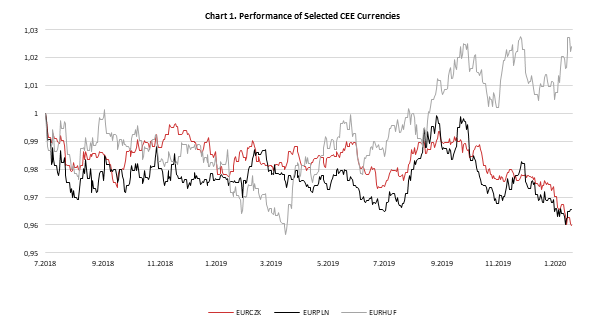

2019 was a stellar year for most of the asset classes, with equities, bonds and commodities posting double-digit performances. However, CEE currencies’ results were mixed. CZK and PLN posted modest positive gains against EUR which, when including for carry, amounted to a total return of close to 3.0%. On the other side Hungarian forint depreciated against EUR by 3.0% in 2019 while Romanian Leu dropped by 2.3%. In the first three weeks of 2020, we are witnessing similar pattern and in this short article we are trying to explain main forces behind CEE currencies and what to expect next.

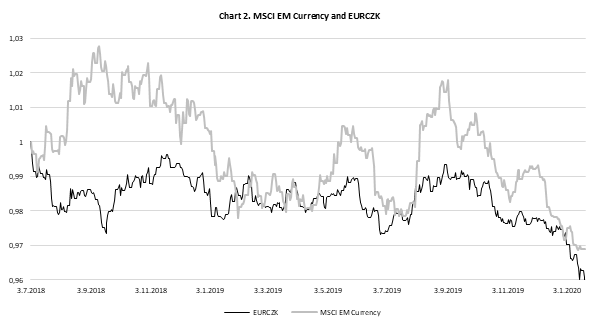

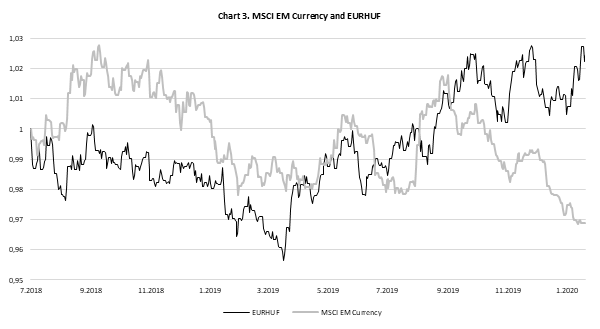

Let’s start this short analysis of currencies in CEE universe by looking at broader environment in which they operate. To start with, our selected CEE currencies (CZK, PLN, HUF and RON) all have positive correlation with euro and with several EM currency indices (this is obvious as our CEE currencies are included in these indices and ETFs). Furthermore, all these currencies post positive correlation with world equity as well, meaning that they appreciate in risk-on periods and vice versa. Regarding economic condition, these 4 selected CEE countries all have similar patterns: they all grow above EU average, their labor markets are very tight while inflation is running on the upper side of the tolerate bands of central banks. Reference rates are above ECB’s, implying they are used as carry currencies, except HUF. Reference rate is the lowest in Hungary at 0.90% and looking at the bid side of EURHUF forward points, there’s only modest 0.50% interest differential to obtain for a one-year period. For both CZK and PLN investor can expect interest differential around 2.0% while Romanian Leu carries almost 4.0%. There are also some idiosyncrasies that needs to be considered. For example, there were some risks in Poland due to CHF loans, while in Romania there were and still are substantial risks connected with overheating of the economy and widening of twin deficits. Also, all these countries were under risk of messy Brexit and lower world trade driven by trade war between US, China and EU.

Source: Bloomberg, InterCapital

Now let’s have a look at what happened in 2019. Last year’s total return was positive among 3 out of 4 countries. Namely, CZK and PLN posted spot positive returns which coupled with solid carry totals almost 3.0%, while Romanian Leu posted negative spot performance, but substantial carry more than compensated for that. On the other side HUF’s modest carry wasn’t enough to cover solid depreciation over single currency. What was the biggest driver of such a divergence compared to PLN and CZK? Most likely, the most real negative interest rates in the whole world. Namely, inflation in Hungary stood at 3.4% in December while reference rate was almost 3.0% lower. Also, due to low interest rates, investors started to short Hungarian forint and use it as a funding currency to go long into richer EM currencies such as Turkish lira, Romanian Leu and so on.

Looking at the current year, Hungarian forint already lost some 2.0% and almost breached all- time highs. This week we saw BBG article saying that short position on HUF started to build in the last several months due to low interest rates that made forint a funding currency versus some “real” EM currencies. So, seems like correlations for Hungarian forint could currently be changed, as risk-off event could lead to buying of forint as investors will try to close their carry trade positions. Nevertheless, Hungarian forint is also part of EM currency baskets which often moves CEE currencies in the same direction meaning that we could see some mixed signals going further. Another important thing is that this Monday Hungarian central bank decided not to maintain its regular FX swap auction, most likely due to forint weakness. Nevertheless, it is not expected from bank to make a U turn in its monetary policy and to turn hawkish.

Source: Bloomberg, InterCapital

Source: Bloomberg, InterCapital

CZK and PLN on the other side continue with their appreciation trend in 2020, following major EM indices and rise of equity since the start of the year. However, there are some signs of economic weakening in Czech Republic which could force central bank to start easing again this year so one should have an eye on CNB. Going further, Romanian Leu stayed close to 4.78 versus single currency and continued moving in very tight band, most likely controlled by central bank. As twin deficits widen and with “government” not being able to deliver smaller wage and pension increases, risks mount which was also marked by governor Isarescu on their last meeting.

To conclude, as equities continue their rally, CZK and PLN are performing great this year, but question is how long this trend can last. On the other hand, Hungarian forint has seen some bad days which should come to an end in case central bank decides to draw the line in the sand as it did this Monday. In Romania there is great carry but also great risk which could be decreased in case new government finds enough political capital to stop wage and pension boosts that do not follow any productivity growth. In case new government stops at least some of the announced hikes, that could be RON positive in the end.