It’s perhaps a coincidence that a WWII pivot and the ECB pivot take place on the same date, just 80 years apart. The D-Day (June 06th, 1944) and ECB’s first-in-a-while interest rate cut (June 06th,2024) both mark turning points, although the first pivot is a truly historic milestone, while the second date is something noticed only by financial experts. Luckily a lot of these are in the ranks of our readers. What do we make of ECB rate cuts this year? Find out in this brief research piece.

We’re looking at the quite intensive week in terms of hard data and central bank decisions, so let’s take it step by step.

On the last day of May S&P downgraded France from AA to AA- with a stable outlook. If you missed the news, you didn’t miss anything really because market reaction has been muted. With EGB spreads to Germany already razor-tight across the board, it would be unreasonable to expect a sharp rise in borrowing costs for the second-biggest auro area economy. And now onto more important things.

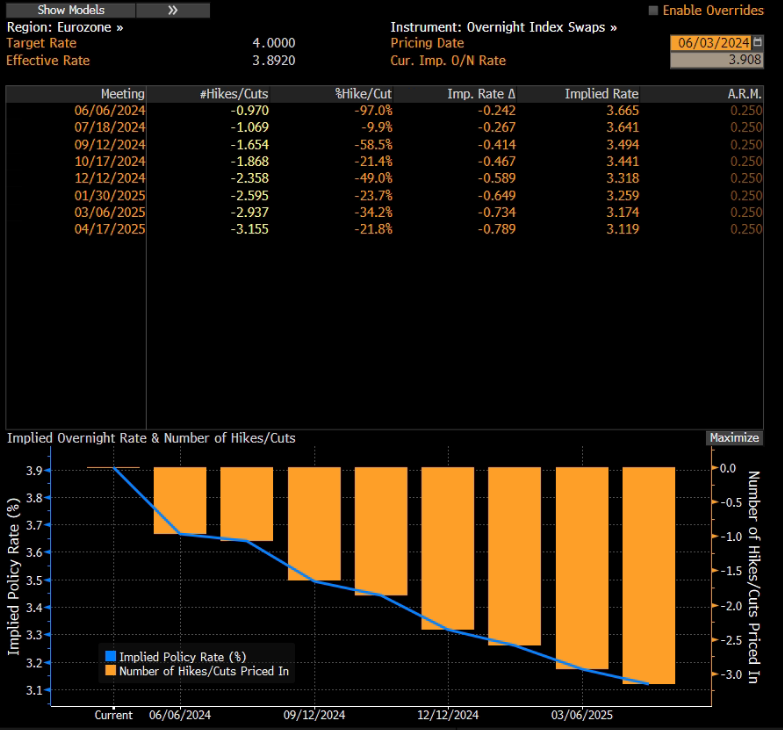

This Thursday is marked by ECB pivoting to rate cuts with an inaugural 25bps rate cut – this promise is so rock solid that you can take it to the bank and use it as collateral for a loan. The real question is what happens next? Isabel Schnabel discarded the probability of a July cut because there simply won’t be enough hard data to corroborate a consecutive cut, although there is a consensus within the ECB that more cuts would be warranted. ECB Vice President de Guindos, Bank of Greece Governor Stournaras and Bank of Lithuania Chairman Simkus are the three GC members advocating for three cuts this year and it’s quite unclear whether they will really get it. In our view, Isabel Schnabel is trying to buy time in order to coordinate actions with other G4 central banks in Jackson Hole (end August), a move that might warrant no EUR depreciation even if the FED decides to abstain from cuts this year (not our baseline scenario, but quite possible). This would mean that hawks and doves within the ECB might find common ground on the September cut, with a bit of luck with no EUR weakness warranted.

What are the odds of the ECB turning the corner in the same manner that the FED did just a couple of months earlier? In plain English – what if ECB GC members get cold feet and put cuts on pause because of EURUSD nosedives 2022-style? Let’s take a look at the US hard data to find an answer for this. Seems that US stagflation scenario is a particular issue for the FOMC and that members currently have no playbook to address it. Remember, stagflation essentially means the environment where FED wants to cut rates, but the inflation data doesn’t allow it. Be mindful of the most recent beige book and GDP data. Although one is a really, really soft indicator, and the other one is prone to seasonality, meaning that one bad quarter essentially means nothing at all. At the very source of the stagflation scenario are sticky service prices that won’t come down that easily, but we also point out that contrary to Neel Kashkari’s remarks hiking rates are not a panacea for stagflation. We also think that it is possible that if the FED does delay cuts and elevated interest rates actually do work with a long and variable lag, FOMC will have to frontload severe rate cuts in early 2025. With that in mind, the ECB can proceed with two or even three rate cuts this year. EURUSD won’t break parity.

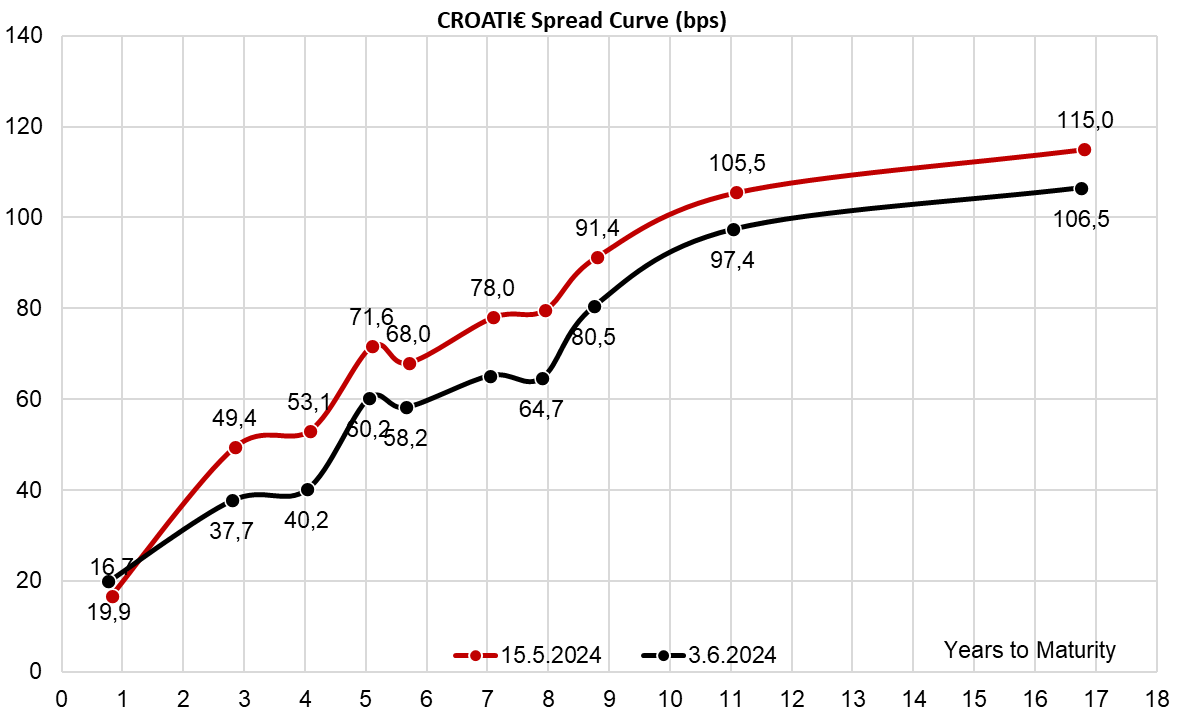

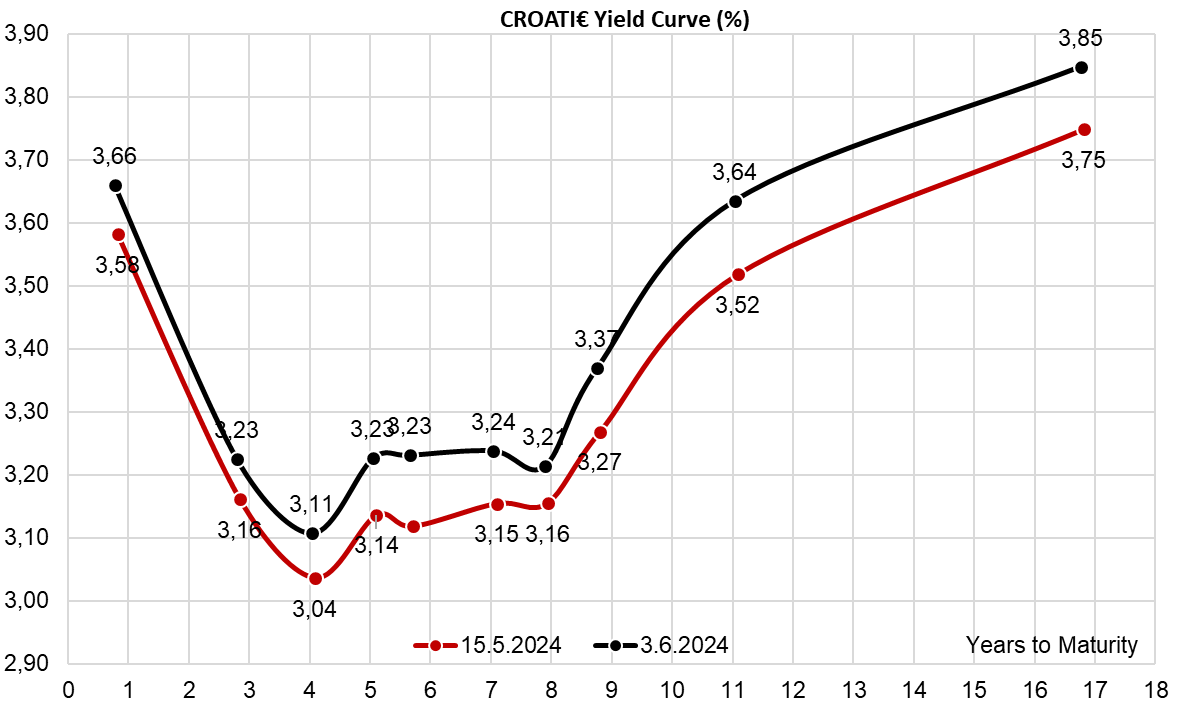

Finally, what’s going on with CROATI€ curve? We find the recent spread tightening quite curious but notice that it wasn’t isolated just on CROATI€ paper, meaning that it has nothing to do with prospects of Croatian credit rating moving deeper into IG. With no international placements this year and only retail bonds on schedule for the remainder of the year, it is possible for CROATI€ spread to Germany to continue contracting. Yes, you read it correctly. Croatia is below 100bps on Germany still has room to tighten. However, be mindful that in March 2025 Croatia will have to go through a mega-bond rollover with CROATI 3 01/11/2025€ (that’s 1.5bn EUR), CROATE 0.25 03/03/2025€ (another 663mm EUR) and CROATE 3.65 03/08/2025€ (1.85bn EUR – a true bazooka) all mature in a span of eight days. Our point: keep some dry powder for a splash of issuances in March 2025. It’s not that far away.