Investing in the biggest U.S. equity index since 2019 would’ve made a positive impact on your portfolio, even with equity market being dragged down by a few negative circumstances like yield curve flattening, QE tightening, boiling inflation, war, etc. Yet, positive sentiment fights pretty hard in financial markets. The region still offers a solid dividend yield which should be attractive for an investor with SBITOP’s expected dividend yield of 6.3%.

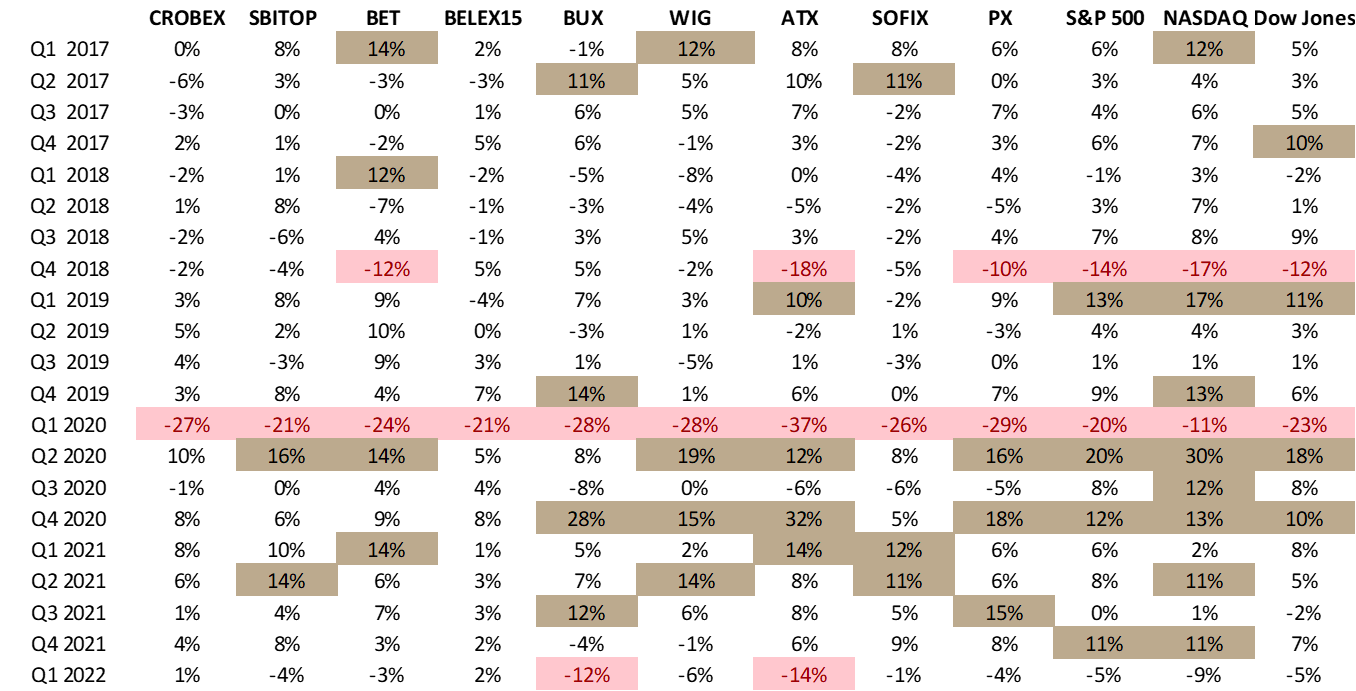

A very challenging quarter ended last week with major global and regional equity indices showing their worst performance in two years. The unease that has plagued equity markets was driven by inflation surging to the highest levels in the last few decades, upending of already stretched supply chains caused by Russia’s invasion of Ukraine and anticipation of rate-increase plan through economies that is influencing discount rates and resulting in flight from equity. 1Q 2022 decrease in value of equity markets is still on average five times lower than the drop induced by the corona crises in 1Q of 2020 when an average decrease of 25% was evidenced. Compared to the end of 2019, equity indices that we are looking at are on average 20% up, while some markets did better than others.

The biggest winners are equity indices in the U.S. (S&P 500, NASDAQ and Dow Jones) and in case you were investing in those markets since 2019 you fared pretty well and could have realized returns in the period ranging from 21.5% (DJIA 2019-1Q 2022) to 70% (NASDAQ 2019-1Q 2022).

When looking at regional markets only Slovenia showed a resemblance with returns to the US by returning 30% in the period from the end of 2019 to 1Q 2022. The drop in Q1 2022 was at 4%, similar to the drop of S&P 500 (-5%) and DJIA (-5%). Slovenia’s equity market has companies with strong fundamentals and since it is a member of EMU, its returns are evidenced in the global currency of Euro. This lack of exchange rate risk gives Slovenia a strong upside compared to for instance Romanian or Polish markets which in the period from the end of 2019 to 1Q 2022 returned 27% and 12%, respectively. In the same period, both currencies depreciated 3.2% and 1.6%, respectively which is not significant in relative terms. So, both markets gave pretty good returns in the period.

Brief regional FY 2021 and Q1 2022 overview

FY 2021 proved to be a very good year for both Croatian and Slovenian Blue Chips. But the market faced another aggravating circumstance, on top of a few one’s market is already bearing (well-known yield curve flattening/inverting, quantitative tightening by central banks more aggressive than expected, still present corona, etc.) due to the Russia – Ukraine situation. Nevertheless, regional blue-chips published their FY 2021 results during March, bearing mostly positive news, among already few mentioned negative ones, still holding up to the positive sentiment.

In Croatia, most blue chips reported both top and bottom-line increases. Croatian tourist’s nights reached as much as 77% of 2019 which was a record year, leading to a triple-digit top-line increase of Croatian tourists. Food companies also reported a good year with inflation pressures starting to impact in Q4. Končar reported robust growth on FY basis. Only AD Plastik reported a drop in both sales and EBITDA levels due to the still-present semiconductor shortage and on top of that, AD Plastik marked the highest negative impact from the Russian invasion of Ukraine due to 27% of revenues being generated from Russia. CROBEX’s movement reported slightly lower changes in price, both on the upside and the downside.

In Slovenia, 2021 proved to be a very good year for Slovenian blue-chips also, as all of them reported YoY top-line growth – clearly representing a more positive sentiment during 2021. This translated into growth in the bottom line for most blue chips. Generally, financials showed a very strong year, yet still having a positive sentiment as the higher expected bond yields would relatively favor financials. Aside from financials, Krka, as SBITOP’s largest constituent, noted a slight increase in sales. Petrol’s acquisition of Crodux boosted their FY and Q4 results. Overall, SBITOP’s expected dividend yield in 2022 is 6.33%, mostly driven by Krka with a dividend yield of 6% and 31% weight in SBITOP. Triglav with 10.4% in SBITOP a few days ago proposed a dividend per share of EUR 3.8, representing a dividend yield of 9.5% at the closing price of the day before, which you can read here.

Corona pandemic market downturn was quite short and severe, and it was followed by a huge amount of government stimulus that has supported the growth of stocks on global and regional markets. But after this market downturn, times of decreasing stimulus and higher marching interest rates are ahead of us. This coupled with oil and energy prices at highly elevated levels shows that this downturn is markedly different from the crash in 2020. The outlook of many multiasset investment officers is that they are not very optimistic about stocks over the next year, while it is not easy to judge by the past as economies were never in a similar position. But it remains to be seen how quickly will assets purchase programs dissolve and how long will global trade bottlenecks be in place. The position of global energy flows are shifting because of Russia-Ukraine war while an abundance of liquidity is not drying up that fast. Companies with exposure to Russia and neighbouring markets are quickly adjusting to new environment in hope that financial markets will not lose their interest. If you throw a good dividend on top of it, demand should be there.