Although a fragile ceasefire is currently in place, the energy crisis still looms over the market, as the mutual (US and Iranian) blockade of the Strait of Hormuz remains in effect. In my previous blog, which I happened to publish just as the Iran war broke out, I covered the flattening dynamics of the US and German yield curves in February. Much has changed since then, and today we will walk through that interim period of two months, which now feels like an entire year.

At the onset of the war, yield curves in both the US and Germany repriced quickly, with markets pricing in more rate hikes and anticipating increased government spending to cushion the impact of higher energy prices on consumers. As a net energy exporter, the US is less immediately exposed to rising energy prices, though consumers are beginning to feel the effects at the pump and in their wallets, putting pressure on the Trump administration to respond. Europe faces a considerably larger challenge. As a net importer of oil and natural gas, much of which originates from Gulf region suppliers, governments will be forced to stretch already strained fiscal budgets further to help shield consumers from price increases.

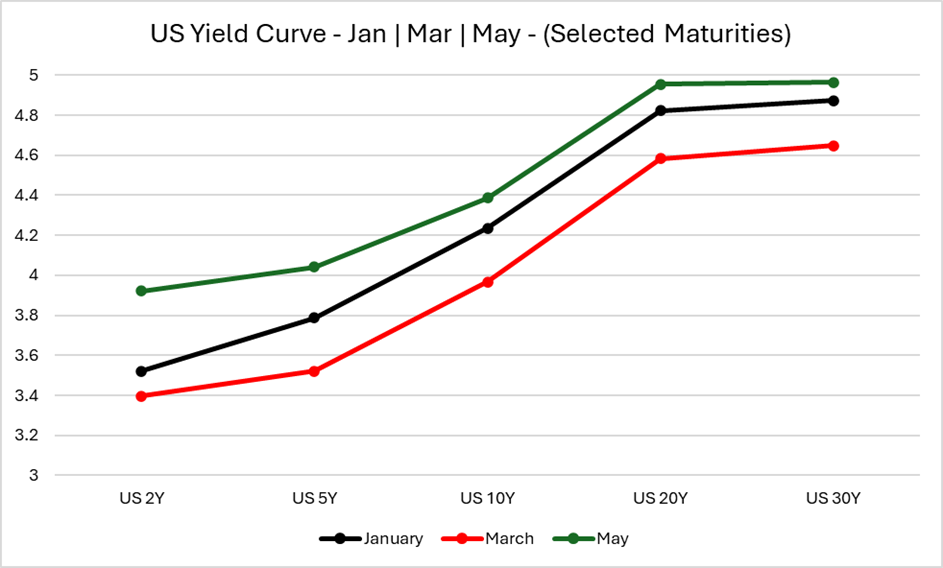

The US yield curve experienced a considerably less extreme bear-flattening dynamic than its German counterpart. This can partly be attributed to the fact that the US is a net energy exporter and faces no immediate risk of supply shortages. The Fed has remained on hold with respect to interest rates, and while markets briefly priced in hikes at the onset of the conflict, that pricing quickly faded, the market is now pricing cuts towards the end of 2026. The dynamic may also shift following the recent nomination of Kevin Warsh as the new Fed Chair, who is set to preside over his first meeting in June. With this in mind, the divergence is visible in the data. The 2-year Treasury yield rose approximately 52bps while the 10-year yield increased by around 42bps over March and April currently sitting at 3.92% and 4.39% respectively, confirming the bear-flattening pattern, with the front end selling off more than the long end. Across the Atlantic, euro area 2Y swaps have increased by about 60bps since the conflict began and are currently pricing an 80% probability ECB hikes next month (June 11th). Actually, ECB-speak coming from Joachim Nagel and Isabel Schnabel points in exactly that direction.

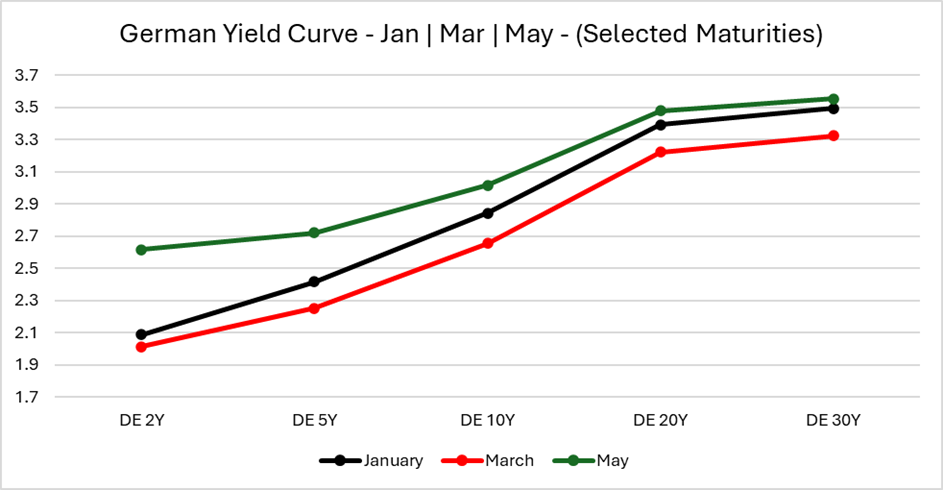

The German yield curve exhibits a considerably more severe case of bear flattening. Europe faces a much larger problem with respect to oil and gas supply dynamics. As already noted, being a net energy importer, with a significant portion of its oil supplies transiting through the Strait of Hormuz, it is more severely affected by the Hormuz blockade. With fiscal budgets already stretched, and in some cases pre-committed to defense spending, it will be far more difficult to absorb new issuance aimed at curbing sustained increases in gasoline and diesel prices, particularly as some airports and airlines are already reporting jet fuel shortages. All of these factors have fed into the bear-flattening dynamic observable on the yield curve. The Schatz yield has risen by approximately 60bps since the onset of the war, currently sitting at 2.62%. The Bund, meanwhile, has tested new highs, breaching the 3% level with an increase of around 36bps.

Although shaken by the current crisis, the US consumer remains somewhat resilient, supported in part by the recent Trump administration tax cuts. With a new Fed Chair nominated, the Fed remains watchful of incoming inflation prints and labor market dynamics before making its next rate move. In Europe, even though the current energy crisis has yet to reach the severity of the one that followed the 2022 onset of the war in Ukraine, the ECB finds itself in limbo, torn between the case for insurance hikes and the reality of anemic growth, which is likely to deteriorate further on the back of looming demand destruction. Negotiations toward a resolution of the conflict remain at an impasse, caught between Trump’s unwillingness to withdraw and Iran’s inability to consolidate power and accept US terms. With vessels still unable to freely transit the Strait of Hormuz and with Iranian storage capacities filling up rather quickly, a swift resolution of the conflict is of paramount importance.