S&P Global Ratings will be reviewing Croatian credit rating this afternoon and domestic investors believe that by Monday morning Croatia might be at A- with a neutral outlook. To quote a popular song from The Cure – “Friday never hesitates“. Nevertheless, we think it’s a coin toss decision. But we know one thing – have Croatian bond prices already priced this upgrade? Is CROATI€ already in the closet A-? Read in this brief research piece.

S&P Global Ratings is scheduled to review the Croatian credit rating this afternoon and the domestic investment community is broadly aligned with rating being lifted from BBB+ (positive outlook) to A- (neutral outlook). Last rating review took place on September 15th, 2023 and staff stated that credit rating could be revised upwards in the following 12 months if „economic resilience is sustained, supported by the country’s deepening integration with Europe, and facilitated institutional improvements, for example within the judiciary, education, and broader business environment“. Let’s take it step by step.

Speaking about economic resilience, the rating agency expected real GDP growth to reach +2.5% (2023), +2.3% (2024), +2.8% (2025) and +2.7% (2026). The 2023 and 2024 figures are slightly below the forecasts put forward by the European Commission, which expects +2.6% in both 2023 and 2024. The rating agency also expects general government gross debt to be reduced to 60% GDP by 2026, but notice that Croatian public debt ended 2023 at 64% GDP and it’s quite likely that it will drop quite close to 60% GDP by the end of 2024. Additionally, EU fund withdrawals, excellent tourist seasons and strong government consumption spell real GDP growth rates above +2.5% in the near future, so the possibility of outperformance is quite evident. Moreover, the Croatian Ministry of Finance is issuing more and more retail instruments, increasing the share of domestic investors.

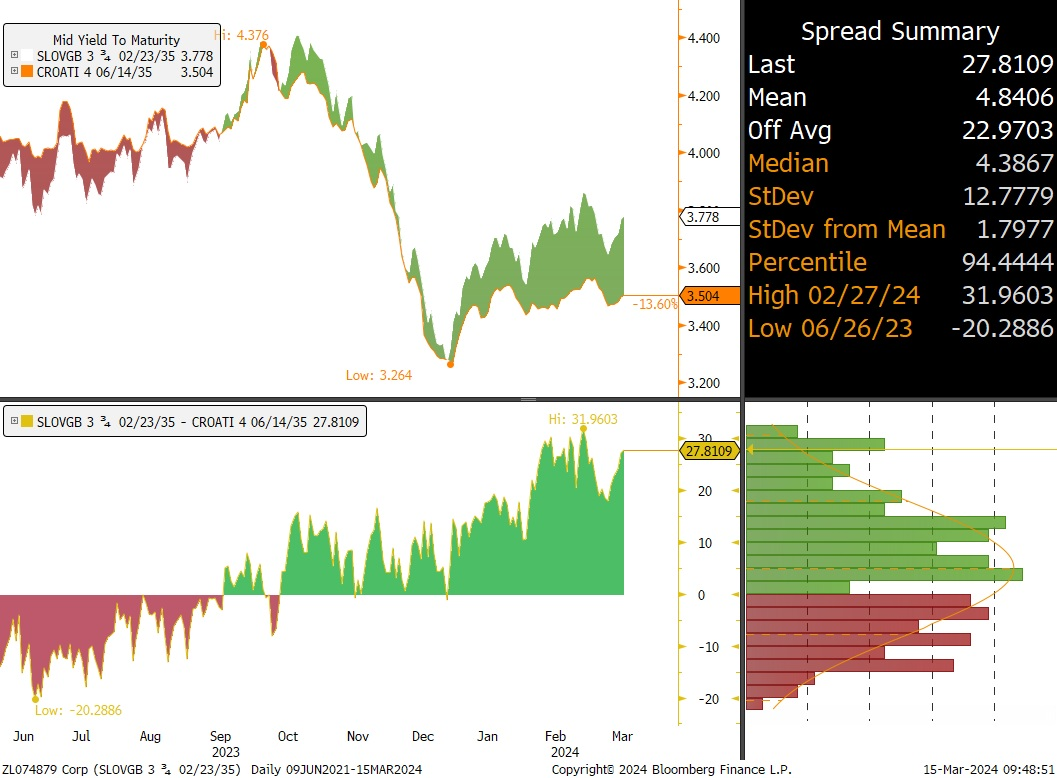

There are downside factors to the review as well, such as the assessment of judiciary independence, however, we do believe that the positive factors offset the negative ones. Needless to say, Croatian bonds have been behaving in a way that suggests that a rating upgrade might be in the cards this year. If you doubt that, just take a look at the spread between SLOVGB 3.75 02/23/2035€ (A+/A-/A2) and CROATI 4 06/15/2035€ (BBB+/BBB+/Baa2; notice that all three rating agencies hold a positive outlook). Slovakian bonds are traded at +27bps in terms of YTM compared to CROATI€ and it’s easy to know why. Markets are really expecting that rating upgrade, but the real question wee need to ask ourselves is – are the prices already reflecting A-? Is Croatia already “in the closet” A- country?

There are pros and cons for this story. If you believe liquidity on Croatian international bonds resembles SLOVGB€, you are right, the consequential spread tightening has been priced in and a hypothetical rating upgrade will be a non-event. On the other hand, take a look at SPGB 1.85 07/30/2035€ trading around 3.30% YTM (A/A-/Aa1). Spanish bonds are a lot more liquid compared to Croatian and the spread between the two is 20bps. Now here’s the kicker – Croatian yields are poised halfway between Spain and Slovakia. Markets tell it all – the liquidity is slightly better than Slovakia, but slightly worse than Spain, so it’s priced halfway in between. Notice that this has nothing to do with creditworthiness, but rather with the width of bid-ask spreads and the easiness of executing bigger orders.

The last thing you have to keep in mind are the subsequent rating decision dates: Fitch (05th April), S&P again on 13th September and Fitch again on 20th September.

According to the latest data by the Croatian Financial Services Supervisory Agency, HANFA, the Croatian pension NAV crept up to EUR 20.5bn in January 2024, growing by 1.4% MoM, and 14.6% YoY.

The beginning of 2024 marked a good start of the new year for the Croatian pension funds, as they recorded a NAV increase of 1.4% MoM, and 14.6% YoY during January, leading to a total NAV of EUR 20.5bn. In absolute terms, this represents an increase of EUR 332.7m MoM, and EUR 2.6bn YoY, respectively.

Of course, given their nature and structure, there are two basic ways that the NAV of the funds can change, and that is the growth/decline in the value of the underlying assets, and the net contributions into the funds. Starting off first with the latter, the net contributions amounted to EUR 113.7m in January 2024, while on the TTM basis ending in January, they amounted to EUR 1.28bn. In other words, net contributions contributed 39% to the MoM NAV change, and 49% to the YoY NAV change in January, showing that a significant amount is contributed by them.

However, the net contributions have been growing steadily in the last couple of years, from an approximate average of EUR 86m a month in 2022 to EUR 104m currently, albeit years in the period before the pandemic did show higher averages as well during certain periods. In other words, net contributions remain stable and have contributed even more significant numbers in the previous years, mainly due to the decline in the value of assets due to the developing macroeconomic and geopolitical situations we have witnessed in the previous years.

Net contributions into the Croatian pension funds (January 2019 – January 2024, EURm)

Source: HANFA, InterCapital Research

Furthermore, the growth in net contributions is also supported by the historically low unemployment rates, and given the overall wage growth we have witnessed in Croatia, driven primarily by inflationary pressures, it isn’t unreasonable to assume that continued growth will manifest itself.

The other side of the coin is the change in the value of the underlying assets. It should be noted that inside these numbers there are also net contributions, and while there is no detailed breakdown as to how much of each of the assets’ NAV growth (for bonds, shares, or any other types of assets as an example) came from net contributions and how much from the asset value change, roughly speaking, 39% of MoM and 49% of the YoY change came from the net contributions, as described above.

In terms of the MoM change of the asset value, the largest increase was recorded by shares, which grew by 3.7%, or EUR 166.2m, followed by deposits and cash at 16.4%, or EUR 110m, the money market holdings, at 63%, or EUR 96.7m, and inv. funds, growing by 2.5% MoM, or EUR 54.5m. Meanwhile, on a YoY basis, the largest increase came from bonds, which increased by 12.9% YoY, or EUR 1.44bn, followed by shares at 23.8%, or EUR 898m, investment funds, at 14.6%, or EUR 283m, and the money market, at 59%, or EUR 92.5m. On the other hand, deposits and cash decreased by 8.6%, or EUR 74m YoY.

Croatian mandatory pension funds AUM structure change (January 2018 – January 2024, EURm)

Source: HANFA, InterCapital Research

In terms of securities and deposits, in total they amounted to EUR 15.7bn, decreasing by 1.7%, or EUR 271m MoM, but growing by 6.3%, or EUR 923m YoY. Domestic securities and deposits make up the vast majority of the holdings, at 88.4%, and having recorded a decrease of 2.4% MoM, and an increase of 4.7% YoY, to EUR 13.8m. On the other hand, foreign securities and deposits amounted to EUR 1.8bn, or 11.6% of the total, growing by 4.2% MoM, and 6.3% YoY.

Finally, taking a closer look at the current asset structure of the funds, bonds have recorded a slight decrease in January, accounting for 61.5% of the total, a decline of 1.4 p.p. MoM, and 0.96 p.p. YoY. Shares on the other hand, increased by 0.5 p.p. MoM, and 1.7 p.p. YoY, to 22.7%. Lastly, investment funds accounted for 10.8% of the total, increasing by 0.11 p.p. MoM, and remaining unchanged YoY.

Current AUM of Croatian mandatory pension funds (January 2024, % of the total)

Source: HANFA, InterCapital Research