Recently yields have been drifting higher as the market began to believe that higher rates for longer is the path that both ECB and Fed will follow. In addition to that, the market raised expectations of the terminal rate for both central banks. Currently, inflation seems to be stickier than previously thought and soft data is pointing out that both economies are in good shape, in better shape than we thought in the third quarter of 2022. Consequently, the start of the year for risky assets was terrific – growth expectations revised higher, and a hard landing seems to be an implausible scenario.

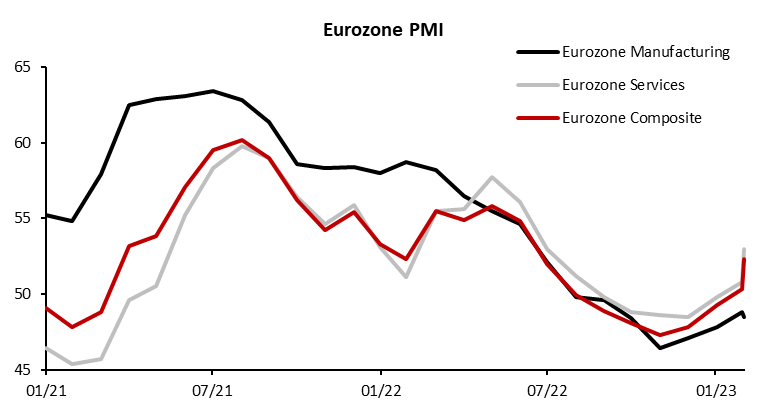

The Purchasing Managers Index for both Eurozone and US are pointing to growth. Composite PMI in Eurozone reached 52.3 in February which indicates an expansion of the economy, a level that was last seen eight months ago. In the second half of 2022, everyone feared the energy crisis in Europe, so it is reasonable that the PMI was below 50 from August 2022 until February 2023. The same situation applies to the US, but the soft data isn’t as optimistic as in Europe.

The two main components of the composite PMI are manufacturing and services PMI. The former is in the contractionary territory for both US and Eurozone. In the Eurozone, I would justify it with the deterioration of energy security and rapid price increases of gas, oil, and derivatives. On the other hand, contractions in the US can be attributed to the appreciation of the dollar which led to costlier exports and cheaper imports.

As the service sector accounts for a larger share of GDP than manufacturing, services PMI is recognized as more crucial data, and the market is much more sensitive to changes in services PMI than to changes in manufacturing PMI. Services PMI in Eurozone is deep in the expansionary territory at a level of 53 (February 2023) which was last seen last summer. As the soft data improved every month in the fourth quarter of 2022 and at the start of this year, the index of the German stock market DAX rose to the levels seen before the war in Ukraine. According to the market, it seems nothing happened to the valuation of German companies even as German 10-year and 2-year bond yields rose from the negative territory to 2.7% and 3.2%, respectively. Soft data in the US is surprisingly not as bright as in Europe. Consequently, S&P 500 is still pinned to the level of 4000 with oscillations of 5% lower and higher since November.

Unfortunately, a growth outlook focused on the services sector raised concerns about persisting inflation and delayed the fall in inflation to 2% as the hawkishness of central banks is in the spotlight again. Further expansion of the services sector accompanied by a tight labor market should further stimulate wage growth and make the task of bringing down inflation more difficult for central banks. Thus, the expectation of terminal rates has risen to new highs, reaching 3.87% for ECB and 5.45% for the Fed. Furthermore, Schatz’s yield rose 50bps over the course of February (2.60% to 3.15%).

A hard landing in both economies is improbable, but expectations in this volatile market environment are changing swiftly. At least the toughest winter that the Eurozone had to survive is behind us and prices of natural gas are down 86%. In case of inflation drops to 2% in 2024 and growth remains solid, it would be a goldilocks scenario for both the bond and equity market in 2024. The only thing I fear is the long-term relocation of energy-intensive European industry in case of natural gas prices ticking higher after the restoration of demand.

Source: Bloomberg, InterCapital