When our US counterparties try to tell us that somebody is “talking the talk, but not walking the walk“, they usually describe the person with the expression “all hat and no cattle”. It essentially describes the person who dresses up like a cowboy but has no cattle (hard assets) to substantiate his perceived identity. Well, this is exactly how the ECB’s Q&A looked like last Thursday – all hat (dovish lingo), but no cattle (results in terms of lower CPI prints). How are Croatian assets reacting to this – find out in this brief research piece.

With a benefit of hindsight, we could conclude that the recent ECB dovishness was quite short-lived, mostly thanks to hard data announced the following day. But let’s take it step by step.

ECB’s Governing Council raised interest rates by 75bps last Thursday, a move completely in line with market expectations. Apart from that more tightening came through the channel of TLTROs – during the pandemic the ECB initiated a 2.1tn EUR TLTRO instrument, allowing the euro area banks financing at 50bps below the deposit facility rate. It was essentially a cash giveaway since banks had the opportunity to borrow at 50bps below the deposit facility and then deposit the proceeds back at the central bank at the deposit facility rate, netting half a percentage point worth of income in the process. That loophole is closed because from November 23rd these loans would track the deposit facility rate. Salomon Fielder (Berenberg) called this “a rate increase through the back door” and ECB staff estimates that about 600bn EUR of loans might be returned in November. This would definitely ease the lack of collateral on front-end BTP/SPGB curves, so if you were looking to load up on short-term periphery EGBs, November might be your month for action.

But more on ECB. Although fast money accounts might have seen some dovishness in the Q&A session, smart money thought otherwise. The bulk of the dovishness mirage came from one sentence alone – “substantial progress” has been made on “withdrawing monetary accommodation”. Madame Lagarde never said that the ECB’s course of action has been creating the desired results in terms of bringing the core CPI down, although we all know that monetary policy works with a lag. ECB cheerleaders pointed out that EURUSD closer to parity might be playing a significant part in anchoring down inflation expectations (and in that way core CPI as well). Still, that’s all hat and no cattle. Also, pay close attention to the wording of the following statements: Lagarde mentioned that a recession might be “looming much more on the horizon” and that now the ECB is aiming for “reducing support for demand”. Recession expectations should definitely contribute to anchoring down the core CPI, however, you still have the food and energy component which might easily jump back up, especially if crude oil prices stage another rally following the US midterms and December OPEC+ meeting.

Why were the markets so hooked up on the dovish ECB mirage? You must also look at the playbook of other central banks. A week before the ECB GC meeting Fed’s James Bullard and Mary Daly started to let probe balloons on possible slower US rate hikes going forward. Then the ball started rolling – the Bank of Canada delivered a smaller-than-expected rate hike of 50bps and the loonie (USDCAD) hasn’t fallen apart ever since. That was a signal, but it turns out it was nothing more than a false dawn for central bank dovishness. ECB’s perceived dovishness was refuted on the following Friday once German, French, and Italian CPI figures came hotter than expected.

Madame Lagarde pointed out that the coming course of action remains data-dependent, so the wisest suggestion we can make right now is to focus on the short run, i. e. November bond flow. It’s quite likely that November’s return of TLTRO proceeds to the ECB, regardless of their size, might leave Lombard Street dealers with significant portions of periphery EGBs on their books. We’re not convinced that Italian asset managers’ demand might relieve the clout, at least not without meaningful spread widening on the front part of the BTP curve. This comes with a big caveat. After November 08th and the end of the US midterms, US risk markets usually stage a rally which is consistent with the tightening of HY premia and lo spread (BTP-Bund) tightening. We advise caution with this idea – we are under the impression that Apple makes up a significant portion of recent SPX’s good performance. Recent news about strict Covid policies in Zhengzhou, the bedrock of Foxconn’s manufacturing and assembly, might become a major headwind to Apple results in Q4 2022, in other words, the holiday season. All of this is a signal for caution, instead of a call to go all in.

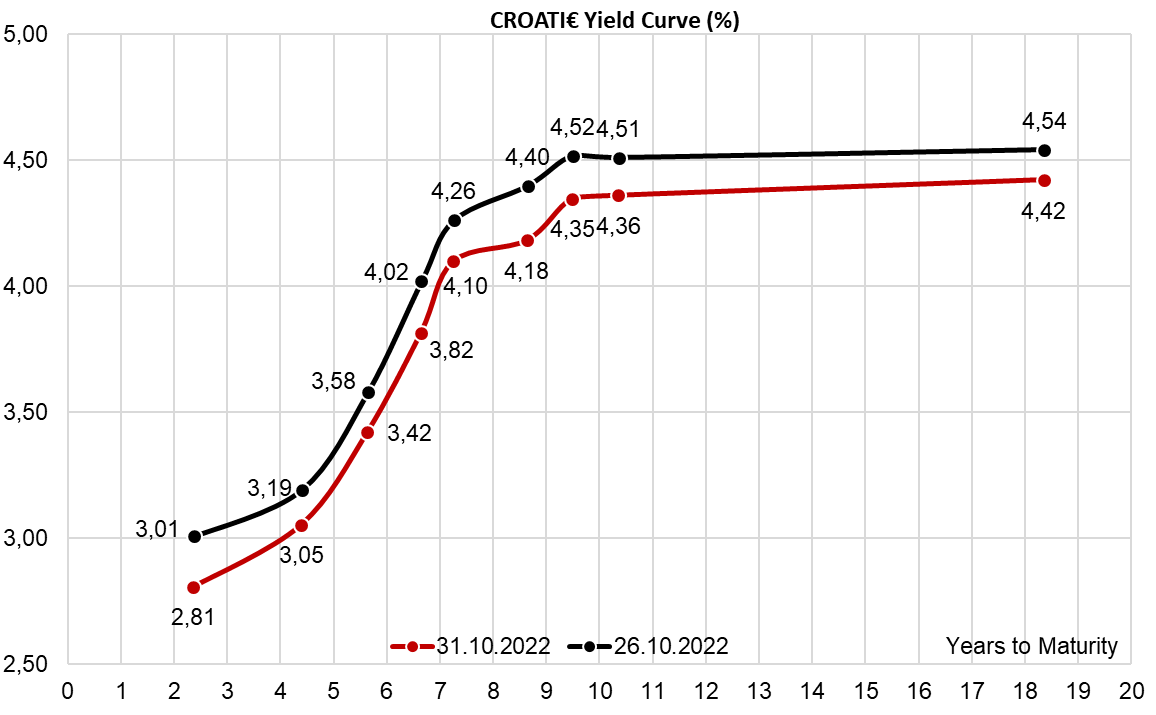

Source: Bloomberg

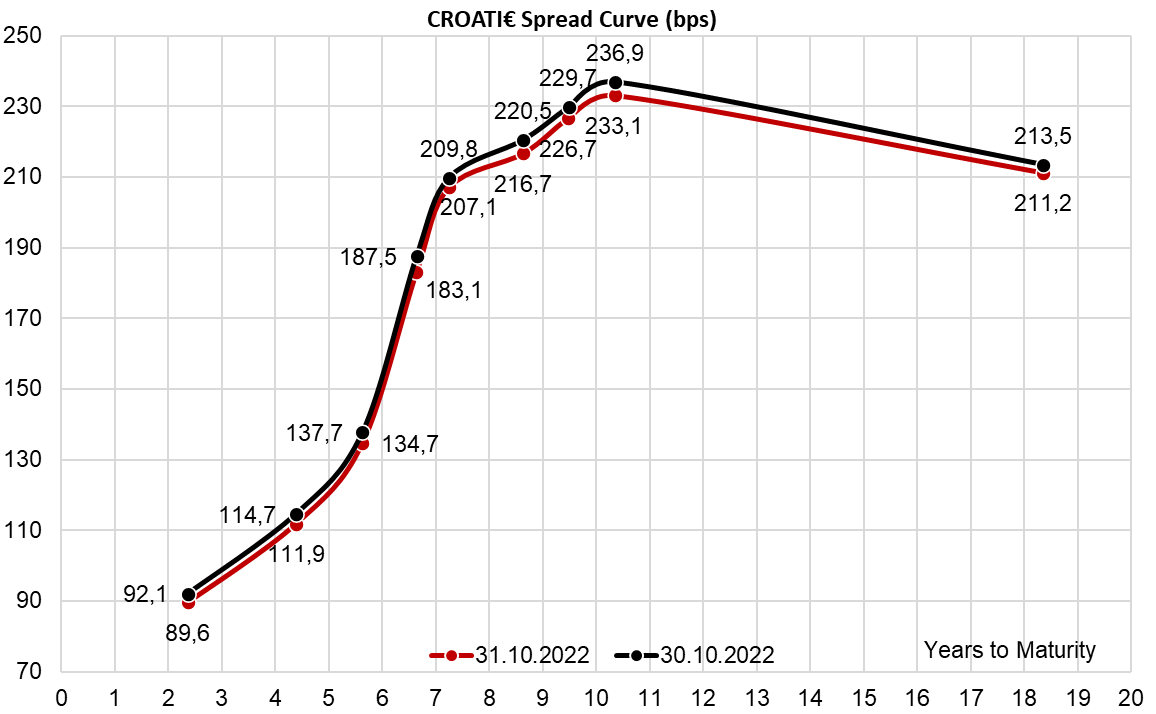

How did all of this affect CROATI€ curves? Well, the yields are slightly lower, however, the spreads are unchanged. To be honest, we have been seeing a lot of demand for longer CROATI€, but it mostly comes from regular, planned flows. Active managers and risk-takers haven’t yet started loading up on CROATI€, perhaps paralyzed by the lack of visibility on the trajectory of major central banks. Stay tuned for more.

Source: Bloomberg