Big QE package by ECB, PEPP, introduced two weeks ago is already in full force. Only in the first 5 days of PEPP, ECB spent EUR 30.2bn through the programme which envisages buying all assets eligible under existing APP but also buying Greek debt and non-financial commercial papers. ECB intends to buy up to EUR 750bn of eligible bonds and some investors hope that this will not be all. This week’s meeting of Eurogroup still didn’t deliver but we think they do not have much choice. ECB’s umbrella showed its full strength when announced, literally halving yields on Italian and Greece bonds. What are other consequences? Read in this short article.

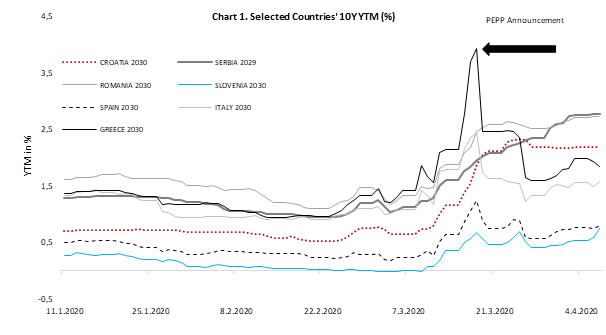

Last week we wrote about new issues on Eurobond market by Slovenia, Portugal and Latvia which have all seen great demand with bid to cover surpassing 2.0, resulting in yield being slightly above levels seen in February 2020. Off course, levels were there most likely due to bazooka from ECB rather than healthy demand from financial institutions. Peak of crisis (at least up to today) seemed to be on March 18th when Italian 10Y papers went above 3.0% while Greek peer surpassed 4.0%. Just to put things into perspective, only a bit more than month ago both Italian and Greek 10Y stood below 1.0% as yield hungry investors were buying every positive yield that they could find.

ECB’s long waited meeting on March 12th on which Ms Lagarde raised QE up to EUR 120bn didn’t get positive response from the market so periphery papers cratered. European periphery went down with speed that wasn’t seen since debt crisis and investors were selling bonds at every bid they found. Story turned around when Ms Lagarde announced PEPP (Pandemic Emergency Purchase Programme) only day after yields in periphery exploded and market was broken, resulting in massive recovery, i.e. periphery yields almost halved. Italian 10Y paper felt from almost 3.0% to around 1.5% while Greek one fell to below 2.0%. These were two most affected ones, but you get the point, bazooka it was.

After two weeks, we have some data by the ECB (only PSPP), showing that in March ECB purchased enormous amounts of Italian debt (almost 35% of all PSPP in March) which is way above capital key. In ECB’s data provided under PSPP, we could see that Italy, France and Spain bonds were the most beneficiaries of ECB’s programme in March as ECB bought EUR 11.85bn, 8.87bn and 5.40bn, respectively which amounts 70% of total March’s buying. Italian paper was bought in March in amount that was last time seen three years ago when ECB was buying EUR 80bn worth of papers a month. However, we still didn’t see detailed PEPP programme under which ECB bought another EUR 30.2bn worth of eligible papers in first 5 days.

So, it seems like yields in euro area are under control, at least for now. With pace of EUR30bn a week, ECB pandemic programme could last for at least 6 months but most likely market will not need such a support for long time. Looking at the equity markets, they were just waiting for new coronavirus numbers to decelerate and started to rocket again. Maybe that could be the case for bonds as well with renewed liquidity provided by central banks. At the moment we are not discussing the mountain of new debt that is coming every day as central banks seem to be eager to monetize the most of it and it’s a theme for another blog. When asked about rising debt, Mr Mario Draghi wrote in a recent article: “Much higher public debt levels will become a permanent feature of our economies”.

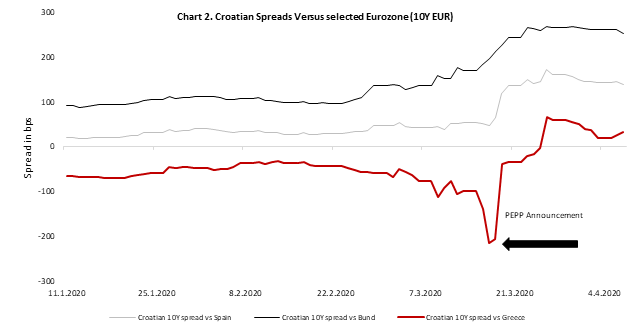

Talking about central bank’s umbrella, what happened with non-Eurozone sovereign yields? Well, they didn’t have ECB so spreads versus EA countries widened significantly. For the sake of this article, lets look at 10Y yield on several EU non-EA sovereign EUR papers and some eurozone peers. Before the pandemic outbreak all mentioned papers were below 1.0% with Serbia and Greece being the last one to reach that magic level. When selling pressure started in the beginning of March spreads versus benchmark started to widen as it’s the case with any minor risk-off event but Italian and Greek bonds took the strongest hit as investors became aware of economic damage. However, ECB came to the rescue and pushed yields to the South. On the other side, EUR Eurobonds issued by Croatia, Romania and CEE company didn’t have that “luck” to be eligible for PEPP, so yields continued to rise or at best stopped rising. To put things into perspective, look at chart 2. on which you could see spread between Croatia and Greece turning positive in the last two weeks. Most likely there will be some spillovers from QE but investors are waiting for some firm ground and to see clear picture, or at least clearer.

Source: Bloomberg, InterCapital

Source: Bloomberg, InterCapital