This Sunday, 22 March 2026, the Slovenian parliamentary elections were held, and the results are as close as possible. According to the newest numbers, Gibanje Svoboda, Robert Golob’s current Government-leading party, won 28.62% of the vote, receiving 29 seats. Janez Janša’s SDS is following them closely behind at 27.95%, winning 28 seats. NSi/SLS/FOKUS won 9.29% of the vote, representing 9 seats. SD and Demokrati meanwhile, won 6.7% of the vote, representing 6 seats each, while Levica and Resni.ca won 5.58% and 5.53% of the vote, representing 5 seats each, respectively. In other words, no party has a majority, and coalition talks in the coming period will determine who will lead the Slovenian Government. In any case, below we present our expectations as to what impact any of these parties in power will have on the Slovenian blue chips.

The Slovenian parliamentary elections were closer than ever this year, with the first 2 parties, GS and SDS, winning 28.6% and 28% of the vote, earning them 29 and 28 seats, respectively. NSi/SLS/FOKUS won 9.29% of the vote, or 9 seats. SD and Demokrati both won 6.7% of the vote, representing 6 seats each, while Levica and Resn.ca won 5.58% and 5.53% of the vote, representing 5 seats each, respectively.

Slovenian parliamentary election results vs. poll averages (2026, %)

| wdt_ID | wdt_created_by | wdt_created_at | wdt_last_edited_by | wdt_last_edited_at | Ticker | Poll average (%) | Actual result (%) |

|---|---|---|---|---|---|---|---|

| 1 | GS | 27,90 | 28,62 | ||||

| 2 | SDS | 25,60 | 27,95 | ||||

| 3 | NSi/SLS/FOKUS | 8,10 | 9,29 | ||||

| 4 | SD | 6,90 | 6,70 | ||||

| 5 | Demokrati | 7,70 | 6,70 | ||||

| 6 | Levica/Vesna | 8,10 | 5,58 | ||||

| 7 | Resni.ca | 4,10 | 5,53 | ||||

| 8 | Others | 11,60 | 9,60 |

Source: State Election Commission (DVK), InterCapital Research

The turnout for the election stood at 68%, a decline of app. 2.4 p.p. compared to 2022. As compared to that year, GS lost 12 seats, SDS and SD both gained 1, NSi/SLS/FOKUS also gained one, SD lost one, Demokrati gained 6, Resni.ca gained 5, while Levica remained at 5 seats, the same as the last election. After the election, GS’s leader, Robert Golob, claimed victory with a defiant yet measured tone, saying: “Since we have received the confidence, now we can think about going forward under a free sun”, also promising to “do everything to grant a better future to all citizens in our next mandate”. Golob also mentioned that he would invite all the parties for coalition talks, although he previously indicated his willingness to negotiate with all parliamentary parties except SDS.

On the other hand, the 2nd party with the highest number of votes, SDS, had a different view. Their leader, Janez Janša, had a more combative tone, describing the vote as a “referendum on corruption”, in reference to the secretly recorded videos. He also said that he was ready to challenge the result, citing his own party’s data that put him ahead. He also warned that “there will not be much political stability” after the ballot. Lastly, he signaled that he would not form a fragile government.

Slovenian parliamentary election results based on the estimated number of seats won in 2026

| wdt_ID | wdt_created_by | wdt_created_at | wdt_last_edited_by | wdt_last_edited_at | Ticker | 2022 seats | 2026 seats |

|---|---|---|---|---|---|---|---|

| 1 | GS | 41,00 | 29,00 | ||||

| 2 | SDS | 27,00 | 28,00 | ||||

| 3 | NSi/SLS/FOKUS | 8,00 | 9,00 | ||||

| 4 | SD | 7,00 | 6,00 | ||||

| 5 | Demokrati | 0,00 | 6,00 | ||||

| 6 | Levica/Vesna | 5,00 | 5,00 | ||||

| 7 | Resni.ca | 0,00 | 5,00 | ||||

| 8 | Minority deputies | 2,00 | 2,00 |

Source: DVK, InterCapital Research

It should be noted that to form the majority Government in the parliament, 46 seats are required. As such, the coalition talks will be the ultimate determinant as to who will lead Slovenia moving forward. While it is too early to say as to who will succeed in this task, below we present the most likely coalitions, not just based on what was said during the campaign, but also on the political alignment of the parties.

Possible parliamentary coalitions in Slovenia in 2026

| wdt_ID | wdt_created_by | wdt_created_at | wdt_last_edited_by | wdt_last_edited_at | Ticker | Parties | Combined seats |

|---|---|---|---|---|---|---|---|

| 1 | Grand centre | GS + SD+ NSi/SLS/FOKUS + Demokrati | 46,00 | ||||

| 2 | Minority Government (GS-led) | GS + SD + levica/Vesna | 40,00 | ||||

| 3 | Snap elections | No coalition formed | 0,00 | ||||

| 4 | Left-centre + Nsi | GS + SD+ Levica/Vesna + NSi/SLS/FOKUS | 46,00 | ||||

| 5 | Left-centre + Demokrati + Resni.ca | GS + SD + Levica/Vesna + Demokrati + Resni.ca | 46,00 | ||||

| 6 | SDS-led cross aisle | SDS + NSi/SLS/FOKUS + Demokrati + Resni.ca + SD | 48,00 | ||||

| 7 | SDS right-bloc only | SDS + Nsi/SLS/FOKUS + Demokrati + Resni.ca | 40,00 |

Source: InterCapital Research

Since 46 seats are required for the majority, this is the base requirement that any coalition, independent of their alignment, has to fulfil. The “Grande centre” coalition, which would include Svoboda (GS), SD, NSi/SLS/FOKUS and Demokrati, would be able to reach 46 seats, but there would be certain things that would have to occur for this: NSi would have to break its pre-election pledge to refuse left-centre coalitions, while Logar (leader of Demokrati) would have to accept Golob as Prime Minister. However, it should be noted that Golob’s coalition management track record is poor, with seven ministerial departures, the Litijska scandal, and the Roma crisis, which would increase the demands of any potential coalition partners.

The 2nd likely scenario would actually be a minority Government, also formed around GS, in combination with SD, and Levica. This option is inherently unstable, as it does not have enough seats (40/46), and would require the opponents to fail to unify the 46 votes against, thus relying on ad-hoc support per vote.

The 3rd option would include no coalition actually being formed, leading to snap elections. Given the tight difference between the 2 highest ranked parties, and many differences in preferences between parties, this is actually a viable option, and it would add several months of additional uncertainty. There are other combinations that could end up in power, based around SD, but again, the variety of parties & their aims make this less likely.

The 4th option would be the SDS, Janša-led party block, which could include SDS + NSi/SLS/FOKUS + Demokrati + Resni.ca + SD, although the chances for this occurring are currently very low, even though it would end up at 48 seats. Out of all of these parties, SDS has a natural alliance with NSi/SLS/FOKUS and Demokrati, with potential to add Resni.ca after talks, but the block would then require 6 more seats for a majority, and the only party that could provide them are the Social Democrats, SD, with 8 seats. But their joining SDS is highly unlikely, as the Black Cube scandal is currently being linked to Janša, and a coalition with his party would infuriate the SD voter base.

The last option is a minority government led by SDS, excl. The SD, although this option is basically a coalition dead on arrival, is thus unlikely to occur. Besides these options, a mix of different parties could also occur, but again, only time will tell who would win.

Now that we have at least some sense of the complexity of Slovenian politics, one could reasonably ask: what impact could this have on Slovenian blue chips?

Slovenia’s ownership* in Slovenian blue chips (as of 28 February 2026)

Source: SDH, InterCapital Research

*Includes both direct and indirect ownership

First, we have to look at several variables: the ownership of the State in these companies, their strategic importance, and what direction any possible Government would take these blue chips, through new regulations/laws moving forward?

As we can see, there are 3 companies which include above 50% State ownership: Telekom Slovenije, Triglav, and Luka Koper. There are several companies with State share between 20% and 35%, and only 1 Company with less than 20% State ownership. For our impact scenarios, we assume two different coalitions: One led by Robert Golob’s GS and the other led by Janez Janša’s SDS.

Scenario A: GS forms the majority Government

In case that Golob’s GS forms the majority Government, we expect that he will be PM again, although options in which he isn’t but is still a prominent figure inside the coalition are possible. His 2022 – 2026 track record centred on an expanded welfare state funded by higher taxes and contributions. Between 2023 and 2026, total labour burden grew by 3.2 p.p. in the country. The Government also raised the minimum wage to EUR 1,482 gross, introduced a mandatory long-term care contribution, abolished and replaced the complementary health insurance, introduced a mandatory winter bonus, and raised public sector wages by 10%.

Now for the possible impact on each blue chip:

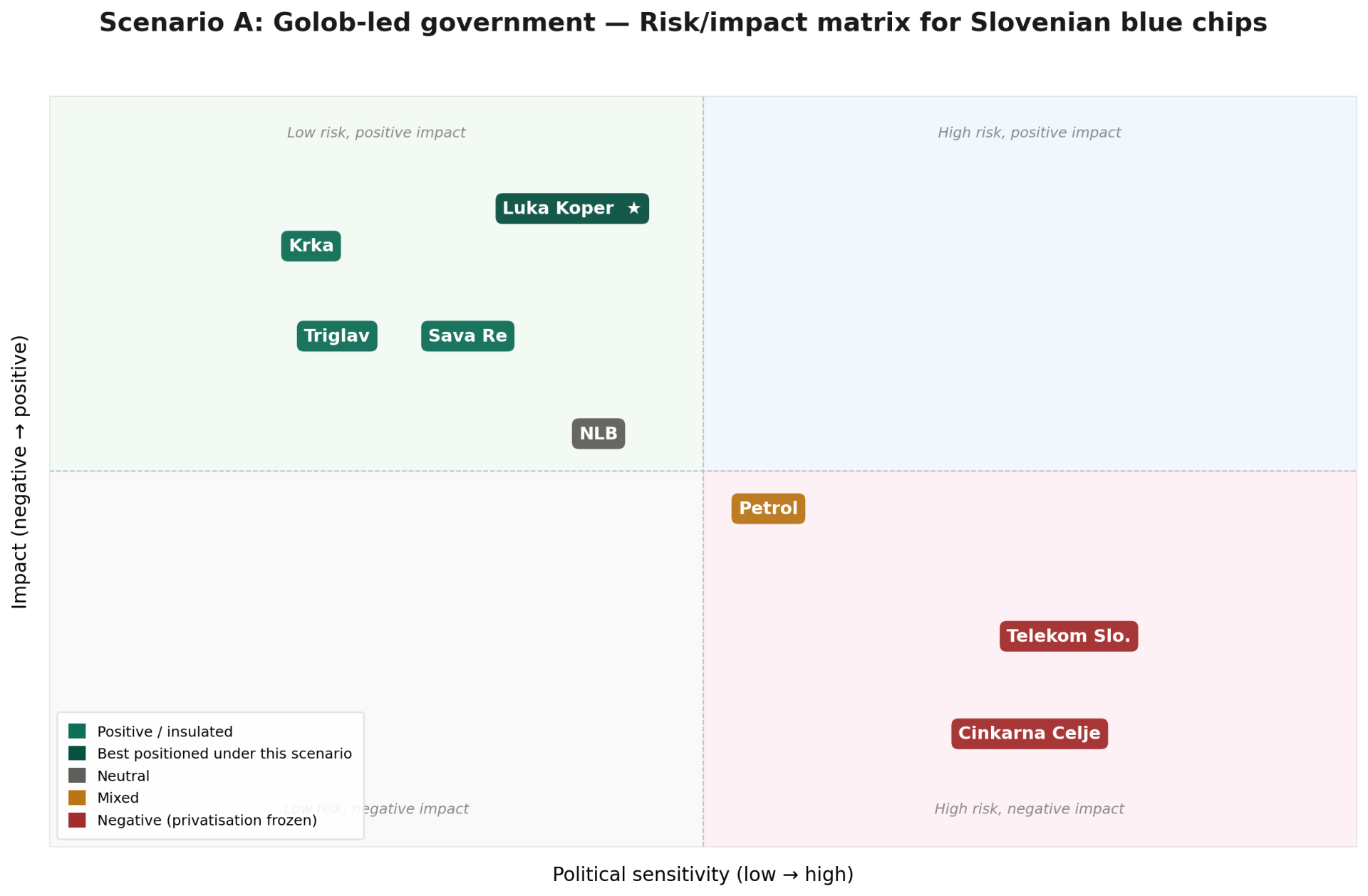

Telekom Slovenije, which was under the Golob-led Government, upgraded from “portfolio” to “important” in 2024, imposed a minimum 25% +1 ownership floor, effectively shelving any privatization of the State’s share. A new GS-led coalition would maintain this classification, and any coalition partners are unlikely to change this, as it was GS’s policy even without any partner concessions in the last couple of years. The telecom industry is a mature sector with a limited organic upside potential, thus making the dividend yield the primary return mechanism for shareholders. As such, we expect no changes in their case.

Moving on, NLB’s 25% state ownership should stay unchanged, as it is a binding EC commitment from the post-crisis restructuring. The previous Golob Government did not interfere with NLB’s regional expansion or operational independence, and this is likely to continue. There are some negatives, however, mainly due to the tax environment, as higher payroll taxes and contributions increase the cost base for Slovenian operations, although this is something that would affect all Slovenian companies. There could be some potential pushes for tighter regulation on banking fees, expanded social lending mandates, etc., but this is more unlikely than likely.

Petrol’s outlook remains mixed in the case of either party’s coalition. Under Golob’s Government, high infrastructure spending, due to flood reconstruction, road and rail investment, is supportive of their operations. Meanwhile, the Krško 2 NPP would be broadly positive for Petrol’s long-term positioning. As the country’s largest energy company and owner of 99.35% of gas supplier Geoplin, Petrol would benefit from a domestic nuclear baseload that reduces Slovenia’s dependence on volatile imported gas and provides long-term energy price stability in its home market. While it is likely that this could be advanced, certain coalition members could pose delays in the procedure. The more immediate headwind is the continued energy price regulation. The Golob Government imposed fuel, electricity, and gas price caps during its last term, significantly compressing Petrol’s margins. With the escalating conflicts in the Middle East, particularly around the Strait of Hormuz, oil and gas prices have grown significantly. A GS-led Government could impose additional consumer protection measures that would further pressure the Company as a distributor.

Krka, meanwhile, is disconnected from domestic politics, with 70% of the revenue outside the eurozone, so its changes and developments would be more tied to the global generic pharma dynamics. Neither side proposed changes to the pharmaceutical regulation, and as such, we do not expect a major impact on the Company, no matter which side wins.

For Luka Koper, in the case of Golob’s coalition forming, they would be the best-positioned blue chip. The expansionary fiscal approach directly benefited the port, with the flood reconstruction spending, Koper-Divača second railway track, and broader logistics corridor development all supporting throughput growth. Its strategic classification means that its ownership wouldn’t change, leading to no privatization risk. The continued investments in the hinterland connectivity and EU fund development continue to provide ongoing tailwinds. It should also be noted that the Koper-Divača railway enjoys full bipartisan support and EU co-financing, so this would not change under any different Government.

For the insurers, i.e. Triglav & Sava Re, Golob’s coalition would be neutral. The structural changes that affected the insurance sector, i.e. abolishing complementary health insurance, already happened and won’t be reversed. There remains a possibility of higher property taxes, which would marginally increase the insurable property risk pool, although this is unlikely. Both of these companies are more affected by the regional dynamics, good underwriting discipline, and the ECB rate environment, as well as the health of the EU as a whole, than by a particular party in power in Slovenia.

Lastly, Cinkarna Celje is the only blue chip classified as a freely disposable “portfolio” asset under the SDH strategy, meaning it could all be privatized. This is, of course, in theory. In practice, the Golob-led government had zero appetite for selling state-owned assets. We expect this trend to continue under the new Government. While we find this to be “negative”, it is negative only on this front. In general, the Company’s underlying business is sound, and it’s more tied to titanium dioxide prices and specialty chemicals fundamentals.

Estimated impact matrix of the GS-led coalition on Slovenian blue chips

Source: InterCapital Research

Scenario B: SDS forms the majority Government

SDS can be described as broadly pro-market, and its economic policies have been characterized as neoliberal. They advocate for lower taxes and speeding up privatization efforts. Besides this, they also aimed at reducing public spending, removing regulations, and lowering the deficit. The 2026 campaign is consistent with this history, with the aim of “turning off the taps” of unnecessary spending, reducing the public sector, and encouraging private investment.

We estimate the impact on each blue chip to be the following:

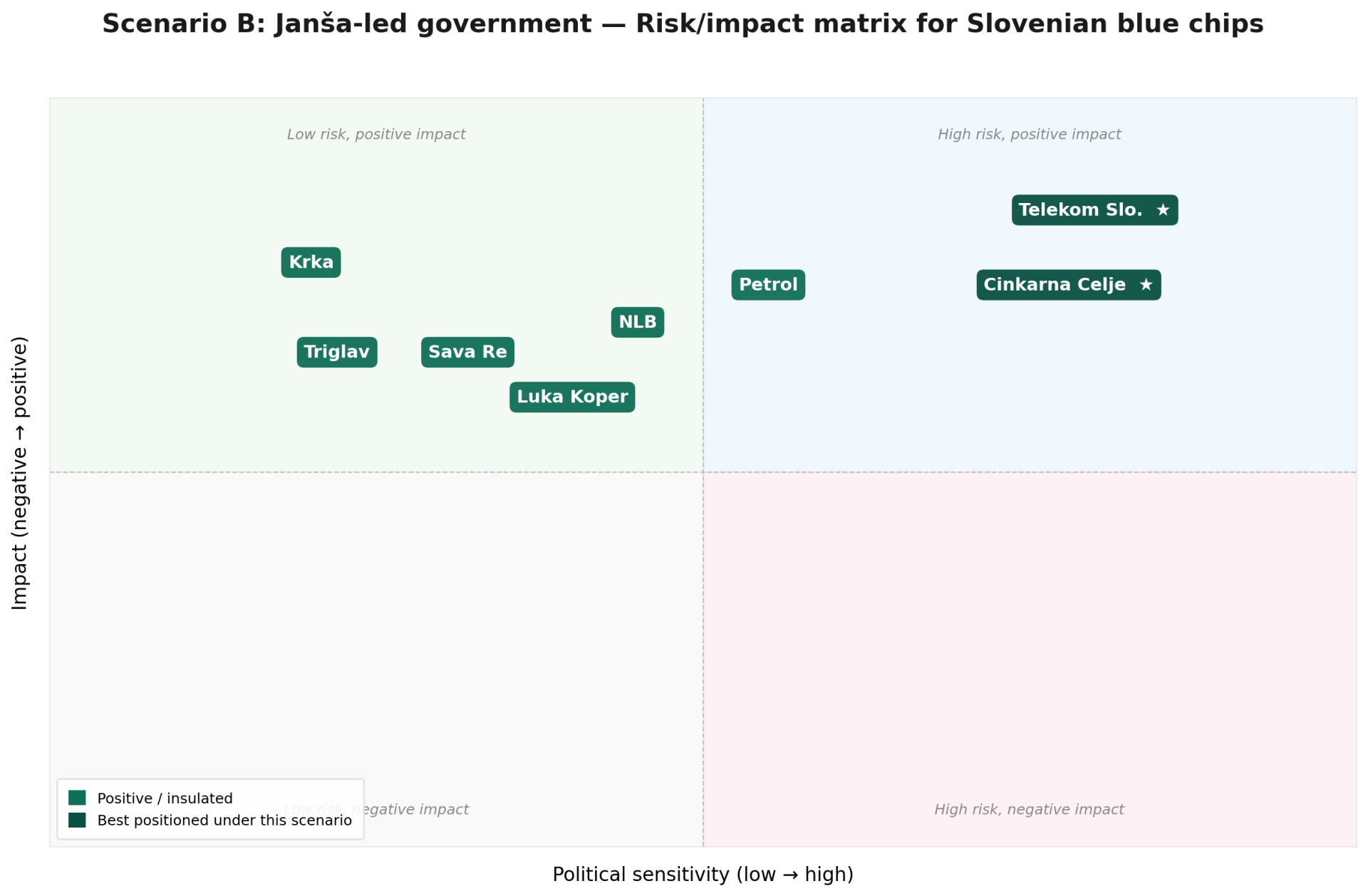

Telekom Slovenije’s outlook changes drastically as compared to the GS-led government, as the privatization efforts could actually be carried out. The first step would be reclassifying the SDH classification to portfolio from important. Other possible coalition members, such as NSi/SLS/FOKUS and Demokrati, would both support this direction. In case they lead the Government, we expect some movement on this front, which would be supportive of the share price, although it is hard to pinpoint when this would exactly occur, as other, more important issues would gain precedence.

For NLB, SDS’s victory could be seen as mildly positive. The party’s pro-market orientation translates to more commercially-focused SDH governance, clearer ROE targets, less political interference in board appointments and potentially more generous dividend policy mandate. The regulatory environment could also be changed to be more supportive of NLB’s regional expansion, while lower payroll taxes would benefit the Group’s Slovenian cost base.

For Petrol, SDS’s victory could also be seen as positive, as the entire coalition would be supportive of the Krško 2 NPP, providing long-term strategic clarity to Petrol. Lower payroll taxes would also lower Petrol’s domestic operating costs. Thirdly, SDS’s possible deregulations could also affect Petrol’s energy price caps, although this is unlikely in the short to medium term, regardless of which party forms the coalition, due to the conflict in the Middle East. On the other hand, SDS’s pledge to reduce public spending could reduce infrastructure investment, which could indirectly affect Petrol as well.

Luka Koper’s position is unlikely to change under SDS’s leadership, as bipartisan support and EU co-financing are present for many of its investments or those adjacent to it. SDS’s pro-business orientation could accelerate regulatory permitting for port expansion and attract private logistics investment to the Koper corridor. On the flip side, reduced public spending could partially offset this impact. In either case, the port’s position is secured.

For Krka, like with the GS-led government, the impact is mostly neutral. It could benefit from the possible tax reform under SDS, as well as improvements to SDH governance. In general, however, it still remains mostly disconnected from political changes in the country. Likewise, the 2 insurers, Triglav and Sava Re, could marginally benefit from better SDH governance, although we do not expect any major changes as to how it was set up until this point. Lastly, Cinkarna Celje’s case is similar to Telekom Slovenije. As it’s in an even better position, privatization-wise, the sale of the 24.44% stake could occur quickly, marking a win for the SDS’s pro-privatization mandate. A trade or a secondary offering would reduce political overhang and could attract strategic or financial buyers interested in the Company’s operations.

Estimated impact matrix of the SDS-led coalition on Slovenian blue chips

Source: InterCapital Research

In general, no matter which party wins, in the short term, no major changes are expected. Privatizations could take place under the SDS-led government, but this remains one of the items on the agenda and not the primary one. It is worth noting that the Black Cube investigation remains ongoing, with the Slovenian authorities probing the allegations, and Golob has requested an EU-level inquiry. Any significant escalation, such as formal charges or EU-level action, could introduce headline risk for Slovenian assets, especially if it prolongs coalition uncertainty or damages the country’s institutional credibility with international investors.

With all of that taken into account, we find that the macroeconomic and geopolitical changes in Europe and globally, especially with the conflicts and uncertainty occurring around the world right now, would be larger drivers for Slovenian blue chips than different political parties ruling, especially in the short to medium term.