Recent Croatian cash bond flows were dominated by buyers and with the market dry of supply, some of the flow was funneled into local paper-based to an already known feng shui of the domestic market. What can we expect regarding monetary policy, geopolitical tensions, and Croatian bond placements in the nearest future? Read the article to find out.

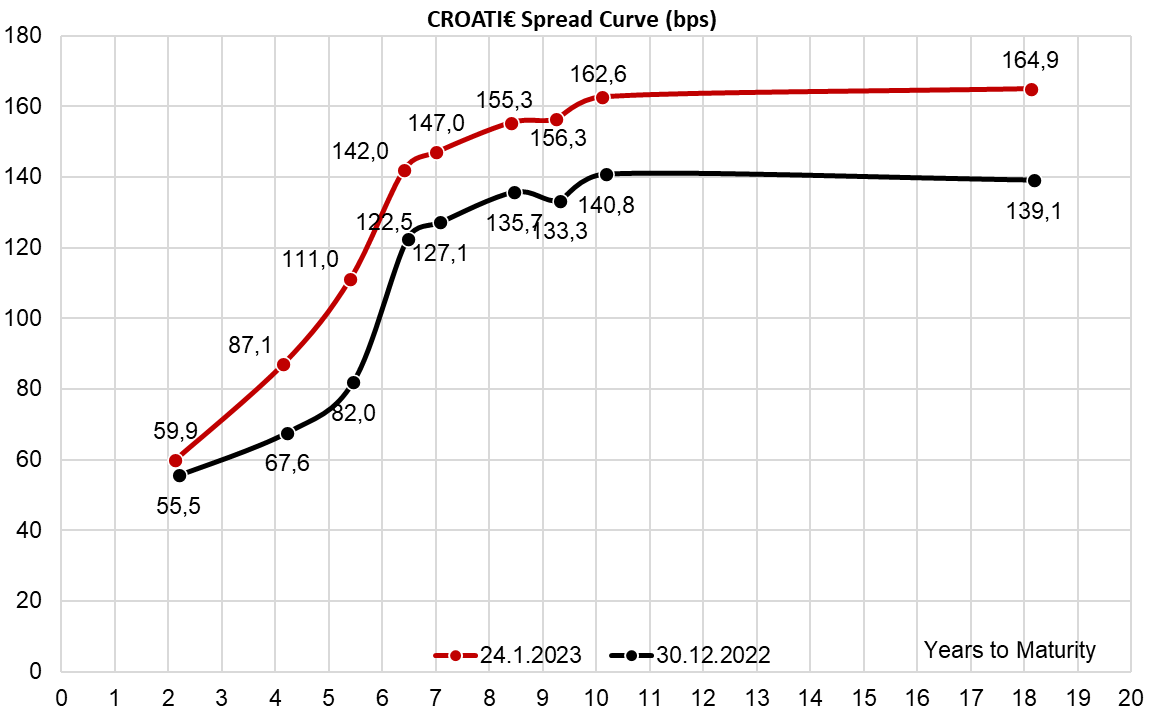

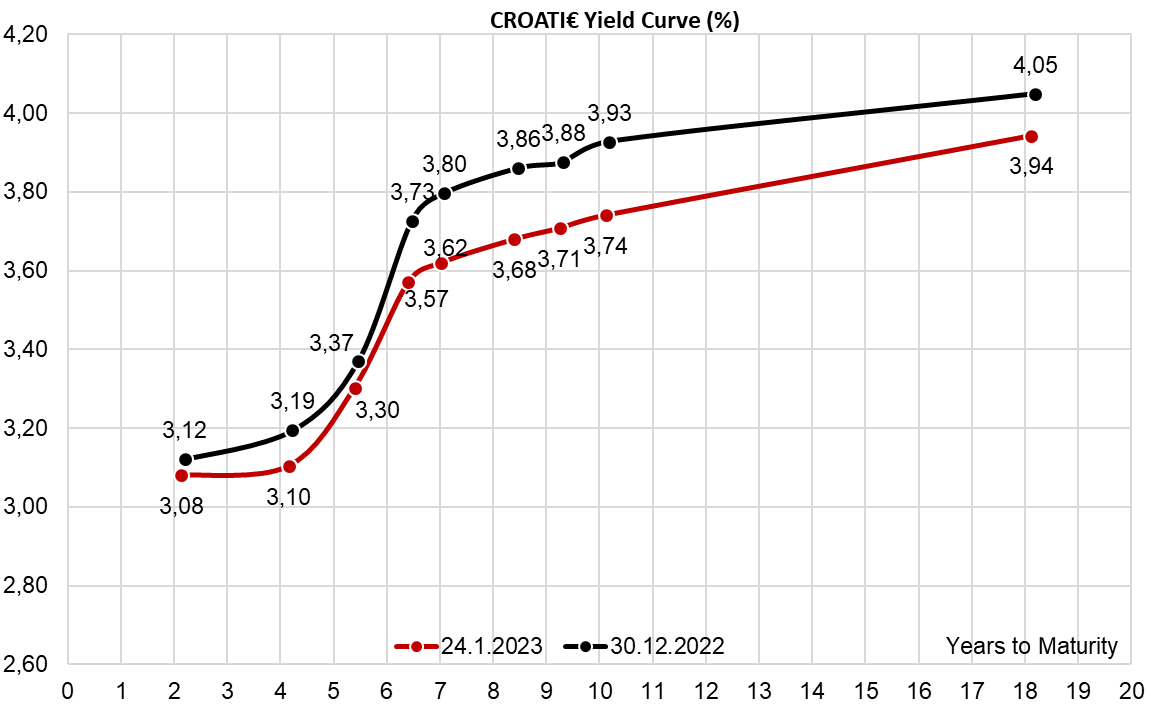

In recent trading sessions, our clients noticed two interesting market features. First of all, it was increasingly difficult to get a hold of a decent offer in CROATI€, especially for a longer duration. After a short-lived sell-off in mid-January, ignited possibly by an increase in CEE primary placements, the market was as dry as it could get. An increasing number of Street dealers indicated that they are short CROATI€, implying that they are better buyers than sellers. Based on this remark, the second feature of the recent trading sessions is the fact that whoever wanted to cut short their CROATI€ position managed to get the price close to BVAL mid, or even higher. But what were asset managers doing with the proceeds of the cash received from trimming their CROATI€ positions?

There were two scenarios. Some of them flocked into short-term EGBs at 2.50%-2.75% YTM since Croatian T bills offer 2.50% on 1Y duration and asset managers estimated that the EA credit risk is much smaller. This scenario also includes buyers of CROATE 1.75 11/27/2023€ at 2.70%-2.95% YTM. The second scenario was buying belly-of-the-curve CROATEs, such as CROATE 1.25 02/04/2030€ which was traded around 3.60% YTM. Notice that this yield implies no liquidity premium to CROATI€ curve, indicating that the market is tight and that CROATE€ sellers are getting slightly a better deal. This scenario was very popular among asset managers that had to target duration and couldn’t be invested into shorter paper all in.

Naturally, there was more switching into shorter EGBs, than into razor-thin CROATE€. We were informed by some of the asset managers that a handful of them expect yields to go higher and spreads to widen even further based on ECB staying on the course of rate hikes and the geopolitical developments in the broader neighborhood. Speaking about the former, it’s worth bearing in mind that the latest addition to ECB’s GC, Croatian CNB head Boris Vujcic, favours a 50bps rate hike at next week’s meeting (February 2nd). This doesn’t mean that the new hawk has been hatched, Mr. Vujcic has been hawkish all along, but rather that the flock of hawks in Frankfurt got a new member of the club. In an environment of core inflation remaining elevated, inflation remains the war that has to be won to maintain monetary policy credibility.

But you all know this by now, so let’s focus on the latter – why do some Croatian asset managers expect CROATI€ spreads to widen compared to where they are now, and pray to the gods of geopolitical developments to make their wishes come true? The hopes are not unfunded by reality because of the recent reluctance of German Chancellor Olaf Scholz to supply Ukraine forces with modern tanks. On Sunday on a trip to Paris Scholz was asked if Germany would approve the supply of armour to Ukraine and his initial statement was affirmative. Nevertheless, when EU ministers met in Ramstein to confirm the deal of tank supply to Ukraine, Sholz’s statement was reserved and he looked as if he was holding back. We were also informed that in high politics every statement that is not a direct, unequivocal “Yes” effectively means “No”. To put the matters in context, Timothy Garter-Ash coined the phrase “Scholzing” – “communicating good intentions, only to use/find/invent any reason imaginable to delay these, or prevent from happening”.

Why is Scholz “Scholzing”? It’s evident that regarding Ukraine, all Western sides want peace, but the ways of reaching peace diverge. It seems that the United States views peace as Ukraine reaching arms parity with Russia on the ground and hence fending off Russian ambitions of crushing the country, leading to peace. Arms parity effectively means that more arms supplies to Ukraine increase the prospects of reaching peace. Poland is a strong subscriber to this point of view. Germany is not. From the German point of view, wars determine not who is right, but who is left and the German historic experience of wars was very much different from that of America. In other words, Germany favours a diplomatic solution to an open military conflict. But don’t worry – Germans will likely hop along on this arms supply issue, albeit not easily, not unequivocally, and not immediately.

This leads us to a final question – why does Ukraine need modern tanks such as Leopard 2, US Abrams, or French Leclerc? Because it’s quite possible that Russia will launch another offensive in late February and assault weapons would then be used to fend off an attack. This scenario would likely cause CEE spreads to widen and some of the asset managers hold this scenario as likely, hence keeping some cash on the sidelines to quickly scoop some of the CROATI€ sell-off. This also means that if the scenario does materialize and some CROATI€ comes to the market – well, you got to be quick to grab it.

What about Croatian bond placement? We think the next bond placement is going to be a local bond used to fund the maturing CROATI 5.5 04/04/2023$. Note that the USD international bond was swapped into EUR back when EUR was quite strong compared to the greenback, meaning that after the swap the net liability amounts to 1.0-1.1bn EUR. This means that the outstanding size may not exceed 1.25bn EUR and that the Ministry of Finance can wait until early March before putting things in motion. The domestic investor base may be resilient to the geopolitical scenario we have just outlined, but only time will tell.