In the most recent bond sell off induced by US CPI print and consequential FED speak, it was quite weird that our prospective buyers didn’t manage to get much bonds at significantly higher yields. Across the CEE board spreads are tightening. What do we make of this new regime? Find out in this brief research piece.

If you are puzzled about the current state of the financial markets, well at first so were we. On Tuesday afternoon Tesla reported 1Q2024 earnings and both top and bottom line came in below expectations (EPS @ 45 cents versus 52 cents; topline was about a billion USD below consensus estimate). However, the company also presented a colorful slide deck with forecasts about introducing new models nobody ever heard of and consequently the stock is now +11.8% up (162.13 USD versus 145 USD before the close Tuesday). At the same time, Meta reported earnings significantly above the consensus estimate (EPS @ 4.71 USD versus 4.30 USD consensus estimate) but is virtually flat versus the previous close.

Does this make any sense to you? Well, if you believe we’re in the narrative economics and if you were a close student of Aswath Damodaran, then maybe it does.

Here’s where things get really tricky. Bond yields are at a six-month high and gold prices are at an all time highs. How is that possible? Rumour from the dealing desks has it that Asian buyers are behind this, but we’re waiting for a plausible research piece from bulge bracket investment bank to confirm it. Either way, the old playbook of earnings-stock performance and bond/gold correlation has obviously been torn apart and new rules of the game are being settled down.

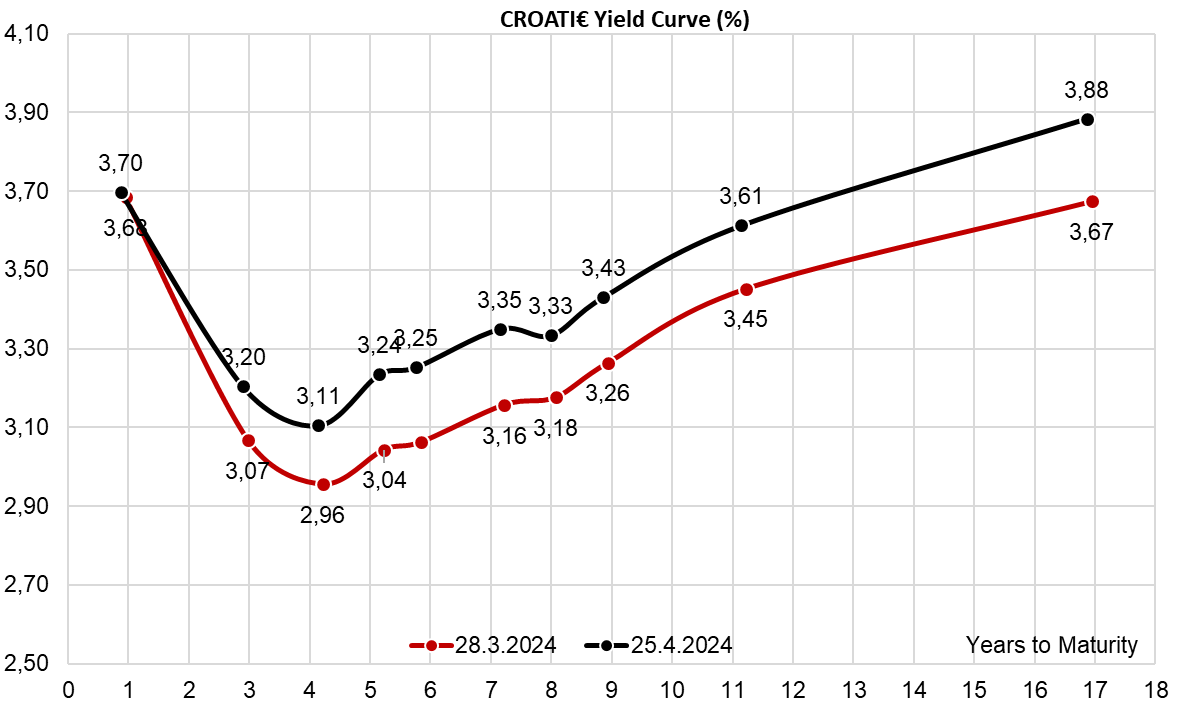

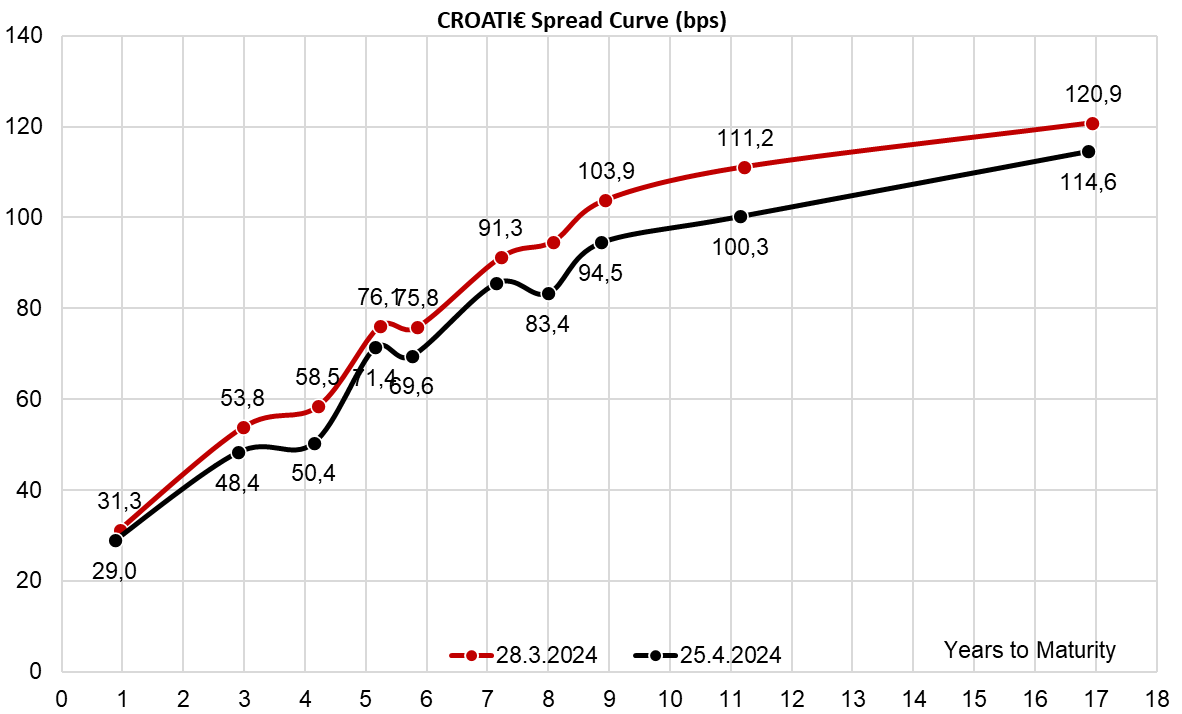

Now that we went through the context, let’s get to some of the finer details. Bond prices are at a 6-month low, however, the spreads appear to be trading tighter and rumors from dealing desks tell us that rise in yields was met with respectable buying interest from real money clients, preventing spreads from widening (take a look at CROATI€ spreads submitted above). Certain bonds such as POLAND€ are currently reporting a significant short interest, which is confirmed by anecdotal evidence of dealers asking around for POLAND€ through reverse repo. But actually, this is not such a surprise if you take a brief look at the two latest US treasury note auctions (2-year on Tuesday and 5-year on Wednesday). Speaking about the former, US Department of Treasury had no problem with placing 69bn USD of 2-year notes at 4.898%, which is lower than 4.904% before the auction. With a bid-to-cover of 2.66x (versus 2.62x on March 25th, 2.49x on February 26th and 2.57x on January 23rd) and primary dealers taking a record low of inventories, seems as if the bond market has drawn a cap for yields, at least for the time being. On the other side of the Atlantic, the ECB officials are not questioning the timing of the start of rate cuts, although they are still to come to terms with the aggregate number of cuts. All of this might be the reason why CEE€ investors tend to hold their assets and not participate in any additional sell off.

So what happens next? With US market pricing about 1.7 rate cuts this year (WIRP US submitted above), notice that market expectations are now below both median dot (3 cuts) and weighted average dot (2 cuts). Notice that according to the latest Summary of Economic Projections, median 2024 PCE inflation was expected to reach 2.4% this year and last month the read said 2.5% YoY; tomorrow BBG consensus expects a 2.6% YoY print, a close call. Speaking about Core PCE, FOMC median expects 2.6%, while BBG consensus expects to see 2.6% YoY tomorrow. Our point: PCE inflation is right where it’s supposed to be for the start of rate cuts. True, CPI came in a tad stronger, but not sufficiently to turn the narrative. Additionally, recent FED speak about the waiting game was probably targeting May meeting – and we agree, it’s too early to start or to telegraph rate cuts as soon as next week. On the other hand, there’s plenty of data until the next meeting in mid-June (two NFP prints, two CPI prints, two PCE prints). It’s very likely that Powell’s Q&A session will pledge data dependence, and when you take an unbiased look at the data, the narrative remains clear. So, yes, it makes perfect sense that CEE RM is not selling – but at spreads tight like this, it also makes very little sense to start buying as well.