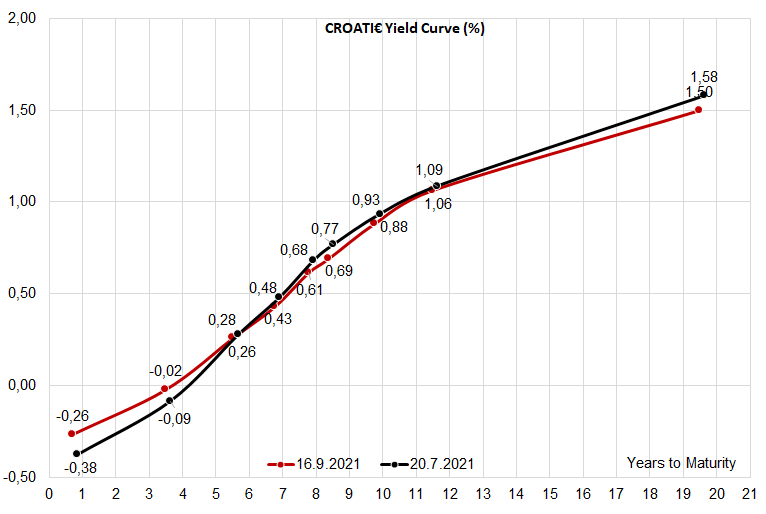

It’s early autumn, but it’s quite hot and we’re not talking about temperature. 30Y Hungarian USD bonds placed on Tuesday managed to pull off a three big figure price increase in a matter of a couple of hours. You don’t see that every day, but more placements from CEE are coming up. Find out more in this brief research piece.

European bulge bracket banks have been signalling strong September in terms of sovereign placement and they were right – first half of the month has been quite strong in terms of both EGB placements, as well as guidance on expected placements. Hungary made a big splash on Tuesday and Wednesday placing a total of 4.6bn EUR in three tranches (two USD, one EUR). There’s a lot to unpack here so let’s take it step by step.

The story about the largest Hungarian Eurobond placement up-to-date actually started in mid-July. Back then Prime Minister Viktor Orban communicated with the press that the delay in RRF disbursements caused by wrangling with EU institutions over LGBTQ rights might warrant bond placements in order to bridge the cash gap so that no projects are on hold (link). Stronger than expected GDP growth allowed the country to tap the international markets without breaking the self-imposed 20% limit in FX debt. Also, although Hungarian broad retail base was providing strong and regular sources of funding for the central government, the relative unpredictability meant the only way PM could have a good night’s sleep in the coming months meant tapping the international markets. On Monday the AKK (Hungarian debt management agency) held a brief road show and on Tuesday the orderbook was open for a dual USD tranche.

On Tuesday morning it was clear that Hungary was going for 4.5bn EUR placement (the largest in the countries history) and decided to put through three or four tranches. The first two tranches were USD-denominated 10Y and 30Y maturities. From issuer perspective, the big perk of USD placement instead of euro lies in much tighter spreads, which are in larger part caused by FED undergoing a standing REPO facility, while on the other hand ECB hasn’t allowed much clarity on what exactly the word “recalibration” means (we’ll probably have to wait for December to figure that one out). To get a hold on the difference in G-spreads between the USD and EUR curve, take a look at where REPHUN 3.125 09/21/2051$ is traded (bid 98.236 clean, 3.217% YTM, T 2.375 05/15/2051 @ 1.866%, 135bps spread to Ts) as opposed to “old” REPHUN 1.5 11/17/2051€ (bid 93.21 clean, 1.8% YTM, DBR 0 08/15/2050 @ 0.20%, 160bps spread to Germany). Some research analysts have been pointing out that in case of EUR paper, the benchmark used to calculate the spread should be put on EU debt (EU 0.3 11/04/2050 @ 0.472%, for instance, putting the R1.5 11/17/2051€ spread to 133bps) but for now let’s stick to traditional G spread calculation. Either way, Hungary allowed itself to tap the deep US financial markets which has been growing hungry of new CEE placements and the size of the book size tells a story of its own.

On Tuesday morning the IPTs in our mailbox indicated T 1.25 08/15/2031+130bps for REPHUN 10Y$ and T 2.375 05/15/2051+180bps for the REPHUN 30Y$. Fair values were calculated at about 97.5bps and 127bps, respectively, and nobody was really expecting the country to place at spreads this wide. Veteran traders remembered that the last dual tranche placed by Hungary went with 25bps tightening and this time around AKK also got some extra tailwind in form of US CPI coming weaker than expected. The combined orderbook swelled to 15.5bn USD, AKK decided to place 4.25bn USD (implying a bid-to-cover of 3.65x) and allegedly the books were full of dedicated EM orders (in dealers’ terms: real money accounts). With fast money accounts getting only scraps, the grey market price basically had only one way to go, which is up. Placed at a clean price of 95.873, the bid on new REPHUN 3.125 09/21/2051$ went as high as 99.25 on Wednesday morning (wow! +338 cents, remember that to tell your grandchildren!). For an hour or two during the morning run there were no sellers. This is the reason the few fast money accounts that actually got allocated called this placement an early Christmas gift.

With about 3.6bn EUR in their pockets (4.25bn USD / 1.18 = 3.6bn EUR) AKK decided to take it easy on Wednesday and put through a 1bn EUR WNG 7Y. With NIP once again cut to the bone, books again swelled to over 4.8bn EUR indicating an even better demand. However, rumour has it the quality of the book was trailing the USD placement and this time fast money managed to get in and get allocated. We still believe that even brand new REPHUN 0.125 09/21/2028€ might have room for price increase because from our understanding most of the Hungarian local accounts couldn’t take part in the placement. They would probably buy today because REPHUN 1.75 10/10/2027€ is quite hard to find and new REPHUN 0.125 09/21/2028€ offers a decent roll down return for a relatively safe duration.

Hungary is clearly done with funding for some time. Next CEE countries on our radar that might tap the international financial markets are Poland, Romania, Albania and Bulgaria. At least two among them are clearly thinking about placing USD paper and with spreads at these levels, they would probably follow through with greenback bonds.

Today, we decided to present you with a brief analysis of cash per share of Slovenian companies.

After Slovenian companies published their 1H reports, we decided to present you with a cash per share analysis. The analysis is done to see the strength of the balance sheet and how liquid selected Slovenian companies are. This figure as the percentage of a company’s share price can give us more insight into the company’s strength on returning the money to shareholders (either through dividends or buybacks), paying down debt etc.

Cash per share of Slovenian Blue Chips

It is important to note that looking at solely cash per share of a company could lead to misleading conclusions without also taking into consideration the company’s indebtedness. To read about the indebtedness of Slovenian blue chips, click here.

A high level of cash per share indicates a solid performance of the company, reinsuring the shareholders that the company is operating with “enough room” to cover for any potential difficulties and that the company has adequate capital.

Cash per share as a % of share price

As visible in the graph, of the selected companies, Cinkara Celje operates with the highest cash per share as a percentage of their current share price of 15.90% and cash per share amounted to EUR 38.47. Luka Koper comes next with 15.48%. On the flip side, Telekom Slovenije has the lowest cash per share as a percentage of current share price (4.40%).

In the graph below you can see the cash position of selected Slovenian companies as of end June 2021. As visible from the graph, only Krka breached the EUR 100m mark with little above EUR 450m.

Cash position of Slovenian Blue Chips (EUR m)

As of August, Fondul’s NAV reached RON 11.03bn (+5.84% YoY).

According to the latest NAV report (31 August 2021), Fondul reported a total NAV of RON 11.03bn (EUR 2.24bn), which translates into a NAV per share of RON 1.8691 (EUR 0.3788).

When comparing it to the same period last year, their total NAV recorded an increase of 5.84%, while NAV per share is up by 16.38% YoY.

Fondul Proprietatea’s portfolio structure remains largely oriented towards the power utilities generation sector (54.75% of NAV) and oil and gas sector (15.81% of NAV), which is why the two largest holdings, Hidroelectrica and OMV Petrom account for 70.56% of the total NAV.

In terms of the Fund’s portfolio structure, unlisted equities make up the majority, accounting for 77.11%, which represents an increase of 13.18 p.p. YoY. Listed equities follow with 18.21% (-25.79 p.p. YoY), while net cash and receivables account for 4.68% of the structure (-36.15 p.p. YoY).

The discount to NAV per share currently stands at 2.63%.