Back in 1950 Japanese film director Akira Kurosawa taped his seminal movie Rashomon, in which several perspectives of the same event are used to depict a more comprehensive picture and develop a deeper understanding of forces shaping peoples lives. Today we will use a handful of data sources (perspectives, if You will) to try to develop a deeper understanding of forces driving te recent appreciation of EURHRK exchange rate, and possibly get a glimpse of what might lie ahead. The two principal perspectives are generated from flow data (compiled by the central bank regarding spot transactions) and the effect of gradually increasing kuna deposits and loans in commercial banks’ balance sheets.

Past month has been marked by exceptional appreciation of euro versus kuna – although its quite common for EURHRK to move up in early fall after the tourist revenues dry up, the scale and speed of the move is something that got everybody’s attention. By looking at the Bloomberg’s SEAG function, we concluded that in terms of upside EURHRK volatility we have just seen the best October since 2012.

Central bank data about spot transactions reveals some insight about what lies under the hood (we’re looking at the N4 table compiled by the central bank). In the past month, larger than usual FX trading was recorded on a handful of dates, and each time it was driven by exceptionally high demand for euros coming from legal enterprises (i.e. government and corporates). But to fully understand the chain of events that drove EURHRK to a two-year high, we might look back to June 2019 for more clues.

Back then the Croatian government placed a total of 1.5b EUR of brand-new international bond (CROATI 1.125 06/19/29) and generated proceeds amounting to 1.47b EUR (notional multiplied by 98.148, a reoffer price). According to the latest central bank bulletin and corresponding Excel files, about 710m EUR of the total proceeds were deposited with the central bank, while the remainder was probably converted into local currency and subsequently deposited with the central bank as well (this notion could be validated by looking at G11 table compiled by the central bank; cell LU34 shows that 662.6mio EUR were traded between the central bank and the Ministry of Finance, roughly corresponding to the remainder of the proceeds). The proceeds were intended to be used to pay off the 1.5b USD notional of the international bond CROATI 6.75 11/05/19, becoming due tomorrow (November 05th). Since this is the only USD-denominated international bond issued by Croatia without the accompanying FX swap to transform the liability from USD into EUR, some 1.36b EUR would be required to settle this paper with the current EURUSD exchange rate.

According to the central bank balance sheet (the C1 table), Croatian government bought some euros in the secondary market in September, driving the FX deposit with the central bank to about 978m EUR. Additional 380m EUR would be required to settle the debt maturing tomorrow and although government has ample cash, still this cash needs to be converted into appropriate currency (this implies buying EUR in the domestic market and then converting it into USD at some point in time).

It’s quite plausible that the Ministry of Finance was buying euros to settle the international bond maturing tomorrow – this would explain the direction of the market, as well as the concentration of the flow.

Why didn’t the government buy foreign currency directly from the central bank? To answer this question, take one more look at G11 table: historically, it was quite uncommon for central bank to sell foreign currency to government. Although that happened back in February when 463m EUR were sold to Ministry of Finance in order to pay for the maturing FX-denominated treasury bill (RHMF-T-906X), still You would have to go back to October 2012 to see the second-to-last large sale of foreign currency from the central bank to the government. History teaches us that for some reason these transactions are not so common and it’s reasonable to assume that to buy the required FX, government simply had to rely on it’s own devices, i.e. the secondary market.

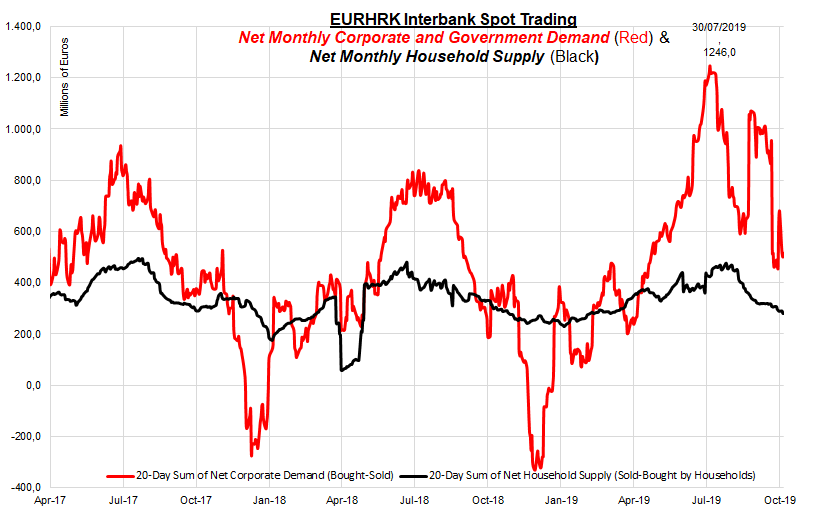

Back to spot transactions on Croatian FX market – unfortunately, the table N4 (daily FX turnover) reveals very little about the possible direction of EURHRK exchange rate, and moreover it can occasionally be misleading. Take a look at the chart submitted below (“EURHRK Interbank Spot Trading”) on which we depicted monthly net purchases of legal persons (corporations and government units, red line) versus monthly net supply of foreign currency by individuals (black line). To make sure You understand what each curve represents, observe that on 30th July 2019 there was a net corporate demand for euros in size of 1.246b EUR. This number means that in the 20 working days preceding July 30th Croatian legal persons bought a total of 2.213b EUR and sold a total of 967.2m EUR, netting a value of 1.246b EUR (small differences are caused by rounding). The trouble with this figure lies in the fact that this includes only spot transactions – swaps and forwards, a more liquid market, is not included, meaning that we’re observing only the tip of the iceberg of demand by legal persons. Nevertheless, this chart is really useful in visualising the point in time when the corporate demand starts shifting into negative, i.e. when corporations become a net supplier of foreign currency. It usually happens between mid-December and mid-January and it’s reasonable to assume that this flow is driven by FX speculators.

Another angle on EURHRK dynamics comes from commercial banks’ balance sheets.

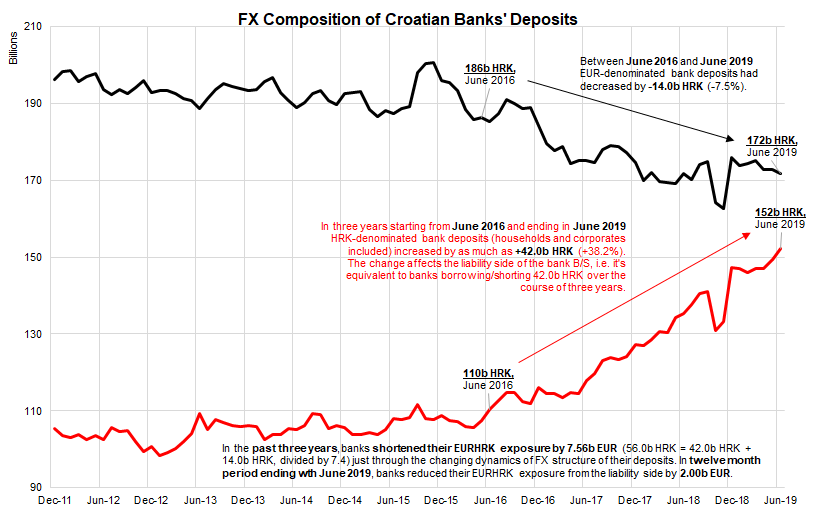

First a couple of words about the anatomy of Croatian banks. In June 2019 Croatian banks had an aggregate B/S in size of 420b HRK; on the liability side total deposits make up about 340b HRK (44.7% HRK-denominated, 50.4% EUR-denominated, close to 4.0% in USD and remainder in CHF). The currency structure of overall deposit went through a significant change in the last three years, as chart depicted below clearly demonstrates. It’s curious to note that in the last twelve months the size of local currency deposits increased by 14.8b HRK (the change in EUR deposits at the same time is too small to be considered important). In other words, looking at just the liability side, the short EUR position is gradually decreasing (i.e. EUR-denominated deposits are shrinking), while the short HRK position is increasing (HRK-deposits are on the rise) – this means that the banks are going long EURHRK through the changing structure of their liabilities. If nothing was happening on the asset side, they would have to sell EURHRK to hedge themselves against strengthening kuna.

What were banks doing to hedge themselves against weakening euro/rising kuna? A significant part of FX hedging came from the changing FX structure of bank loans, although You have to know one more thing about the anatomy of Croatian banking sector: in absolute size, they’re much smaller than deposits (as a matter of fact, in June 2019 overall bank loans amounted to 254.9b HRK). Nevertheless, it’s worth mentioning that according to the table SP4 (compiled by the central bank as well), since June 2016 EUR-denominated loans decreased by 27.2b HRK (to 143.0b HRK), while HRK-denominated loans increased by 21.8b HRK (to 109.2b HRK). Through the changing loan structure Croatian banks effectively went short on EURHRK. The trouble with this analysis is that it’s still difficult to see the off-balance sheet items, preventing us from delivering the final verdict on the effect of bank B/S rebalancing on the EURHRK exchange rate.

In other words, commercial bank B/S data can also deliver misleading results, for the sole reason that it simply doesn’t convey all of the necessary data.

So where exactly does that leave us? Famous forecaster Nate Silver said that before engaging into forecasting You should try to determine what You can forecast effectively. In other words, the recent purchases of euro on the secondary market (regardless of who did it) have increased the amount of local currency in the financial system by considerable amount. It’s a question of time when this liquidity might start spilling over into liquid financial instruments – local bonds might be a target in this process. Currently, this spill over is on hold because it’s clear the government is planning to hold a local bond auction in the coming weeks to roll over the maturing RHMF-O-19BA. It’s quite likely that cash rich market participants are waiting to see what they might get on the primary market. Nevertheless, the liquidity is ample and it’s quite likely that after the primary market ends, HRK-denominated fixed income paper might be bought into year end. That is… unless the eurobond yields start moving up.

If You think this is complicated, try watching Kurosawa’s Rashomon. Then please read this research piece one more time.

It will look much simpler than the first time.

The Court of Arbitration has ruled that Antenna Slovenia B.V. exercised its put option correctly, and has imposed on Telekom Slovenije to pay EUR 17.59m with default interest and costs of the arbitration procedure for the 34% share in Antenna TV SL

Earlier today, Telekom Slovenije published an announcement on the Ljubljana Stock Exchange stating that the company received a decision of the Court of Arbitration of the International Chamber of Commerce (ICC) in the arbitration procedure between Telekom Slovenije and Antenna Slovenia B.V. The procedure was launched to determine the purchase fee amount in exercising the put option by Antenna Slovenia B.V. for the sale of a 34% share in Antenna TV SL, to Telekom Slovenije.

The Court of Arbitration has ruled that Antenna Slovenia B.V. exercised its put option correctly, and has imposed on Telekom Slovenije to pay EUR 17.59m with default interest and costs of the arbitration procedure for the 34% share in Antenna TV SL

The ruling of the Court of Arbitration is final and binding for both parties.

The company announced an investment plan of roughly HRK 500m. The mentioned plan is stated to be the driver of the growth in the coming period.

Arena Hospitality Group published an announcement on the Zagreb Stock Exchange announcing an investment plan of roughly HRK 500m, which is in line with the company’s previous announcements. The mentioned investment plan is stated to be the driver of the growth in the coming period.

The investment plan includes:

- The repositioning of hotel Brioni, which will start at the beginning of 2020 and will open in the summer of 2021. The hotel will be repositioned into a luxury upscale hotel with 227 rooms.

- Continued investments into Arena Kažela Campsite through a second phase, which has started in October. The first phase of the investment included 164 new luxurious mobile homes, two new pools, reception, new pool bars etc. The second phase of the investment will include a further replacement of mobile homes, repositioning of pitches (which will feature a full infrastructure in prime seaside), refurbishment of public areas etc. The investment will transform this campsite into a modern 4* Camping Resort and on completion will be renamed and relaunched to Arena Grand Kažela.

- Continued investment cycle into the Verudela Beach self-catering apartment resort. Following the initial repositioning of the first 10 accommodation units prior to the 2019 summer season, construction works have started in October where the remaining 146 units of the resort will be fully repositioned.

- The repositioning of the restaurant Yachtclub on the Verudela peninsula, along with the refurbishment of public spaces and rooms in its hotel Park Plaza Histria.

In 9m of 2019, the company observed a 2% decrease in operating revenues, a decrease of 36% in EBITDA and a decrease of 72% in net profit.

In the first nine months of 2019, Končar recorded sales of HRK 1.87bn, representing a 1% increase YoY. Meanwhile operating revenues amounted to HRK 1.94bn, which is a decrease of 2%. The mentioned decrease could be attributed to the prolongation and blockade of several significant deals, which include the construction of a hydroelectric power plant in Bosnia and Herzegovina and a delay in the contract realization of equipment to an Iranian buyer (due to sanctions implemented to Iran).

On the domestic market, Končar recorded sales of HRK 721.2m, accounting for 38.6% of the total sales. There, sales of goods and services to HEP account for the majority of the sales.

On the foreign market, Končar recorded sales of HRK 1.15bn, accounting for 61.4% of the total sales. The most significant exports were made to Germany, Sweden, Austria, United Arab Emirates and Hungary.

For the FY 2019, the company expects to record sales of HRK 3.1bn (+8% YoY).

Operating expenses amounted to HRK 1.92bn, representing an increase of 1% YoY. Consequently, EBITDA observed a decrease of 36%, amounting to HRK 87m. EBITDA margin stood at a low 4.5%, representing a decrease of 2.4 p.p. YoY. Meanwhile, D&A remained flat at HRK 68.4m.

Going further down the P&L, operating profit amounted to HRK 18.6m, representing a sharp decrease of 73% YoY.

In 9m 2019, the company observed a net financial gain of HRK 3.6m, compared to a loss of HRK 7.13m in 9m 2018, which helped lessen the decrease of the net profit for the period.

Net profit amounted to HRK 20.1m, representing a decrease of 72% YoY. Such a decrease could be attributed to the lower topline performance compared to the previous period.

In 9m 2019, the company observed a decrease in sales of 2% YoY, (positive) EBITDA of HRK 18.97m and net profit of HRK 22.38m.

As Dalekovod published results for the first nine months of 2019, we are bringing you key takes from it. According to the report, the company recorded sales of HRK 864.98m, representing a decrease of 2% YoY. However, when observing solely Q3 the company recorded a slight increase in sales of 1% YoY, amounting to HRK 325.7m. The company states that during Q3, a high activity of new tenders occurred. Similarly to other quarters, 83% of the revenues comes from the power line segment, 13% from the infrastructure segment, while 4% comes from the substation segment. When observing revenues by market structure, foreign market continues to account for a significant amount, partially due to the decrease of activities and delay of tenders on the domestic market.

In 9m 2019, operating expenses amounted to HRK 894.5m, representing a solid decrease of 6% YoY (HRK 58m). As a result, the company turned its way towards profitability, with EBITDA amounting to HRK 18.97m, compared to HRK -3.9m in the same period last year. However, operating profit remains negative, amounting to HRK -7.97m. Still, this represents a significant reduction in loss of HRK 28.8m.

It is worth mentioning that the Group’s poorer performance compared to the Company was most influenced by the operations of the company MK Manufacturing and OSO which generated a negative EBITDA of HRK 14.7m in 9m 2019.

Going further down the P&L, Dalekovod observed a net financial gain of HRK 30.6m, compared to a loss of HRK 8.51m, which led to a net profit. Such a difference could be mainly attributed to a favorable FX result.

In 9m 2019, Dalekovod recorded a net profit of HRK 22.4m, compared to a net loss of HRK -45.5m in 9m 2018. However, when observing solely Q3 the company observed a net loss HRK -7.7m, representing a reduction in loss of HRK 29m.

Dalekovod Performance (9m 2018 vs 9m 2019) (HRK m)

The Group states that despite the increase in profitability, they continue to operate with limited liquidity and dependencies on the immediate support of key creditors, financial institutions. Limited liquidity is still largely a result of negative operating results in 2018, and current working capital needs to support the growth of business activities in the operational restructuring process.