Word is on the Street that a lot of fixed-income traders are sitting this war out. Bad decision – the current geopolitical layout offers some nice opportunities since realized volatility is here to stay. Positioning is the key because whatever you do, markets eventually move in your favor if you’re willing to wait for a couple of trading sessions. What else did we find out from recent sessions? Find out in this brief research piece.

Recent trading sessions were primarily driven by conflicting news flow coming from the United States and Iran. The news flow ping pong game that we have been witnessing since early April looks like this: headlines about US and Iran possibly reaching a deal “within days” are usually quickly rebuffed by Iranian media claiming it’s all false; financial markets zig-zag in return. There were a few notable exceptions – traders glued to their screens remember pretty well that Friday when Iranian foreign minister Abbas Araghchi claiming that the Strait of Hormuz is open just to see if the corresponding reaction comes from the United States. American’s didn’t want to play ball. Instead, Trump’s administration called for the complete abandonment of the nuclear program from the Iranian side (a well-known no-go), and financial markets quickly retrace the excessive optimism. The very next day, even the IRGC Navy called Aragchi “an idiot”, highlighting that they (IRGC Navy) are in charge of Hormuz vessel transit.

Where does that leave us? Clearly, none of the belligerent sides is really willing to abruptly end the ceasefire and resort to armed conflict once again. Time is on the Iranian side, and by May 09th, OECD crude stockpiles might drop down to an operational minimum. Elevated gas prices spell higher inflation in the months ahead, posing a threat to Trump’s chances of keeping the US Congress under control after the November midterms (the irony of the whole situation is that the 2024 Trump-Vance red wave was also powered by US voters’ discontent with Biden-Harris levels of inflation). By looking at the bigger picture, it looks like 2026 might be a widowmaker year for extreme right/populist leaders around the world. Hungary’s Victor Orban was ejected from his country’s driver seat after sixteen consecutive years in power; Benjamin Netanyahu faces a really election this autumn since all of the opposition parties have united in a single anti-Netanyahu front (sounds a lot like copy-paste of Hungarian political layout, with Naftali Bennet looking a lot like Peter Magyar); and finally, Democrats are rallying against Trump’s many foreign policy errors and it seems that the only thing that consecutively decides US elections are the number at gas pumps. Hence, if the situation stays unchanged (i.e. Hormuz closed, crude oil prices remain elevated) – then the situation will really change on the ballot box. This is our baseline scenario.

There are two things that are leaving fixed-income investors puzzled. First of all, EGB spreads are contained in spite of European governments pledging fiscal support to keep price rises at bay. ECB’s Lagarde has been critical of these decisions since artificially low gas prices in Europe prevent demand destruction from working its magic into naturally lower gas prices. Actually, that’s what has been happening across Asia. Lagarde was judgmental about EU ministers of finance since they are making her job impossible to do. Imagine, all of the countries in the euro area doing their own version of fiscal support, on their own terms and their own timelines. What happens with inflation and growth with this complete disarray? Well, time would tell, but the real problem is the fact that after the ECB’s April 30th meeting there is no more chance of raising interest rates before the June meeting, and by that time it might be too late (again). That’s why ECB will be reluctant to raise interest rates on Thursday (April 30th) but is expected to sound hawkish.

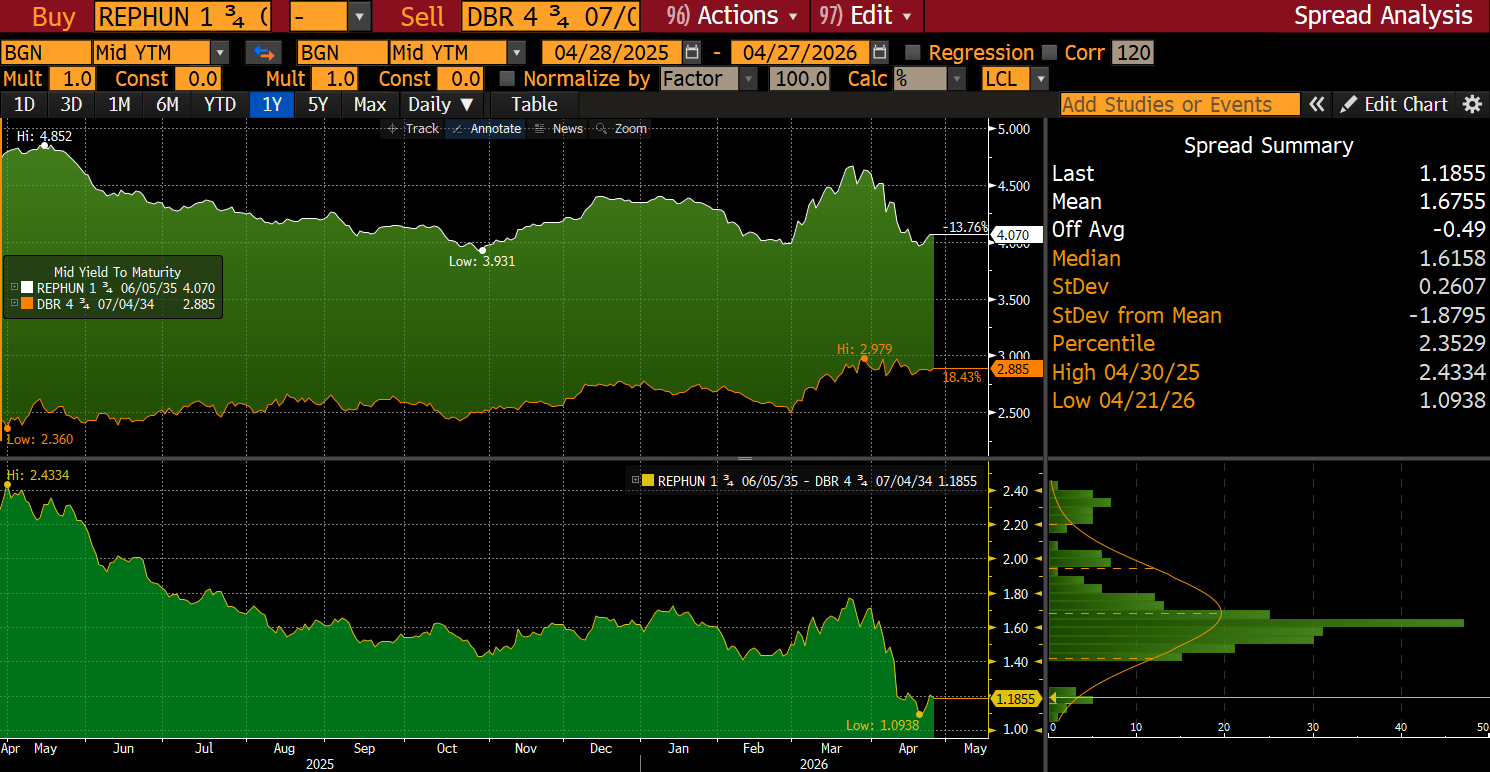

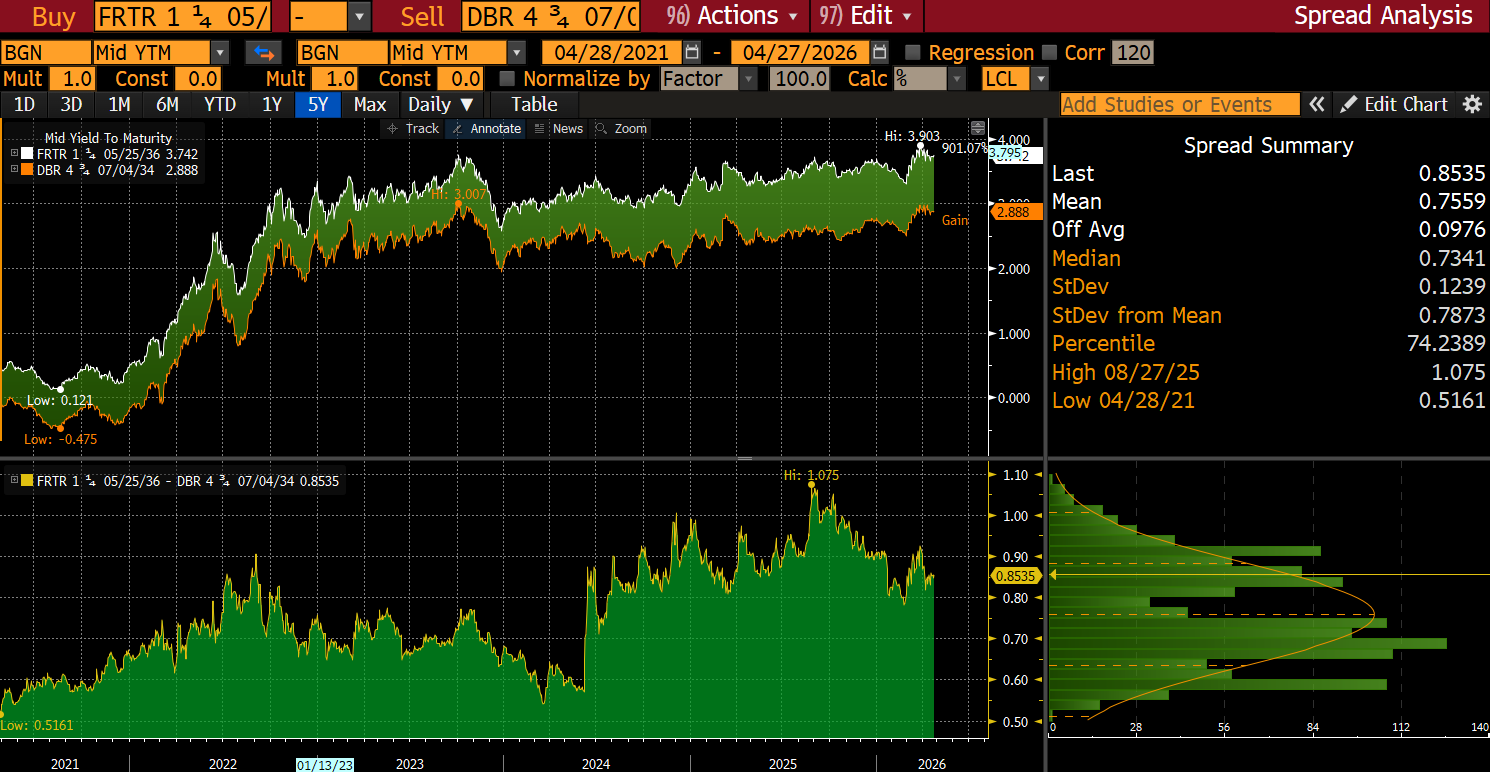

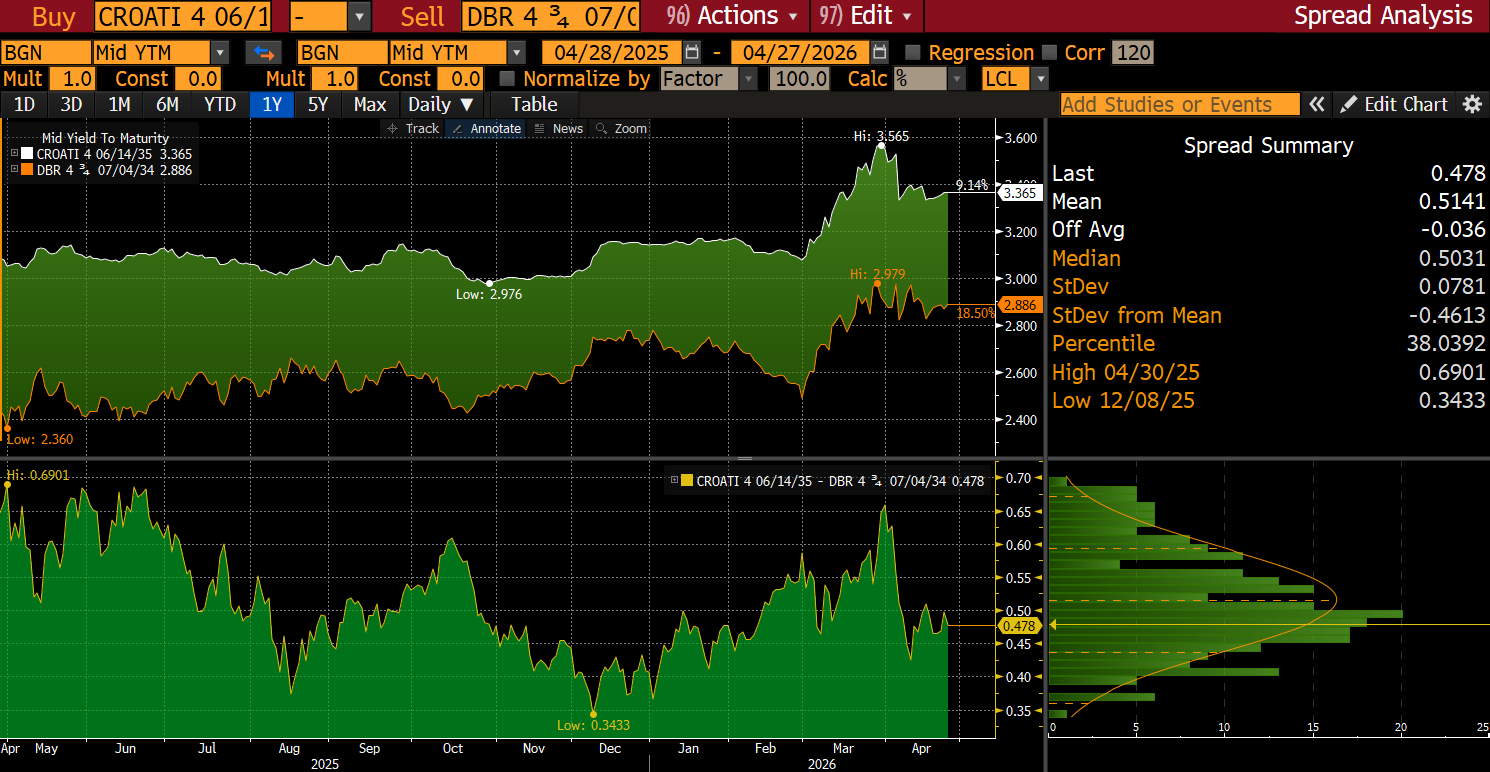

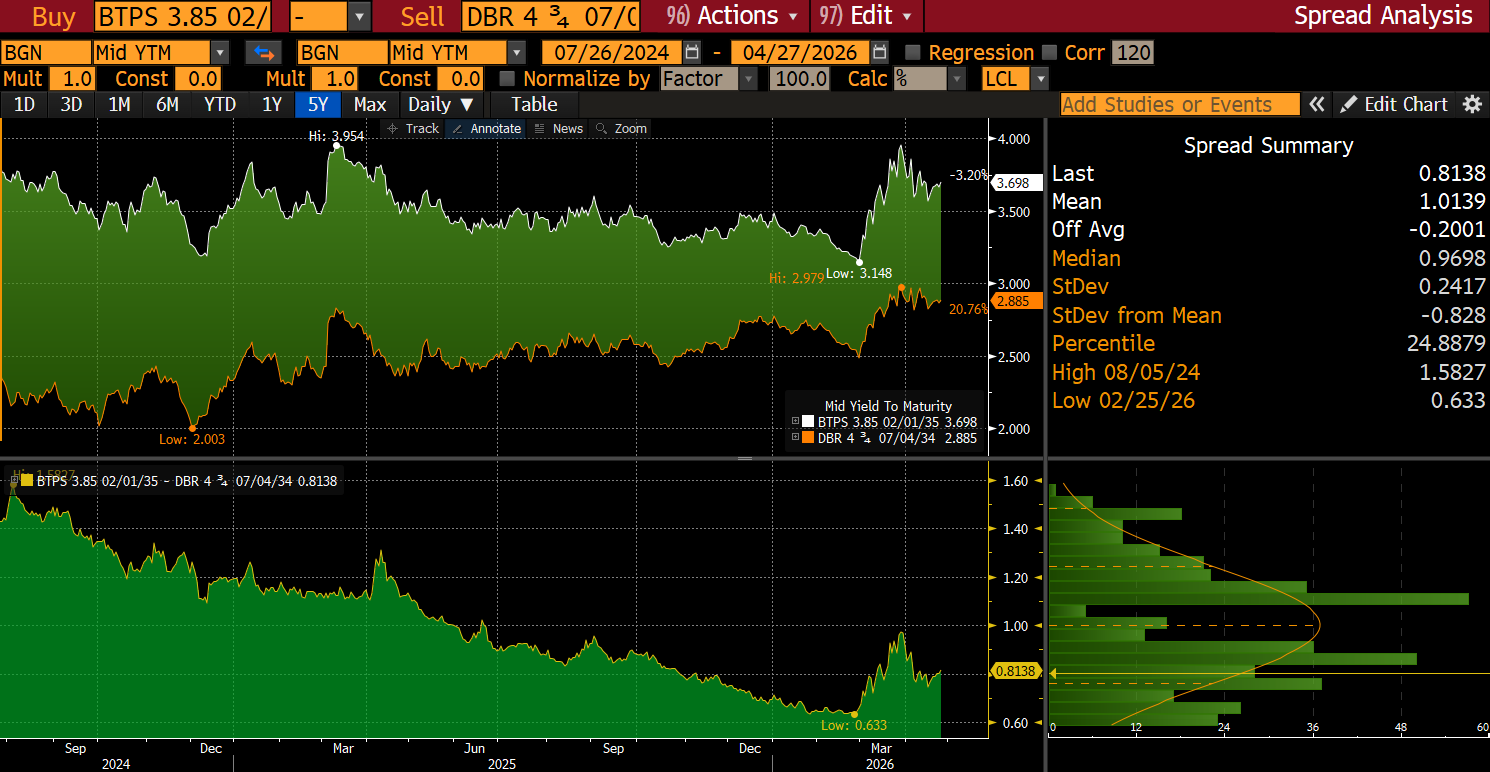

So what does happen with EGB spreads in the coming month? They will be contained, with one notable exception.

In May countries will return to syndicated deals and we do expect some concessions in terms of NIPs. Issuing below the curve seems to be a thing of the past. That’s not all – because of governing coalition breaking down in Romania, Romanian 10Y spread to Germany is once again very close to YTD highs (344bps). This might be a good place to start. So stays tuned, stay focused!