Last week, NLB held a 2-day event, including the Investor Day, during which it unveiled its new business strategy until 2030. The goals in the 2030 Strategy include reaching over EUR 50bn in assets by 2030, having recurring revenues of over EUR 2bn, profit of over EUR 1bn, a dividend payout ratio moving towards 50-60%, as well as a P/B ratio of over 1x. While these goals might seem ambitious, the track record of the Bank’s management in the last couple of years has proven that they can achieve their set goals. In this overview, we’ll detail the whole strategy and look at its feasibility from the current perspective.

While the 2030 Strategy might seem ambitious, it is set out across many initiatives in 3 segments: Retail, Corporate & Investment Banking, and Payments.

Retail

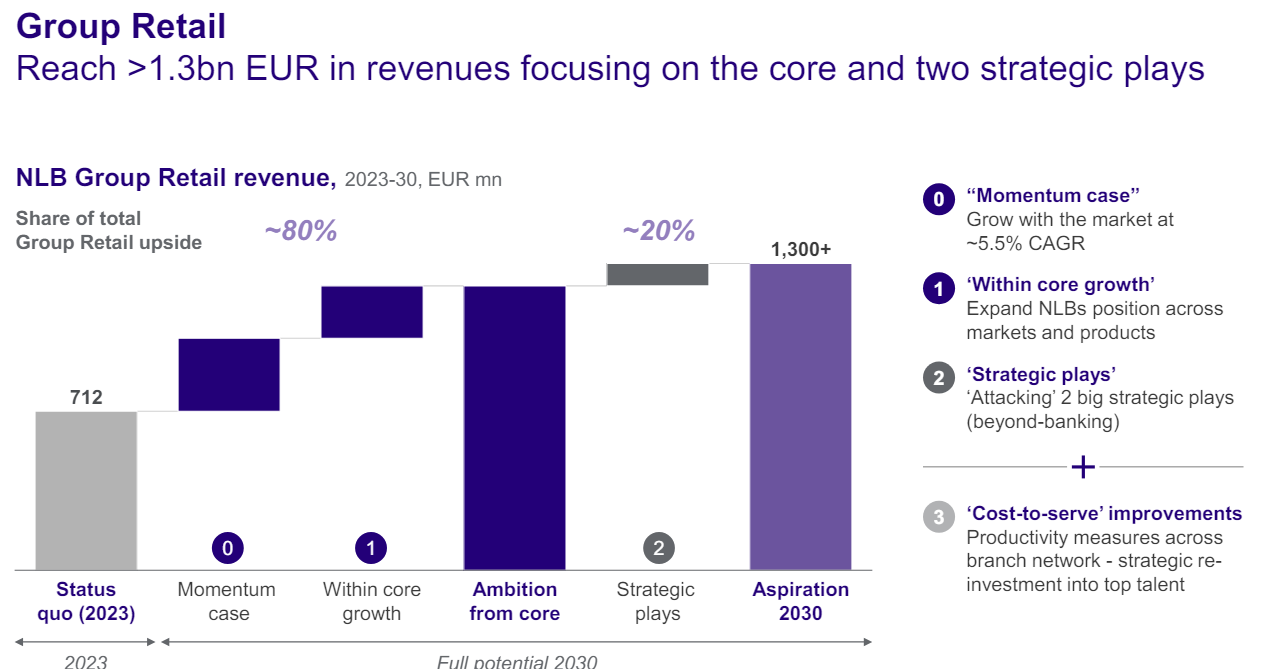

Starting with Retail, NLB currently holds the position of the largest bank in the SEE region, and its goal is to not only maintain but also expand the position. Thus far, this was achieved by growing the customer base to over 2.7m clients in the region, with just the Slovenian segment having over 700k clients. Also, NLB was able to grow at an 8% revenue CAGR thus far, with strong diversification (e.g. 30% fee contribution). Furthermore, the Group has diversified its services structure, offering investments, banc-assurance, leasing, payments, etc. to its clients.

The Group plans on expanding this further, reaching >3m clients by 2030 across all regions, growing the revenue per customer to over EUR 400 (2023: EUR 270), and achieving a revenue of EUR 1.3bn, implying a 9% CAGR until 2030. Furthermore, through digitalization efforts, they plan on reaching 80%+ digital penetration (currently: 39-60%).

NLB Group retail revenue development until 2030 (2023 – 2030, EURm)

Source: NLB Group

Besides organic growth, the Group plans on 2 strategic plays (previous outlooks: 1 strategic play of up to 4bn RWAs).

NLB Group Retail segment initiatives

Source: NLB Group

As we can see in the two previous graphs, the Group has set out goals which at the current rate of development do not seem that outlandish, and they are aimed at expanding the current business, especially in the less-developed regional markets.

Corporate & Investment Banking

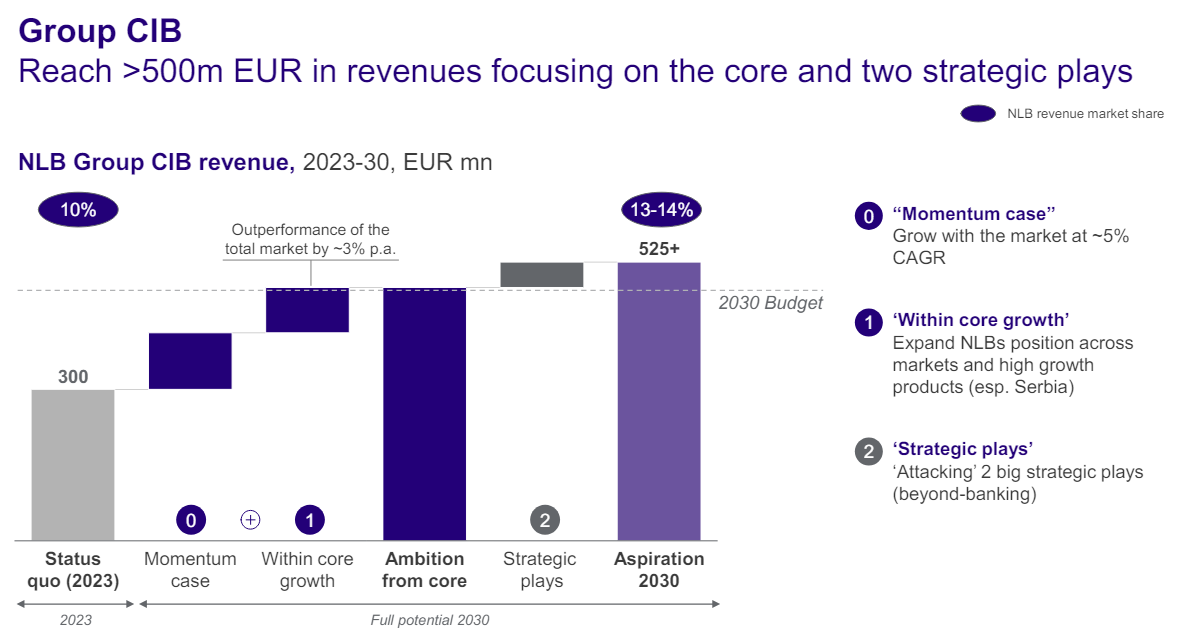

Meanwhile, in the Corporate & Investment banking (CIB) segment, NLB started by noting that the SEE region in general is growing faster than the EU in terms of real GDP, while at the same time, the regional companies are less indebted than the EU average. Suppose we combine the various EU funds’ contributions and the desire of SEE region countries to converge with the EU average (especially after the possible entry of more regional countries into the Union). In that case, it will mean that a lot of investments will have to be made in the coming years. These investments would of course have to be financed by debt, and NLB sees a strong opportunity for synergy in this regard.

Thus far, this has been supported by the fact that NLB has positioned itself as a strong CIB franchise in the region, with a clear market leadership position in Slovenia with app. 26% of loan market share. Furthermore, despite the challenging macroeconomic environment in the last couple of years, NLB was able to manage the risk well, resulting in both profitable book building as well as low NPL ratios. NLB plans on expanding its CIB playbook, which includes trade finance, corp. finance, as well as custody. If all goes as planned, they will be able to achieve EUR 3.2bn of new transition finance volume in 2030, EUR 500m in revenues, implying an 8% CAGR, <45% cost-to-income ratio, as well as a full (100%) digital onboarding for SMEs.

NLB Group CIB revenue development until 2030 (2023 – 2030, EURm)

Source: NLB Group

While no details were provided, the organic growth could once again be supported by 2 strategic plays. The full overview of the CIB strategic initiatives is available below.

NLB Group CIB segment initiatives

Source: NLB Group

If successful, NLB will be able to achieve revenue per active client of EUR 20k in 2030 (2023: EUR 12.5k), increase its fee income to over 37% of the total (2023: 27%), grow its total CIB stock loan volume from EUR 6bn in 2023 to over EUR 12bn in 2030, and achieve over EUR 1.3bn in Green financing stock (currently: EUR 0.3bn).

Payments

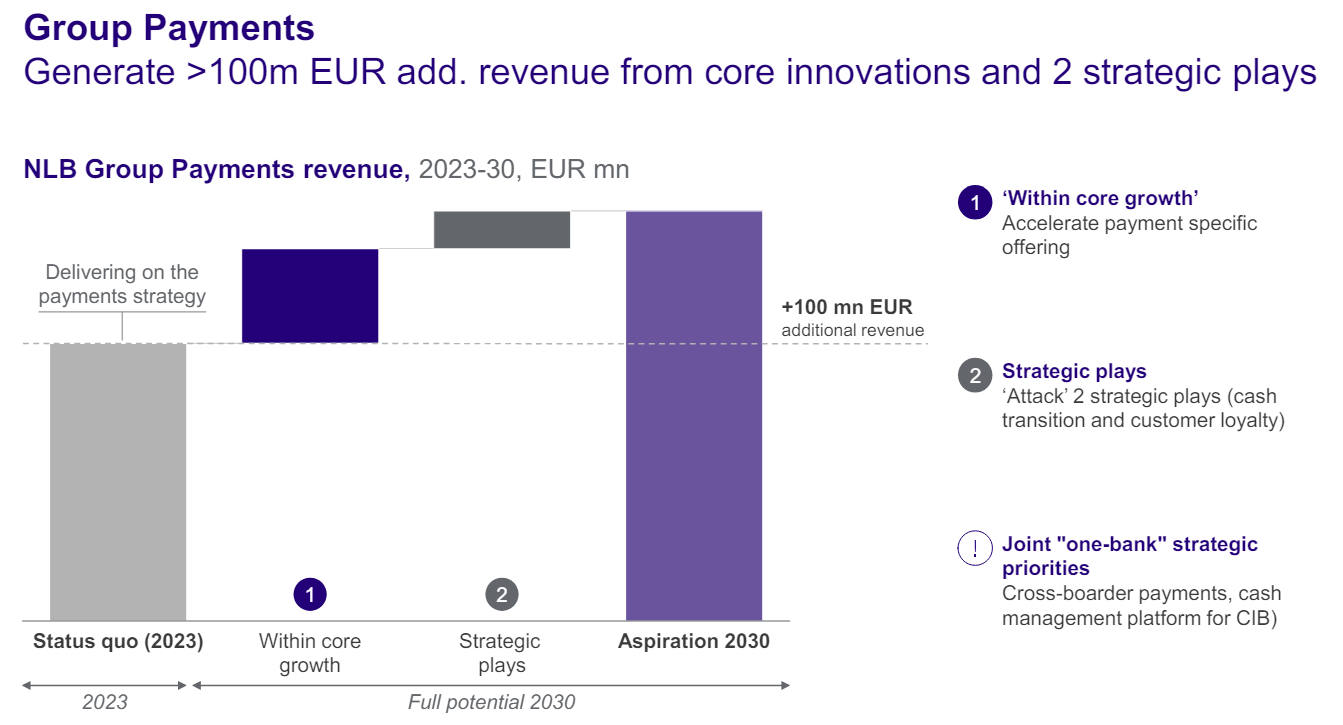

The last segment, i.e. Payments, was focused primarily on the transition from cash usage in the region towards a more cash-less society, and how NLB could position itself to take advantage of this. In general, regional markets still use cash far more than the EU average. Thus far until 2023, NLB has established payments as a core part of the Group, with EUR 220m+ of fee income, related to accounts, packages, cards, and payments. NLB also continues to be a regional front-runner for services such as instant pay, Apple Pay, Google Pay, merchant acquiring, and other digital payment innovations.

By 2030, they plan on rolling out more of these, with a focus on digital payments and merchant solutions. If this is achieved, by 2030 the Group will have >EUR 100m in incremental revenue, with >80% of mobile active by 2030.

NLB Group Payments revenue development until 2030 (2023 – 2030, EURm)

Source: NLB Group

To achieve these developments, NLB provides six strategic initiatives, which we detail below:

NLB Group Payments segment initiatives

Source: NLB Group

If all of this is achieved, this segment’s revenue contribution will grow to over EUR 320m in 2030 from EUR 220m today. Retail clients’ digital penetration will reach over 80% (2023: 25-60%), with increased penetration of mobile value, increased number of digitalized card transactions, and a lower number of Retail cash transactions in the Group’s branches.

When all of the aforementioned initiatives and developments across the different Group segments are combined, NLB has set a goal for itself of achieving over EUR 50bn of assets, doubling from the current level, having recurring revenues of >EUR 2bn (2023: EUR 1.1bn), ROE of >15% (2023: 21%), a payout ratio that goes towards 50-60% (currently: app. 40%), and a P/B of >1x (currently: 0.8x).

While all of these goals seem extremely ambitious, they would be achieved over 5 and a half years, leaving a lot of room. One thing that is important to note is that a lot of the growth in the banking sector in general, but for NLB too in the last couple of years came from the elevated interest rates. While it isn’t exactly yet known how low the rates will be cut once the rate cut cycle ends, it is unlikely that they will land in the negative territory or at 0% as they were before. This could leave NLB room for growth toward its goals, but until we know where the rate cuts end, it is hard to say if will it be achievable. At the same time, the Group still has a lot of room for growth in its regional markets outside of Slovenia, and with a larger focus on digital services and reduction of costs from branches as a result, there are still headwinds behind the Group.

The wildcard is of course, in the strategic plays, i.e. M&As. Previous M&As by the Group were always done at P/B levels of <1x, and if such opportunities present themselves, this could give another strong push toward these goals. Furthermore, the resolution of the legacy issues in Croatia could also open opportunities for growth in the region, and NLB’s management hasn’t hidden the fact that they desire to unite the whole region under the Group. However, no clear targets have been communicated.

Still, if the goals set out in the strategy are achieved, strategic plays would account for “only” 20% of revenue production, meaning that they would be a boost on top and not the main driver. While a lot of people were surprised at the announcements made during the Investor Day, especially regarding the high ambitions of the goals, one must remember that the current Management has achieved all of the goals that they’ve set out in the last couple of years, and this also includes several upgrades to outlooks. As such, it might be too early to count them out. After all, like NLB’s CEO said: “It’s not rocket science”.