Today we are bringing you our overview of the announced Croatian and Slovenian Blue Chips’ dividends, for the year 2024. The currently announced dividends in Croatia would imply an index DY of 3.1%. Meanwhile, in Slovenia, the currently announced dividends would imply an index DY of 5.8%, while if we include the full NLB dividend amount, as well as our own estimate for Equinox’s dividend, the SBITOP DY should land on 6.9% in 2024.

Croatia

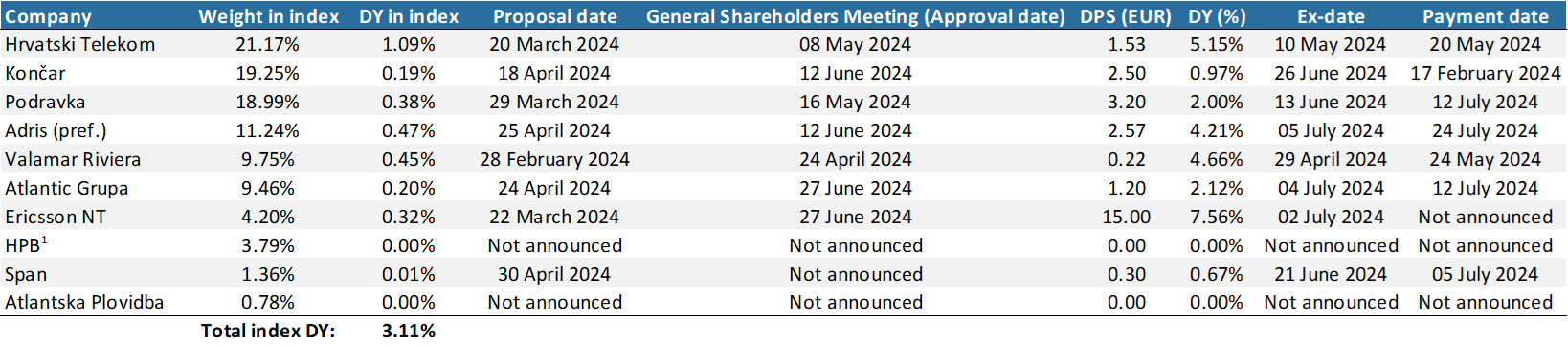

Starting off with Croatia, out of the 10 Croatian blue chips, i.e. members of the CROBEX10 index, 8 have thus far announced a dividend payment for 2024, while 2, HPB and Atlantska Plovidba are yet to announce their dividends.

2024 Croatian Blue Chips dividend information

Source: Companies’ data, InterCapital Research

1Transferred into retained earnings, with a possibility of a dividend announcement later in the year

The largest dividend currently offered by the Croatian blue chips (in terms of DY) is one by Ericsson NT, at 7.6% per share. This is composed of a regular dividend of EUR 10 DPS and an extraordinary dividend of EUR 5 DPS. Ericsson NT recently also announced their dividend policy, according to which they plan on paying out between 30 and 100% of distributable net profit from the previous year, barring any extraordinary events that might affect the business operations.

Next up, we have HT, with a DY of 5.2%, which represents an increase of 39% YoY. HT is one of the most consistent dividend payers on the exchange, and it also has a share buyback program which further enhances the value returns to shareholders. Following HT, we have Valamar Riviera, and Adris (pref.) shares, whose current dividends yield returns of 4.7% and 4.2%, respectively. For Valamar, its position as the largest tourism company in Croatia, combined with improvements in both its top and bottom lines after the pandemic allowed it to pay out higher and higher dividends, culminating in the said DY in 2024. A similar situation is present with Adris, and even though the Company is a composite of various sectors (tourism, insurance, food), it has recorded improved financial results in the last couple of years, especially due to the strong performance of its luxury segment in tourism, and good returns on its insurance segment (Croatia osiguranje). As such, continued growth in dividends was also recorded in the last couple of years.

Besides these, the only companies with somewhat noteworthy dividend yields are Podravka and Atlantic Grupa at 2.1% and 2%, respectively. While both of these companies operate in the food sector, their stories in the last couple of years are almost completely different. While both companies experienced an inflationary hit on their OPEX, especially in terms of material expenses (commodity prices) and employee expenses (inflation-adjusted wage growth), Atlantic Grupa had an especially hard challenge with this, resulting in subdued profitability in the last couple of years. Podravka on the other hand, managed to improve its profitability despite this occurrence, which can also be seen in the share price changes for both of these companies in the last couple of years. Still, for this sector, larger dividends than this are harder to achieve, as a lot of investments also have to be made into maintenance and acquisition/improvement of manufacturing/storage plants.

Lastly, in Croatia we have Span, which as a technology company isn’t expected to pay out a large dividend, as these companies are usually considered “growth” companies, and as such higher expectations are put on them to improve their financials, thus yielding higher future returns. Furthermore, a large part of Span’s revenue is lower margin operations related to licensing services from Microsoft, while its higher-yielding sectors, such as cybersecurity require constant investments in new employees. Span has been growing in this regard, but it takes time for these new employees to become profitable, which puts pressure on the company’s profitability, leading to lower dividends than in the previous year.

The remaining 2 companies in the index, i.e. HPB and Atlantska Plovidba haven’t yet decided to pay out their dividends this year. For HPB, the bank announced a transfer of 2023 net profit into retained earnings. However, this was the case last year as well, but it still paid out a dividend. The reason why though, is related to the fact that it is majority-owned by the Croatian state, and in November last year a decision was made that state-owned companies, especially the ones with “extraordinary” profits will have to pay out part of their profit in the form of dividends. For HPB, this was set at 30% of the 2022 net profit. Atlantska Plovidba on the other hand, might not actually even propose a new dividend, for two reasons. Firstly, it operates in the shipping industry, which is notoriously volatile, having extremely strong and relatively weak years. The former happened after the pandemic in 2020/2021 and part of 2022, while the latter happened from the 2nd half of 2022 until basically today, with slight improvements. Secondly and more importantly, Tankerska Plovidba recently announced the intention of a new takeover offer, after which Atlantska Plovidba’s share appreciated by double-digit levels. In other words, if it gets taken over by Tankerska Plovidba, it can be expected that Atlantska Plovidba will be delisted from the stock exchange as was the case with previous takeovers by Tankerska Plovidba (TUHO, TPNG).

All taken together, the currently announced dividends would imply a dividend yield of 3.1% for the entire CROBEX10 index, taking constituent weightings into account.

Slovenia

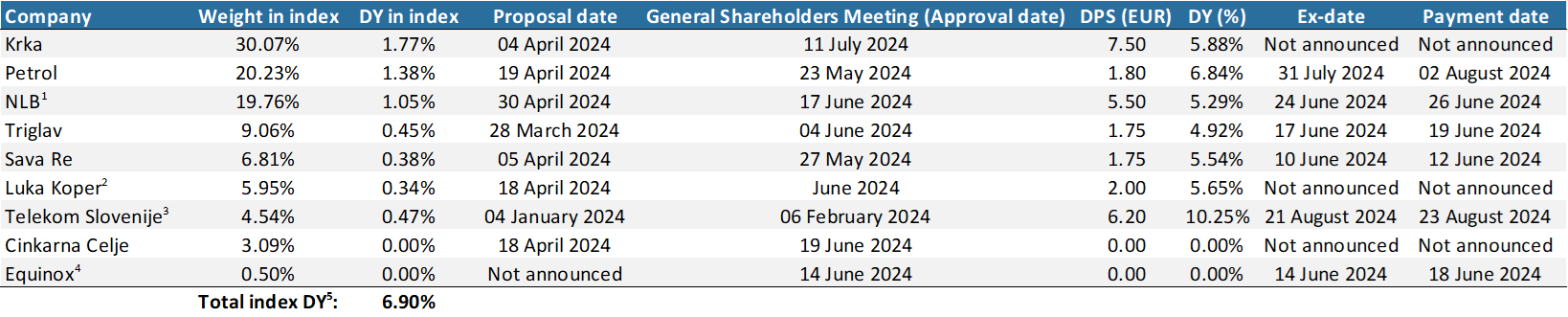

2024 Slovenian Blue Chips dividend information

Source: Companies data’, InterCapital Research

1Data represents the 1st dividend tranche, NLB is expected to pay another one, in the same amount, for a total of EUR 11 DPS

2No exact date of GSM has yet been announced

3Ex-date and payment date refers to the 2nd dividend tranche of EUR 3.1 DPS, EUR 3.1 DPS already went ex-date and paid out

4According to the Company’s financial calendar, the convocation notice should be published on 10 May 2024, during which the dividend proposal will be made. The ex-date and payment date are already available in the financial calendar.

5Index DY includes both the unannounced Equinox dividend as well as the full expected dividend for NLB Group

For Slovenia, the largest dividend yield in 2024 is actually held by NLB, at 10.6%. The dividend presented in the table above is the one that was announced recently. However, it should be noted that NLB usually pays out 2 dividend tranches in a year, and this represents the 1st one. Furthermore, given its strong financial results on the back of elevated interest rates and continued new loan production, NLB announced an improved outlook for this year and the next, and they plan on paying out EUR 220m (EUR 11 DPS) in the form of dividends this year. While the 2nd tranche is yet to be announced, it is almost 100% certain it will be made in this form. At the share price before the initial announcement, this would imply the aforementioned 10.6% DY.

Following NLB, we have Telekom Slovenije at a DY of 10.3%, or a total dividend of EUR 6.2 per share. However, it should be noted that Telekom Slovenije proposed 2 dividend tranches as well, one of which was already paid out, leaving only EUR 3.1 DPS to be paid out in August. While the 2024 dividend is positive, it has to be noted that it came about due to the fact that Telekom Slovenije did not pay out a dividend in 2023 due to receiving Government aid. If they did, they would not only have to pay back said aid, but would have to pay out the dividend from the reduced net profit.

After them, we have Petrol at a DY of 6.8%. Petrol’s financials were under special pressure in 2022 due to significant growth in natural gas prices and government regulation of petrol margins. The situation did improve in 2023, allowing the Company to pay out a higher dividend. It should be noted that however, despite this challenging environment, the Company did not skip its dividend payment last year either. Next up, we have Krka, the largest member of the SBITOP index, with a DY of 5.9% in 2024. The Company’s operations, while both more positive/negative in 2022/2023 due to FX changes related to the Russian rouble/euro fluctuations, are stable, and it continues to record top-line growth across all regions, even though profitability might suffer in certain periods, and be above expectations in other due to the aforementioned dynamic.

Following closely after them are Luka Koper, Sava Re, and Triglav, with DY of 5.7%, 5.5%, and 4.9%, respectively. For Luka Koper, the results in 2022 were extremely good (and unsustainable in the longer term), which led to a higher dividend payment in 2023. The situation is more tempered right now, and the Company continues to post stable results, while this dividend is still the 2nd highest after last year’s.

The insurance companies, Sava Re and Triglav, remain stable dividend payers, even though several situations affected them, most notably the natural disasters in Slovenia in the summer of 2023. Besides this, new accounting standards affected them, while the supplementary health insurance changes also hit Triglav in Slovenia. The last two Slovenian blue chips are Cinkarna Celje and Equinox. Cinkarna proposed no dividend payment this year, as it received similar Government support as did Telekom Slovenije, meaning it would have to pay the said support back. However, this doesn’t mean a payment couldn’t be made at the beginning of 2025, much like their 2023 dividend was paid at the beginning of 2024, for the same exact reason.

Equinox on the other hand, is expected to announce its dividend soon, more precisely on 10 May 2024, and this is expected to be in the range of 50-70% of the funds from operations (FFO) of 2023. According to our own estimates, this dividend should amount to app. EUR 2.34 per share, with a DY of 4.3%. Excl. this, all the currently announced dividends would imply an index DY of 5.8%. If we were to include Equinox’s estimates as well as the full NLB amount, then the DY would amount to 6.9%.

By the end of April 2024, Slovenian CPI recorded an increase of 1.0% MoM and 3.0% YoY. The YoY increase marks the lowest rate of inflation since October 2021.

According to the latest report on Slovenian CPI, it has continued to decrease in April 2024, at least on the yearly level, while on the monthly level, it recorded a noteworthy increase. As such, the Slovenian CPI growth amounted to 1% MoM, and 3% YoY. The YoY increase in CPI marks the lowest point of CPI growth ever since October 2021, indicating that the inflation rates continue to cool off, at least annually.

Slovenian CPI change (January 2011 – April 2024, %)

Source: Slovenian Statistical Office, InterCapital Research

Breaking this growth down by components, on an annual basis, service prices grew by 4.5%, while goods prices increased by 2.3%. Inside the goods category, non-durable and semi-durable goods recorded price growth of 3.2% and 1.8%, respectively, while durable goods prices decreased by 0.7%.

In terms of CPI growth by groups, housing, water, electricity, gas and other fuels recorded 4.8% higher prices, leading to a 0.6 p.p. contribution to the overall 3% growth. Higher prices in restaurants and hotels, at 7.3% YoY, contributed 0.5 p.p. to the overall CPI growth, while the remainder of the growth came from all other groups combined. On the flip side, the prices of food and non-alcoholic beverages remained the same YoY.

Moving on to the monthly inflation, in terms of groups, 0.5 p.p. to the 1% MoM increase came from the group recreation and culture, in which the package holiday prices increased the most, at 13.8% MoM. Clothing and footwear prices meanwhile, recorded a 4.2% increase, leading to a 0.3 p.p. contribution to the inflation rate. On the other hand, 1.1% lower food prices led to a 0.2 p.p. negative contribution to the MoM inflation rate, while 9.8% lower prices in spare parts and accessories for personal transport equipment led to a 0.1 p.p. negative contribution.

In terms of the harmonized index of consumer prices, HICP, in April 2023 Slovenia recorded an increase of 0.7% MoM and 3.0% YoY. We already covered how the EU states compare on this metric in our April 2024 CPI overview for Croatia, which you can access here.