware of the progress made to build the market infrastructure necessary to place a retail short-term paper in meaningful size. The retail bond placed in early March was a great success indeed, but the preparations took nearly a month to be completed. Besides that, CROATE 3.65 03/08/2025€ has a liquid secondary market and it’s listed on the stock exchange, assuring mom-and-pop investors they can get out at any time and at a predictable price with negligent transaction cost. This is still missing on the T-bill market, albeit we were informed that the Ministry is pushing in the direction of building the necessary infrastructure. Meanwhile, institutional investors that are feeling stood up at yesterday’s auction are looking for alternatives in core euro countries. DBR 1 08/15/2024€ (1-year German paper) is trading at roughly 3.40% YTM, while French paper of equal maturity could be fetched at about 3.65% YTM. Nevertheless, institutional investors are smart enough not to wait for the reversal of Japanese bond flows away from French paper and back into their home currency – because that takes too long, and smart money needs to be invested now.

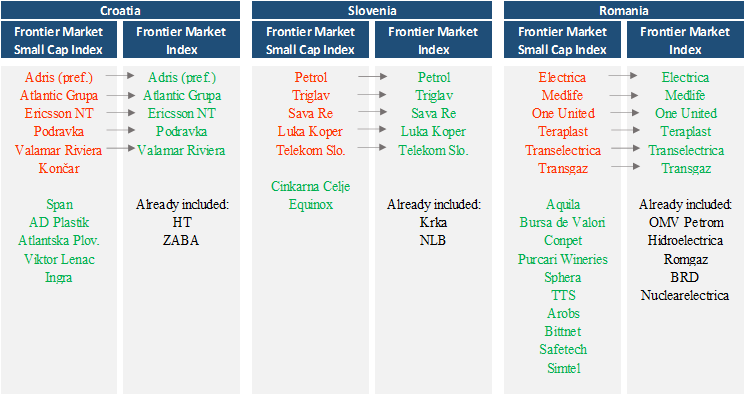

MSCI, the best known for its series of stock indices that provide a benchmark for many ETFs and mutual funds, has recently published its regular revision. The revision is favoring our region regarding its visibility for Croatia, Slovenian and Romania in the form of new representatives in MSCI’s Frontier Index.

MSCI, the largest provider of stock indices globally and best known for those series of stock indices being a benchmark for many ETFs and mutual funds, has recently published its regular revision. In a recent publication of its regular revision, MSCI has decidedly shed light upon our region and its potential for Croatia, Slovenia, and Romania (among others). This strategic move is manifested in the form of new entrants into MSCI’s esteemed indices, a recognition, which might bring an unlocking substantial value through recognition. The changes will take place as of the close of 31 August 2023.

In short, MSCI divides frontier market into two main categories that enter the Frontier Market Index: Frontier Small Cap Index and Frontier Market Index, which is composed of companies with even higher market capitalization compared to Small Cap.

With that said, if a company is on any of these lists, it makes it „investable“ in the eyes of asset managers and investors. Additionally, special attention is paid to the companies listed on Frontier Market Index (read: not in Small Cap index). Companies like the aforementioned might be included in passive ETFs that track MSCI Frontier Market as its constituent. However, we note that this will also act as a catalyst for easier passing of investor’s screening when looking at region! The changes will take place as of the close of 31 August 2023.

Which companies are being included?

Let’s look at these changes with regard to the country as a whole. After the changes take place. Croatia will have 12 „investable“ companies (+4 companies overall), while 5 companies will enter the Frontier index (from a previous Small Cap Frontier).

Slovenia will have 8 investable companies (+1), while 4 companies will enter the Frontier index (Krka and NLB are already part of the Frontier index).

Romania will have 16 investable companies (+10!), while 6 companies will enter the Frontier index.

Source: MSCI, InterCapital Research

In conclusion, MSCI’s recognition of Croatia, Slovenia and Romania through more companies being included in MSCI’S Small Cap and Frontier index implies increasing economic prominence. We are eager to witness the unlocking of value that this deserved recognition of the region may bring!