Over the past year, inflation has been dropping on a yearly basis due to a high base in 2022. As the inflation accelerated in 2021 and 2022, the sharp spikes in inflation happened due to the sudden price appreciation of mainly oil, natural gas, and other commodities in Europe. As time passed, those high levels were moving out of the calculation of yearly inflation and that is the main reason for a sharp drop in headline inflation on a yearly basis. However, core inflation remains high as the food and energy prices are excluded from the calculation.

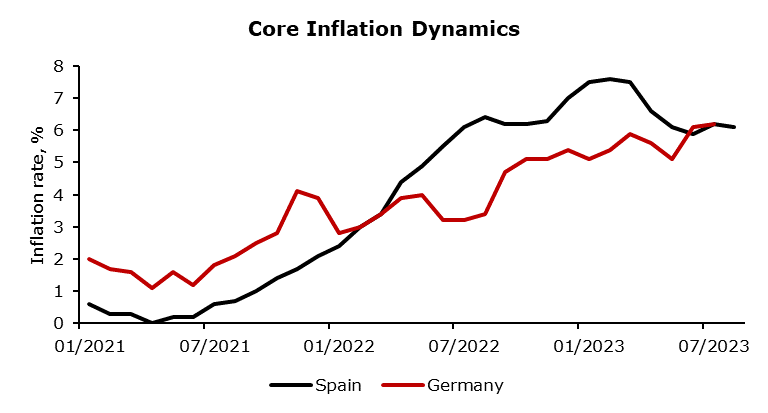

Fear of persistent inflationary pressures is embedded in bond yields which are multiple times higher than a year or two ago. Mainly due to the central bank being hawkish as core inflation remains a bit below highs and fright of high wage growth pushing core inflation up still exists. Thus, central bankers reiterated their willingness to hold rates higher for longer as the structural changes to the economy happened post-pandemic alongside the reduction of globalization. Positive news for European inflation comes out of China as the deflationary risk rises unless China delivers significant stimulus to the economy to reboot economic growth. However, that might put downward pressure on commodity prices and consequently to inflation in Europe, but the Chinese economy losing steam is unpleasant news for the world economy as it is one of the largest world economies with almost a fifth of the world population and huge export capabilities upon which the whole developed worlds depends. High hopes of the Chinese government delivering enormous stimulus for the economy might push commodities back up and push headline inflation in Europe significantly higher. The first signs of inflation rising in Europe are in Spain which recorded 1.9% on a yearly basis in June and now it is already at 2.6%. By the end of the year, it should accelerate further as the average monthly change of inflation in Spain in the first eight months of the year is at 0.4% which should prop up the inflation on a yearly basis notably higher than current 2.6%. However, core inflation is still at 6.1% on a yearly basis in Spain, while the month-over-month average rate of change is at 0.4% which indicates that the core inflation should stay much higher than 2% in 2023. In Germany, the average monthly rate of core inflation in 2023 is at 0.5% which indicates that price pressures persist and times of low-interest regime as it was in 2010 seem to be behind us.

Core inflation should remain remarkably above 2%, thus restraining the European Central Bank from lowering interest rates to prevent a wage-price spiral. Across Europe, unions demanding higher wages were particularly successful and the European Central Bank cannot do much to lower interest rates as inflation remains high even though core countries of the Eurozone are recording negative GDP growth. Mostly it is due to the significance of the manufacturing sector in the economies of the core countries of the Eurozone as opposed to Spain and Croatia whose services sector drive growth and whose economies prove resilient to the rate hikes by the European Central Bank. Currently, there is no reason for the ECB to turn its back to higher for longer policy as the core inflation is notably above the targeted rate and the wage inflation should keep the core inflation high.

In conclusion, the complex interplay of factors has led to a complex inflation landscape in Europe. While headline inflation has seen a sharp drop due to the high base effect, core inflation remains elevated. Bond yields reflect concerns over persistent inflation, spurred by the central bank’s cautious stance amidst fears of rising wage pressures. China’s role as an economic powerhouse adds further uncertainty, as potential stimulus efforts could impact global commodity prices and European inflation. As core inflation remains stubbornly high and wage-price dynamics evolve, the European Central Bank’s commitment to a vigilant approach seems warranted, even amid varied growth trajectories across Eurozone nations.

Source: Bloomberg, InterCapital