Today, we are bringing you the key takeaways of the recently published ECB Financial Stability Review.

The bi-annual ECB Financial Stability Review (published in May and November each year) contains a plethora of data on the financial and credit environment, the financial markets, the data on the Euro area banking sector, as well as the Non-bank financial sector. The report is used by many European institutions, and due to its broad data range contains many interesting data points. The latest version, published on 16 November 2022, can be accessed in full here.

Without further ado, here are our key takeaways:

Recession risks are rising due to higher energy prices and tighter financial positions

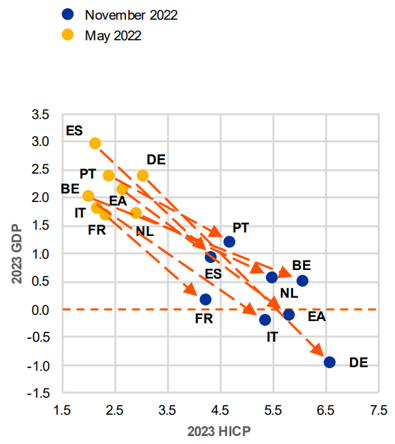

According to the report, the recession risks in the euro area have increased as energy prices have soared. This came as a result of mounting pressure from gas supply disruptions, supply chain disruptions, elevated energy prices, and weaker global trade. In fact, private sector forecasts downgraded their growth expectations for 2023 (to -0.1% vs. 3.0% in May 2022), while higher expectations for elevated inflation (5.8% vs. 2.4% in May 2022) were also recorded.

2023 Consensus inflation vs. economic growth expectations for select euro area countries (%)

Source: European Financial Review, November 2022

Furthermore, the severity of the energy crisis in the euro area has impacted the area’s terms of trade, weakening economic growth prospects. Even though commodity prices have come down from their recent peaks, they still remain elevated, especially for natural gas and other energy commodities. As the euro area economy is a larger net importer of energy, the terms of trade have worsened in 2022. Maintaining the current import volumes at higher prices is resulting in a transfer of purchasing power from the area to the rest of the world. As a result, the negative income impact is significantly higher in the euro area than in the US or the UK, as these economies are less dependent on energy imports. This weaker trade position has also had a significant impact on the depreciation of the euro’s exchange rate against its major global peers.

Higher energy prices and higher borrowing costs are affecting corporations

Even though the corporations in the euro area experienced a sharp recovery and high profits over the past year, they are currently facing stagnating activity and tightening financial conditions. Backward-looking measures of aggregate corporate vulnerabilities, such as gross profits (which are 8% above pre-pandemic levels in Q2 2022), have remained below their long-run average. Furthermore, govt. support measures have helped mitigate the adverse effects of the COVID-19 pandemic. Despite the tightening of financial conditions, lower indebtedness and a high-interest coverage ratio are keeping corp. vulnerabilities below their long-term average.

However, corporates are facing new challenges over the coming quarters, due to worsening interest coverage ratio, higher financing costs, fading activity, and higher leverage. Also, small and medium-sized firms (SMEs) have benefitted less from the rebound in economic activity, as their profitability is still lagging behind that of large corporations. These companies might face a higher risk of insolvency if the economic situation deteriorates further. The sharp increase in energy prices may challenge certain business models and negatively impact the competitiveness of euro-area firms. Business confidence has already started to decline in the most energy-intensive sectors. At the same time, loan demand has increased for short maturities, reflecting the increased need of firms to cover higher production costs. This can also be seen in an increase in debt levels of sectors with high exposure to commodities. Going forward, it might become difficult to sustain high output prices as economic activity stagnates while supply pressures remain. Therefore, producers might have less pricing power than their international competitors to pass on higher costs and input prices to end users.

Household vulnerabilities are also rising

As expected, high inflation and fears of a recession are deteriorating euro area households’ economic outlook. As a result, consumer confidence and households’ expectations of their future financial situation have reached historical lows.

Consumer confidence, expectations of financial situation, and unemployment rate (January 2000 – October 2022, %)

Source: European Financial Review, November 2022

Even though the strong labour market (with an unemployment rate of 6.6% in September 2022) has thus far supported household incomes, inflation is continuing to squeeze real disposable incomes. Higher spending on items such as food and gas has influenced the post-pandemic rebound in consumer expenditures, but this is mostly price and not quantity driven. As the high savings rate recorded during the pandemic normalizes, households’ ability to cushion further price increases is declining.

In terms of indebtedness, household borrowing has thus far remained strong, although there are signs things are changing. Growth in lending for house purchases as well as consumption has remained stable, with September showing growth of 5.1% and 3.7%, respectively, but the growth trend seems to have halted. Further moderation in lending is expected, as higher interest rates on household credit as well as tightening of banks’ credit standards will lead to a reduction in loan demand from households.

Growth in lending to households and household indebtedness (January 2000 – September 2022, %)

Source: European Financial Review, November 2022

As the interest rates rise, some households might have issues servicing their debt. In the low-interest rate environment of the last decade, the share of new loans with fixed interest rates for periods longer than 5 years has increased steadily, reaching almost 70% across the euro area in H1 2022. This shields many households from having their existing debt repriced at higher interest rates in the short term. However, due to the increase in interest rates, the number of newly issued loans with longer fixed interest rates has started to decline. Furthermore, as a further tightening of credit standards is expected, low-income households, especially the ones with high individual indebtedness could be affected.

Overall, despite these challenges, households remain resilient. Even though excess savings are re-absorbed by inflation and net wealth has started to decline, the aggregate household balance sheet remains strong, supported by the current labour market. The rising inflation is continually affecting disposable income and thus consumption, which could slow down overall growth. This could worsen if the labour market environment deteriorates. The immediate impact of the higher interest rates is largely mitigated due to the large percentage of fixed interest rates, but newly issued loans would be affected by higher interest rates which would inadvertently increase the possibility of households being unable to service this new debt.

The real estate market might be at a turning point

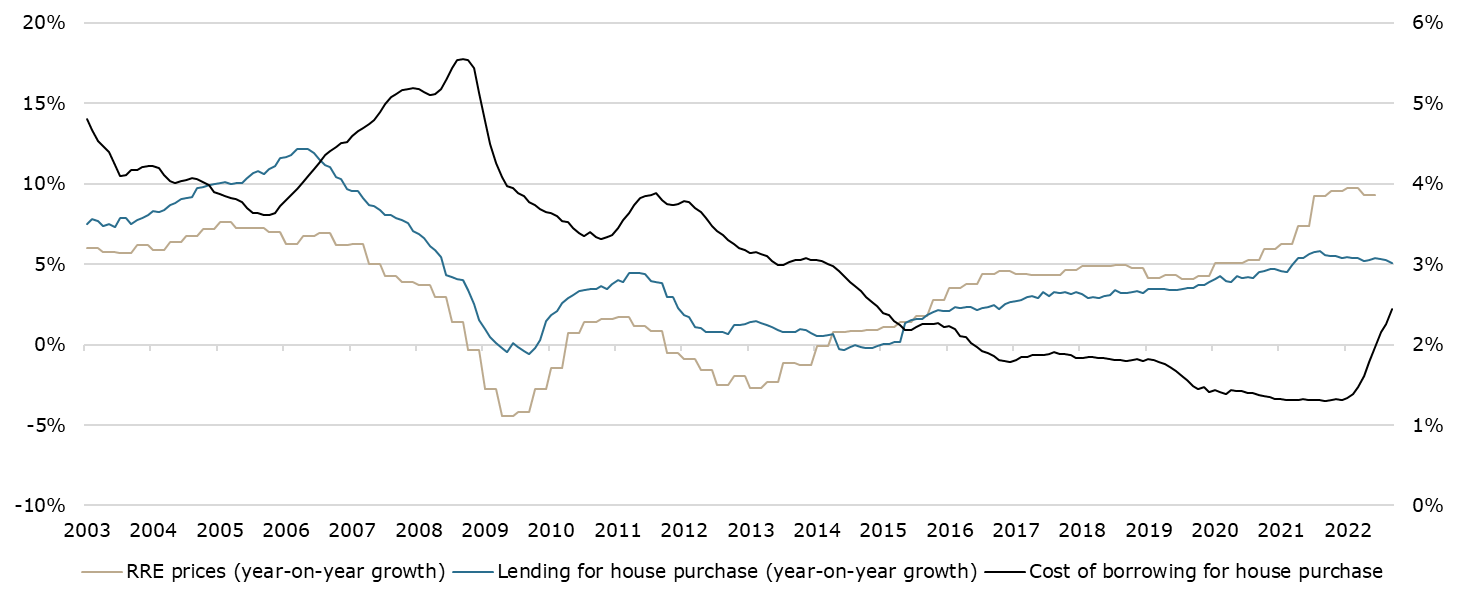

The euro area residential real estate (RRE) market has experienced strong price and lending growth, but forward-looking indicators suggest a slowdown. Nominal house prices grew by 9.3% YoY in H1 2022, leading to increasingly stretched valuations in some euro area countries as house prices exceed fundamentals. Housing loans have continued to show stable growth, but the increase in borrowing costs and further tightening of financial conditions are likely to reduce demand for new loans going forward. Euro area households are also less likely to buy or build a new home, while a lower share of construction companies expect construction prices to increase. As demand slows, the construction sector could come under pressure, which may lead to a rising number of defaults and declining investments.

Euro area RRE prices, mortgage lending, and cost of borrowing (January 2003 – September 2022, %)

Source: European Financial Review, November 2022

This would mean that after a long period of rapid expansion, euro-area real estate markets may have reached a turning point. Rising interest rates and forward-looking indicators are pointing toward moderation in RRE markets, but short-term downside risks have also increased, especially in countries where debt levels are elevated, and properties might be overvalued. As such, high uncertainty remains, and how the situation develops further will not only depend on the government support for households but will also be under the influence of geopolitical and macroeconomic developments.