US CPI went above the consensus estimate, but used cars are not to blame this time. It’s the rents and that is not OK if you are in “inflation is temporary” camp. Have you wondered why did the longer end of the curve flatten after the CPI print? We have an explanation. And no, it was no short squeeze. Read it in this brief research piece.

Yesterday’s US CPI print was clearly a tailwind to everyone believing inflation pressures aren’t going away so soon. Although core CPI came right on the consensus estimates (+0.2% MoM, +4.0% YoY), the headline print managed to slightly beat the expectations (0.4% MoM vs. 0.3% MoM expected by consensus). Reasons for concern are hidden beneath the surface of aggregate print: namely, until September rise in CPI was driven by components dubbed as “temporary” or “reopening related”, while used cars were a poster child. This time around things have changed: used car prices dropped by -0.7% YoY, the second consecutive decline after a rapid, double digit increase at the start of the year. But what’s really raising the eyebrows is the fixed income market reaction: the longer end, such as US 10Y, actually got flatter by a couple of basis points. This fueled speculations that the fixed income market oversold the 10Y into the inflation print and wasn’t able to cover after the announcement, thus effectively creating a minor short squeeze.

We decided to subscribe to a different point of view instead: bear in mind that EDZ2 Comdty (Eurodollar futures expiring in December 2022) dropped for a second to 99.33, implying USD Libor at 0.67% at the end of next year versus ATM 0.12% USD Libor. There’s your explanation for why the curve flattened: market is now starting to price in (again) the possibility of FED being behind the curve on inflation, meaning that if CPI really does get out of hand, they will have to hike more rapidly to stop it from spreading. This would imply at least two rate hikes next year (ATM Libor @ 0.12% + 2*25bps = 0.67%) and rate hikes tend to slow down the economy, the reason why longer end of the curve was being bought by the market. And that’s basically the whole story of yesterday’s US yield curve flattening: shorter end was sold, longer end bought and the results you can see right here – the 2Y10Y spread tightened as a result.

If the focus of your interest was exclusively on US CPI, you might have missed the boring FED minutes which were also published yesterday. “Most” of the participants acknowledged the risks open market operations have on OERs and rents, which is a fundamental support for tapering of the asset purchases in November (or December being the latest). The divide still persists on what’s going on with the labor market: doves claim the gap to full employment is quite considerable, while the hawks think supply side disruptions are causing manufacturing to cut shifts since there aren’t enough inputs to utilize more capacity (i.e. labor force). This time you have to give it to the hawks: even here in Eastern Europe anecdotal evidence points in a way of supply side bottlenecks putting a lid on employment. Just yesterday Slovenian car manufacturer Revoz announced they will reduce its staff by 14.5% by the end of the year because of… Well you guessed it. Chip shortage. They’re the most prominent Slovenian company cutting shifts, but clearly not the only one.

But back to FED – the narrative about labor market is clearly in the eye of beholder and it’s still questionable what the FED is going to do to fight the monster of stagflation – i.e. the unfavourable junction of supply side bottlenecks feeding into higher prices and lower employment. Lifting interest rates faster might not be the panacea FED is after, but then again – time would tell.

Source: Bloomberg

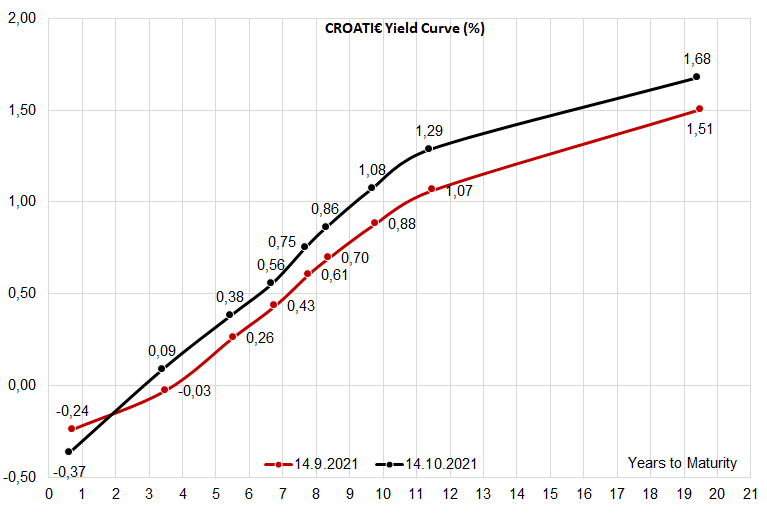

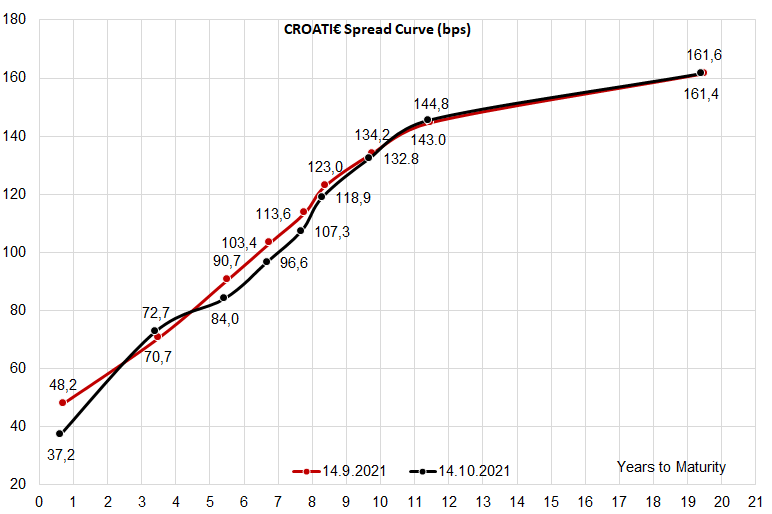

What’s going on with Croatian international bonds? On a five-day horizon the curve gradually steepened, but this week they managed to catch a bid. Market participants are mostly focused on the belly of the curve, paper such as CROATI 3 03/11/2025€ (if they find it at YTM above the freezing level), CROATI 3 03/20/2027€ and CROATI 2.7 06/15/2028€.

Why is that so? From our understanding, some of the UCITS funds have limits up to which they have to be invested into Croatian bonds and some of the buyers fell below these limits, triggering automatic purchases. Fund managers had a difficult job ahead of them – most of them are not sure about the direction if rates, so the most reasonable way to go was to load up on these three bonds. CROATI 3 03/11/2025€ is a “ghost” of a paper – some dealers claim to have seen it being offered, but APA data (BBG MOSB function) comes short of confirming it. Even when some of it appears on the offer, it’s usually short lived since Street dealers who ended up short quickly lift it before somebody else does it for them.

So let’s focus on the next paper on the curve, namely CROATI 3 03/20/2027. UCITS fund managers are veteran traders who understand how fixed income and total return work: bonds tend to roll down the yield curve, so CROATI 3 03/20/2027€ bought today at 0.38% YTM would reasonably expected to be offloaded (if needed) two years from now at some 0.09% YTM (that’s where BBG BVAL placed CROATI 3 03/11/2025€ mid). In other words, you would pay 114.025 today (0.38% YTM, t+2 settlement), sell it at 109.93 two years later, lose about 410 cents on the price, but pocket in 600 cents in coupon, netting some 190 cents in the process. 0.83% in annualized total return on the lowest duration that money can buy on CROATI€ curve. Nevertheless, we stick to the opinion the buying interest might slow down before the fund managers get a hold of direction where the rates might be heading in months to come.

CROBEX ended yesterday’s trading day relatively flat, while SBITOP increased by 0.45%.

ZSE noted a quite high turnover of HRK 43m, of which HRK 73% relates to a block transaction. To be specific, HRK 31.45m worth of HT shares were traded as a block. HT was also the most traded share when observing solely regular turnover (HRK 3.8m).

Looking at the top gainers in the prime market, Podravka noted an increase of 1.26%, followed by Valamar Riviera and Arena Hospitality Group, with an increase of 0.63% each.

Meanwhile, CROBEX, remained relatively flat with an increase of 0.1%, ending the trading day at 2,045.58 points. On a YTD basis, the index is up by 17.6%.

Turning our attention to Slovenia, one could note a relatively low turnover of only EUR 474k. At the same time, Krka makes up for 39% of the total turnover. We note that NLB Group found its place among the top gainers, with a 1.64% increase, ending the day at EUR 74.2 per share.

Slovenia’s SBITOP closed the trading day at 1,168.39 points, marking an increase of 0.45%.

In 2022, HNB expects inflation to slightly decelerate to 2.1%, due to lower projected growth in energy prices.

Croatian National Bank (HNB) noted that when it comes to current economic trends, the model of rapid GDP assessment indicates that the growth of economic activity accelerated in the Q2 compared to the previous quarter, which was mainly due to a solid performance of the tourist season. In 2021, HNB expects the annual growth rate of real GDP to be 8.5%, which reflects the strong growth of exports of goods and services as well as domestic demand.

As the pre-pandemic level of economic activity is expected to be reached this year, growth will slow down in 2022 and the growth rate could be 4.1%, according to HNB. At the same time, strong growth in exports of goods and services is expected to continue, and the inflow from EU funds is expected to affect the growth of domestic demand.

HNB noted that favorable trends in the labor market continued, so that the number of employed people exceeded the pre-crisis level in the middle of the current year, while the number of unemployed ones is still slightly above that level.

In 2021 and 2022, an annual increase in the number of employees and a decrease in the unemployment rate is expected by HNB, while the growth of labor productivity and strong demand for workers could support the continuation of wage growth, especially in dynamic segments of the economy.

HNB added that annual growth in consumer prices accelerated from 2.8% in July to 3.1% in August, mostly as a result of accelerating annual growth in food prices. Although core inflation also rose slightly in August, it remained relatively low at 1.8%. Consumer price inflation could temporarily accelerate to 2.3% (from 0.1% in 2020) throughout 2021, due to an increase in the annual rate of change in energy prices, especially of petroleum products. In 2022, inflation is expected to slightly decelerate to 2.1%, due to lower projected growth in energy prices. However, the negative risks related to the inflation projection were emphasized, i.e. the possibility that it will exceed the projection.

CPI (January 2013 – August 2021)*

Source: Croatian Bureau of Statistics, InterCapital Research

*Annual change