With oil prices rising sharply in the last several months, inflation in CEE has only one way to go and is already approaching higher bound of central banks’ targets. Nevertheless, yesterday’s ECB meeting showed that Mr Mario and co. don’t have any intentions to change their dovish stance, which seems as a headwind to all CEE central bankers that follow ECB but also have their own internal fights.

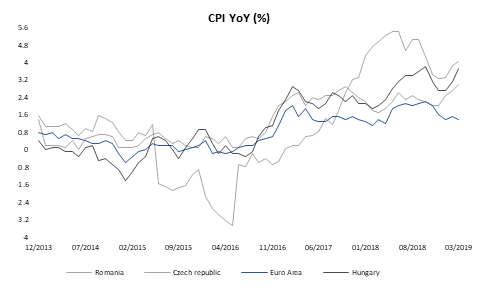

This week we have seen Romania, Czech Republic and Hungary publishing their inflation data for March and seems it surprised forecasters in all three cases. Although there are some similarities in all three countries its worth our while to briefly look at the cases separately and see what their central banks do to fight inflation.

Romanian CPI once again increased and stood at 4.0% YoY in March, compared to 3.8% YoY in February and 3.3% in both December 2018 and January 2019. As it was the case in almost all the countries in the region, increase mostly came from increased energy and food prices. In their minutes from the last meeting, NBR Board stated that all major CPI components had posted higher than expected increases and that they expect annual inflation most likely to stay above the upper bound of their 2.5% ± 1.0% target band due to very tight labor market, strong household consumption, increased energy prices and weaker RON. Also, they stated that RON could stay at its historical lows due to the ongoing worsening of external position of Romanian economy with risks tilted to the downside, i.e. they expect RON could weaken even more. Bearing in mind some external risks connected with trade wars and slowdown of biggest trading partners coupled with dovish ECB they decided to leave the key rate unchanged while maintaining strict control over money market liquidity reflecting slight hawkishness from NBR’s Board. In case inflation keeps rising, one shouldn’t be surprised if NBR increases its reference rate once or even twice this year even though external factors weigh to the opposite way.

Consumer price index change in Czech Republic on the other hand reached a seven year high of 3.0% YoY. Inflation is now 1.0% above the central bank’s target and we expect central bank at least changing its stance towards more tightening on the next meeting in the beginning of May. Namely, on their last meeting only two of seven members voted for rate hike with slightly dovish stance connected with external factors, i.e. slowdown of euro-zones growth. However, still high levels of EURCZK which bank forecasts at 25.20 in the end of the year, lowest unemployment rate in EU and record high inflation, hike on May 2nd shouldn’t be out of cards. Still, one should have any eye on Brexit talks due to UK being significant trading partner and could negatively affect Czech economy in case of messy exit.

Lastly, Hungarian inflation also surpassed analysts’ expectations, reaching multi-year highs of 3.7% YoY in March. However, Hungarian central bankers are not keen to make an U-turn in their policy as it was seen on their last meeting. Namely, they decided to hike its interest rate on deposits from -15bps to -5bps saying that hike was designed to be only one-off. Furthermore, they decided to introduce new measures to stimulate the economy with new unconventional policy in which MNB will buy bonds from non-financial corporations. Due to extremely loose stance, Hungarian Forint is once again trading around 322 levels.

Talking about central banks, we should note that yesterday’s ECB meeting was quite non-event with

Source: Bloomberg, InterCapital

At the current share price, the dividend yield is 5.5%.

Krka published a document in which they proposed

Note that the ex-dividend date is not yet proposed.

In the graphs below, we are bringing you a historical overview of the company’s dividend per share and dividend yield. Note that this would be the highest dividend yield in the observed period.

Dividend Per Share (2009 – 2019) (EUR)

Dividend Yield (2009 – 2019) (%)*

*compared to the share price day before the dividend announcement

Administrative Court of Slovenia, rejected the appeal to the decision of the Insurance Supervisory Agency, which denied Adris grupa and Croatia Osiguranje the right to increase their share above 20% in Sava Re.

Croatia Osiguranje released an announcement in which they stated that the Administrative Court of Slovenia, rejected their appeal to the decision of the Insurance Supervisory Agency, which denied them the right to increase their share above 20% in Sava Re. Since Sava Re is considered to be an important investment by the Slovenian Government the Government’s share can’t fall beneath 25% and no other shareholder may own more shares than the Government.

As a reminder, the Slovenian Regulatory Agency denied Adris grupa and Croatia osiguranje the right to acquire additional shares of Sava Re several times now. However, when filing their appeal last time, the Administrative Court ruled in their favour, annulling the decision of the regulator.

In Q1 2019, net sales revenue increased by 8%, amounting to EUR 59.6m.

Luka Koper published a document in which they announced their Q1 2019 net sales revenues and throughput. According to the report, in Q1 2019, net sales revenue increased by 8%, amounting to EUR 59.6m.

In the first three months of 2019, throughput decreased by 2.6% YoY. The decrease could mainly be attributed to the high fluctuation in certain cargo groups. When observing the throughput of vehicles (in units), they amounted to 169,496, representing a decrease of 17% YoY. The decrease occurred mainly due to unusually high volumes in Q1 2018. The company notes that the car throughput has been very volatile in recent months, probablydue to the situation on the global automotive market. However, the volumes of cars have been growing since January 2019.

In the table below, you can see the company’s throughput for Q1 2019 compared to Q1 2018.

| wdt_ID | Throughput (tons) | Q1 2019 | Q1 2018 | change (%) |

|---|---|---|---|---|

| 1 | General Cargo | 368.964,00 | 373.803,00 | -1,30 |

| 2 | Containers | 2.428.182,00 | 2.316.769,00 | 4,80 |

| 3 | Cars | 258.138,00 | 306.812,00 | -15,90 |

| 4 | Liquid Cargoes | 847.866,00 | 767.323,00 | 10,50 |

| 5 | Dry Bulk Cargoes | 2.016.228,00 | 2.312.398,00 | -12,80 |

| 6 | TOTAL | 5.919.378,00 | 6.077.105,00 | -2,60 |

In 2018, Sojaprotein recorded a decrease in operating revenues of 16% YoY, a decrease in EBITDA of 29% and a net loss of RSD 2.8bn.

As Sojaprotein published their 2018 results, we are bringing you some key takes from the report. According to it, the company recorded operating revenues of RSD 14.4bn (EUR 121.6m) which represents a decrease of 16% YoY. In 2018, Sojaprotein observed the highest decrease in revenues in soybean by RSD 872m (-110%) and raw soybean oil by RSD 739.6m (-25%). When observing the foreign market, the company recorded a decrease of 14.1% and amounted to RSD 9.1bn (EUR 77.3m).

Operating Revenues (2015 – 2018) (RSD bn)

Furthermore, operating expenses in 2018 decreased by RSD 2.6bn (-15%). This decrease could mostly be attributed to the fall in material costs of RSD 2.1bn. Going further down the P&L, Sojaprotein recorded EBITDA of RSD 348.7m (EUR 2.9m) which represents a decrease of 29%.

In 2018 the company recorded a net loss for the third year in a row, which amounted to RSD -2.8bn (EUR -23.6m) which is a reduction of RSD 3.7bn compared to 2017.

However, note that in 2017, Sojaprotein had high expenses from value adjustments which amounted to RSD 5.9bn (EUR 49.9m), compared to 2018 when they amounted to RSD 1bn (EUR 8.9m).

EBITDA & Net Income (2015 – 2018) (RSD bn)

To read more about Sojaprotein click here.

As OMV Petrom published their Q1 2019 key performance indicators, we are bringing you key takes from the report.

OMV Petrom published a document in which they state the information on the economic environment, as well as OMV Petrom Group’s key performance indicators for Q1 2019. These can be seen in the tables below.

Note that the OMV Petrom Group’s Q1 2019 results will be published on 3 May 2019.

| wdt_ID | Economic environment | Q1/18 | Q2/18 | Q3/18 | Q4/18 | Q1/19 |

|---|---|---|---|---|---|---|

| 1 | Average Brent price (USD/bbl) | 66,82 | 74,39 | 75,16 | 68,81 | 63,13 |

| 2 | Average Urals price (USD/bbl) | 65,17 | 72,74 | 74,16 | 68,33 | 63,42 |

| 3 | Average USD/RON FX-rate | 3,79 | 3,90 | 4,00 | 4,08 | 4,17 |

| 4 | Average EUR/RON FX-rate | 4,66 | 4,65 | 4,65 | 4,66 | 4,74 |

| wdt_ID | Downstream Oil | Q1/18 | Q2/18 | Q3/18 | Q4/18 | Q1/19 |

|---|---|---|---|---|---|---|

| 1 | Indicator refining margin (USD/bbl)* | 6,56 | 6,72 | 6,62 | 5,27 | 3,62 |

| 2 | Refinery utilization rate (%) | 94,00 | 49,00 | 98,00 | 99,00 | 96,00 |

| 3 | Total refined product sales (mn t) | 1,12 | 1,13 | 1,39 | 1,35 | 1,18 |

* The actual refining margins realized by OMV Petrom may vary from the indicator refining margin due to different crude slate, product yield

| wdt_ID | Downstream Gas | Q1/18 | Q2/18 | Q3/18 | Q4/18 | Q1/19 |

|---|---|---|---|---|---|---|

| 1 | Gas sales volumes to third parties (TWh) | 12,13 | 9,51 | 7,54 | 9,74 | 9,79 |

| 2 | Net electrical output (TWh) | 0,89 | 0,42 | 1,04 | 1,48 | 1,08 |

| wdt_ID | Upstream | Q1/18 | Q2/18 | Q3/18 | Q4/18 | Q1/19 |

|---|---|---|---|---|---|---|

| 1 | Total hydrocarbon production (kboe/d) (1+2) | 162,00 | 160,00 | 160,00 | 156,00 | 153,00 |

| 2 | 1) thereof crude oil and NGL production (kboe/d) | 73,00 | 74,00 | 74,00 | 72,00 | 71,00 |

| 3 | 2) thereof natural gas production (kboe/d) | 89,00 | 86,00 | 87,00 | 84,00 | 82,00 |

| 4 | Total hydrocarbon sales volume (mn boe) | 13,50 | 13,70 | 13,70 | 13,30 | 12,80 |

| 5 | Average realized crude price (USD/bbl) | 57,36 | 64,65 | 66,35 | 59,71 | 55,66 |