September looks like a month when central banks bring on their best performance in what is now a global crusade against inflation. Accelerated US QT starts today, we have ECB GC next week and everything left to doubt is whether they raise by 50bps or 75bps. A lot of hawkish news is already being priced in. Except for one we have all been waiting for – that consumer inflation has peaked. How do we look at these things – read in our brief research piece.

United States’ Federal Reserve’s accelerated pace of balance sheet reduction (popularly called quantitative tightening, or QT) starts today and it’s worth looking over our shoulder to check some of the facts. First of all, FED has a balance sheet of historically unprecedented size totaling 8.8tn USD (link). Elevated US inflation figures motivated FOMC officials to accelerate the pace of interest rate hikes as well as the pace of balance sheet reduction, so on June 01st QT started at a pace of 47.5bn USD; the breakup of these were 30bn USD of USTs espoused by additional 17.5bn USD of mortgage-backed securities. This is scheduled to increase today to 95bn USD (60bn USD of USTs and 35bn USD of MBS). Notice this is the fastest QT pace ever, but it corresponds to largest FED balance sheet ever, as well as consumer inflation revisiting multi-decade highs.

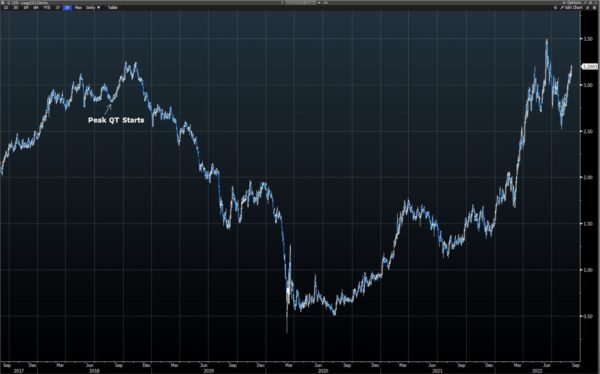

Before we proceed further, some myths should be dismantled. First of all, FED has a much shorter duration of its bond portfolio compared to the 2017-2019 tightening period, which is an end result of buying huge sums of shorter T bills during the pandemic in order to create market liquidity and stabilize the financial system. If you think otherwise, you should check the composition of FED’s SOMA – System Open Market Account (link). A popular myth going around these days is that interest rate rises are expected to affect the shorter part of the curve, while QT is expected to raise longer-term interest rates, but in fact, both tools target the front part of the yield curve. And oh, it gets better – last time FED did a QT, the maximum pace (50bn USD per month) was reached in the fall of 2018. Let’s take a look at how US 10 year behaved after that:

Source: Bloomberg

Notice that after the initial rate rise UST yields went down from 3.20% to sub-2.00% before the pandemic began. One of the key differences between now and then is that in the 2017-2019 tightening period the US curve inverted after the peak QT pace had been reached, while this time the curve is already inverted. This is just one of the many differences, apart from the obvious fact that this time we’re also troubled by staggering inflation rates.

What can we expect going forward? It’s obvious that ECB is calling US FED’s bets and that once Washington started raising aggressively, Frankfurt had to follow suit. Notice that the ECB is doing no QT of its own, but it’s troubled by staggering inflation rates and huge disruptions in energy supplies. Now, we have mentioned a couple of times that weakening EUR versus the greenback is part of the problem of why EU inflation rates are looking so grim. In other words, with no QT in sight in Europe, Frankfurt has to call FED’s bets at least and match the anticipated September rate hike. Notice that in September ECB has an opening act, meaning that this time ECB officials have to act in anticipation of the US FOMC decisions (until now they had the luxury of waiting for the FED to make a move and then react). This is the reason why it’s very, very likely the ECB would raise rates by 75bps at the September 08th meeting. EONIA swaps from Bloomberg’s WIRP EZ function price a 73% probability of 75bps hike in one week’s time:

Source: Bloomberg

The September 21st FOMC meeting is in our opinion still too close to call, but as you can see the market is leaning in the 75bps direction. FED is data-dependent, but the rhetoric delivered on Jackson Hole is quite hawkish. Markets are expecting a 75bps hike as well, but with a 70% probability:

Source: Bloomberg

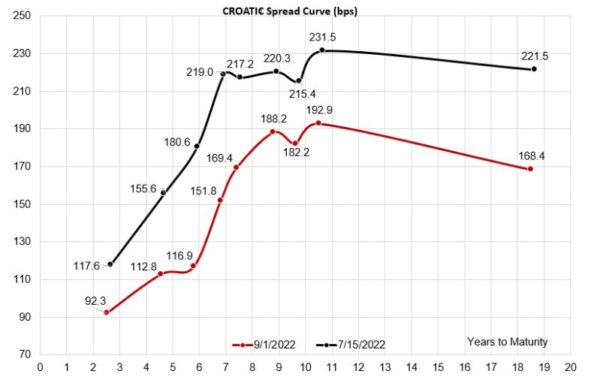

What does all that mean for Croatian bonds? Well, it’s obvious that eurobond yields went up, you don’t need us to tell you that. But the spreads have so far been well behaved and we haven’t seen anybody lucky enough to buy CROATI€ above 195bps spread to Germany. Lately, every nugget of information we have received on the desk has been blowing in the horn of the EU recession – just this morning FT reported that „German factories halt output after Russia’s alarming Squeeze on gas“. The good thing from European perspective is that China has maintained Covid curbs in main industrial cities and accelerated the production of coal, the end result being that China is now exporting LNG (and you thought you saw everything!). This unfolding of events, augmented by the fact that European natural storage is getting nearly full, managed to ease TTF natural gas forward price, but we’re still struggling with elevated electricity prices across the board. Why are we telling you this under the “Croatian international eurobond” paragraph – it’s simply because we have received requests from the client side about our analysis of how Croatian bond spreads would behave in case the EU recession takes hold? Remember, things have indeed changed – Croatia now has a better credit rating than Italy by one notch. Also, cash positions on some of the large institutional asset managers look ample, to say the least.

Is it possible that the EU recession might bring about lower benchmark yields and higher CROATI€ spreads? Yes, it’s possible. But let’s take a few more weeks to think about this scenario, as well as a plethora of events taking place on a global stage.

Source: Bloomberg

Yesterday, LJSE in cooperation with InterCapital held a webinar with 6 listed Slovenian blue chips. During the event, the companies commented on their H1 2022 financial results and Danijel Delač, the board member at InterCapital presented an overview of the Slovenian Capital Market.

The following companies participated in the webinar: Cinkarna Celje, Krka, Petrol, Triglav, NLB and Sava Re. Out of these companies, we listed the most important highlights below.

Cinkarna Celje – the company quickly glanced through their H1 2022 financials results that were also reported yesterday. We’ve sent the Company Note to our clients where you can read financial results in more detail. Further, Cinkarna emphasized its margin cycle since 2017. As the main bullet, the company thinks the peak in their margins has already occurred. Further pressures on margins should be expected in the following quarter. Current and unusually high margins occurred due to the imbalances in the market, which resulted in high titanium dioxide prices – enabling Cinkarna to achieve growth in its profitability. The downtrend in spot prices for titanium dioxide in China has already taken its toll, but Cinkarna estimates there should only be limited spillover on the EU market due to high transport costs (the costs that we should note, are slightly starting to decrease). Regarding contracts with customers and established prices, Cinkarna negotiates its selling prices quarter by quarter. Overall, margins are expected to decrease in the second half of the year and especially during 2023. ESG-wise, Cinkarna noted it is preparing a sustainability report, which will include the taxonomics part for 2022 that should be available in the near future.

Krka – presented 1H results that showed a 6% increase in sales while they also maintained high profitability. The situation in Ukraine and Russia is manageable, but it requires special attention. Results in H1 are encouraging, but business results in H2 may depend on unexpected events that could be evidenced in the possible Covid closing of economies and adverse movements of the exchange rate of the Russian ruble. Besides that, in 2022 they expect sales of EUR 1,610m and net income of EUR 300m. R&D is expected to rise 10% on the level year level.

More than 90% of all receivables are ensured by credit insurance companies. They have been using derivatives to hedge their RUB position. At the end of June, high exchange rate gains that are unrealized are evidence, which could partially be wiped out by adverse changes in the exchange rate. They have realized 13% dividend yield growth in the last 10 years while the pay-out ratio stands at 50%. They have a vertically integrated business model thanks to this model they can be flexible. They plan to realize an increase in sales by adding markets and quantities and they have around 1,500 medical representatives.

They have no problems withdrawing money from two Russian companies and they keep no liquidity in rubles. It is difficult to increase the prices of generic pharmaceutical medicine. Non-prescription medicine is possible to increase prices so it is not a significant part of the growth strategy. Their main goal is the growth of quantity, supported by newly introduced products. they don’t have plans to decrease activities on the Russian market and it is one of their key markets. Currency exposure is managed by decreasing their exposure to RUB currency as much as it is possible.

Petrol – Second quarter was quite turbulent for Petrol Group as the world has changed in this quarter. So, they will not be able to achieve the objectives set in the Petrol Group’s business plan for 2022. It is due to the magnitude and length of the energy crises and the already imposed and announced energy commodity price regulation measures without proper compensation. They were streamlining business operations and they have delayed some investments due to higher inflation a bit as they have been faced with the negative impact of regulation on all of its markets. In Slovenia, they oversee ¼ of the electricity supply and 1/7th of the gas supply to end users so they remain to be a reliable provider of energy supply in this market. S&P has put them on the watch list due to negative intervention in the motor fuel market. In H1 they lost EUR 108.9m in Slovenia and EUR 14.5m in Croatia and they have ongoing conversations with the governments to achieve reimbursement of this economic loss and lost profit. They believe that this is a one-off event and Government is not planning to reintroduce price caps. They are in a good position concerning energy prices as they are hedging and they have been scaling up credit lines to have access to liquidity in case of any adverse effect.

When looking at EBITDA decrease in H1 of 52% YoY and 64% compared to their plan is a direct result of (i) loss resulting from regulated fuel prices in Slovenia and Croatia and weaker results in electricity supply to end consumers. It is also due to cost increases which are affected by adding Crodux and rising selling prices and energy prices of commodities. Inflation is as twice as high as when they made plans, so they think they have a sensible business model. Crodux derivati Group is now part of the Group so you cannot compare results. At the end of H1 they have the same number in point of sales in its network and 359 EV charging stations. In Q2 they deleveraged from EUR 561m to 536m EUR. Integration of new Crodux companies and IT integration of E3 is running smoothly and in Crodux they are even ahead of plan.

There is high uncertainty regarding the payment of compensation due to the motor fuel and other energy commodity prices limitation (electricity and natural gas) in Slovenia and Croatia in 2022. They are in active dialogue with ministries that are covering price regulation and there is a legal foundation in the law for reimbursement so they are positive that ate some point they will get reimbursed.

In Slovenia current regulation on margin in fuel sales is acceptable, but they are still in the discussion that biocomponent has to be included which is not part of the formula yet. In Croatia, they cannot cover all the costs with the current solution, and they are trying to find a new solution. Refining margins have increased two-threefold, which was confirmed by the Austrian regulator after the Russian invasion. So, trading margins have shrunk and they have 1 thousand employees in this market, and believe that they will reach acceptable terms with the Government.

From 1 September electricity prices are regulated and also gas prices would be regulated. From end of October, they look to understand how this will affect them as this is the term when Government has asked, their state-owned distribution companies (Eles d.o.o. and Plinovodi d.o.o.) to prepare a potential mechanism to determine the entitlement to compensation for the companies which could suffer substantial loss because of the temporary electricity and natural gas price control measure. What Petrol now needs to resolve is the bio-component in Slovenia and current regulation in Croatia while they expect that heating oil will also be regulated in Slovenia. More information on what to expect should be available by the end of October.

Triglav – the company presented its H1 2022 results combined with its business plan and strategic estimates. Perhaps the most important thing to point out from the presentation is the view of Triglav for its guidance. The Company still believes its strategic guidance until 2025 to be correct. In 2022 Triglav plans to achieve EBT in the range of EUR 120 – 130m, which, if realized, would represent a decrease compared to FY 2021 EBT of EUR 132.6m. The Company expects gross written premiums to reach levels beyond EUR 1.4b., meaning Triglav expects a continuation of the company’s stable and organic growth in the market. Also, the important thing Triglav noted regarding GWP’s is that H1 growth in GWP’s was only driven by volume, not by prices. Further, Triglav states it should not hesitate if necessary to also raise prices, but already reported H1 growth was not impacted by higher prices at all. Nevertheless, risks are considerably higher due to the adverse effects of the business environment.

NLB – NLB talked about both their business results for 2022, the current macroeconomic situation in the region, current inflation and pressures from the War in Ukraine, as well as their current position in this situation and what are they expecting/doing to mitigate any of the negative trends. Starting off with the results, NLB reported solid growth in both their retail loans and corporate loans sectors. They reported growth in gross loans to consumers, both in terms of the volume as well as the income, and this mainly relates to higher net interest income and net fee and commission income. In Slovenia, they currently have app. 22% of the housing loans issued. In other countries, they have been increasing their market share across all loan segments, and have been growing it faster than the market average They also noted that with every housing loan sold, they sell 5-6 products. In terms of corporate loans, they are growing their business strongly as well, which is especially true in the asset management (investment funds), as well as their life insurance segment, which has a 20% market share. In total, the net interest income increased by 14% YoY, net fee and commission income by 17%, and a net profit to majority increase of 105% YoY, but it should be noted that this was influenced by the negative goodwill from the acquisition of Sberbank.

In terms of the economic and macroeconomic situation, NLB is well positioned for any shocks, they have issued a senior bond that will cover any capital requirements for 2022, they said that this was not required, but was done both as a contingency if the whole economic situation deteriorates significantly, as well as to cover the capital requirements, both in terms of the dividend payment and any potential acquisitions. Relating to the dividend payment, they reiterated several times that the EUR 100m that they have reserved for dividend payment in 2022 is still planned, and as such, it is expected that in 2022 a dividend of EUR 5 DPS will be paid out, which at the time of the presentation meant a DY of app 8%. In terms of M&A, they said that they do not currently see any potential targets for acquisitions, but as the situation in the market is volatile, they will be on the lookout for any opportunities. In terms of the entire macroeconomic situation, they see Slovenia in a very good position considering the situation, and they estimate that the govt. can offer robust support to businesses if needed. If any higher debt requirements would be needed, NLB, as well as other banks have enough liquidity to provide support. Industrial production companies are the ones with the highest exposure to the whole situation, and again, the support should be enough. They see the cost of risk at between 30 and 50 bps, in the base scenario, and only if the situation deteriorates significantly do they expect a cost or risk at 90 bps. Overall, their guidance for the year is strong, they do see some headwinds from the energy market, but the overall equity structure of the corporate and retail sectors is solid, and as such, they expect continued growth in the coming period.

Sava Re – company glanced through H1 2022 results with a detailed decomposition of GWP segments. Sava Re emphasized the ROE is in line with their plan and also in line with strategic guidance. The Company believes its combined ratio of 92.5% is solid, taking the industry norms into the consideration, even as H1 2021 ratio stood at a much lower 80.4%. Sava is currently relatively conservative in the reinvestment sector. Also, the company stated that a higher approved dividend in 2022 should leave capital adequacy intact. Regarding Sava’s strategic guidance the important thing to note is that Sava does not see any new acquisition projects. Further, Sava Re will publish a new updated guidance in the near future.

Slovenian Capital Market – The overview of the Slovenian market was presented by Daniel Delač, the board member of InterCapital Securities, who highlighted the main trends of the Slovenian capital market. He said that local support is coming from retail and investment funds. Value stocks and dividend payers are in focus on the market and the lack of share buyback is representative of the markets. Few stock splits were evidenced on Slovenia capital which is positive as it increases liquidity and entices participation of retail investors. Going forward, the dividend yield is expected to still be highly positive while inflation is a threat, and it is posing pressure on profitability margins. He reckons that there is need for increasing retail participation in the market as in Slovenia. Slovenian retail is heavily under-invested, and it stands far below Western Europe as on average only 5.9% of Slovenia households own shares in Slovenia.

Slovenian market provides an interesting mix of value stocks combined with solid and stable DY. No new issuances of growth companies are announced, while Pharmaceuticals & Financial sectors are having the biggest weight on the performance of SBITOP index. Slovenia offers nice dividend yields as the DY of SBITOP is 7.2%. All companies are paying dividends and they are much heftier compared to e.g Croatia. Slovenia is still undervalued compared to the regional market and it trades currently at P/E of 6.5x, while in the Croatian market this metric stands at 11.2x due to differences in industries that have a higher value in the index. In Croatia, hospitality companies are still trading at quite high multiples and their main 3Q results are still not evidences.

When we look at the liquidity of the market, we can see that the stock exchange is trading roughly between EUR 1m and EUR 2m daily and we don’t see any uptick as we don’t see any trends that could change that. Main culprits for low liquidity on LJSE is that deposit growth and RE investments continue, while crypto is eating a chunk of capital markets liquidity as it is becoming a major theme among retail investors. Liquidity/flow slowly coming back to the local market in spite of the valuation gap. Block trades on the market are of high importance, as they are used by brokers of Institutional investors when they are building and exiting larger positions. Roughly 30% of trading is done via blocks. The government’s role is important as new issuance and tax incentives are needed for long-term liquidity boost.

For Slovenia to move from Frontier to Emerging market on MSCI methodology a lot of things still need to happen. The top three weighted companies in SBITOP index are still far from fulfilling the criteria so this is not expected in the upcoming future.

SBITOP performed nicely compared to foreign market indexes. Expectations for LJSE remain solid, especially for top blue chips. While patience is the key and a long-term investment view is needed by investors. Market faces both supply and even more, demand problems. The highway is there, but there are more drivers needed for it to make sense. Rising interest rates have a positive long-term correlation with financials (heavy-weighers in SBITOP). Securities lending and short trading is still not possible, even though robust settlement system in place. The tax system for remuneration via own shares is not beneficial or supportive for Share buybacks. So, employees and management are not awarded in shares so they are not becoming participants in the market. So a comprehensive State-backed strategy in needed. Issuers are deleveraged so they should be able to weather an increasingly challenging macro environment. Slovenia offers an attractive valuation albeit with liquidity concerns. Investors should be keeping an eye on Western markets as they dictate the broader sentiment. Slovenia is not a typical FM (FM tends to have a low correlation to Developed markets), esp. in a prolonged period.