Recently a few regional banks issued their bonds and one term that has been making waves – MREL, standing for “Minimum Requirement for Own Funds and Eligible Liabilities.” It may sound complex but fear not. In this blog, we will break down the basics of MREL, shedding light on its importance for banks and the overall financial system.

The Pillars of Bank Resilience

At its core, MREL serves as a safety net for banks during times of financial distress. Think of it as a two-fold requirement that banks must meet: having enough of their own funds and maintaining eligible liabilities that can absorb losses. These twin pillars work together to ensure banks can bounce back without relying on taxpayer bailouts. In the simplest terms, MREL is a regulatory measure saying that banks need to have collateral in case everything goes south.

- Own Funds: The Sturdy Foundation

First, let’s talk about own funds. These are the financial cushions that banks create to weather unexpected losses and sustain their operations. We’re not talking about just any funds here – we’re referring to the strong and resilient ones. Common equity tier 1 capital and additional tier 1 capital are the superheroes of own funds, known for their ability to absorb losses like champs.

- Eligible Liabilities: The Flexible Safety Net

Now, let’s shift our focus to eligible liabilities. These are the debt instruments issued by banks that can come to the rescue in a resolution scenario. Picture them as a safety net that banks can rely on when things get tough. These liabilities, such as specific types of senior unsecured debt and subordinated debt, can be converted into equity or written down if the bank faces insurmountable difficulties. Therefore, those debt instruments are cheaper than financing pure capital and can even be considered straightforward “cheap” – again, especially compared to equity.

One size does not fit all when it comes to MREL. Each bank’s requirements are tailor-made, considering factors like size, complexity, business model, and risk profile. This individualized approach ensures that banks maintain an appropriate level of resilience. The calculation of MREL is a collaborative effort between the bank, the resolution authority, and the central bank, all working together to set realistic targets.

Complying with MREL is not just a box-ticking exercise. Banks failing to meet their targets face serious repercussions. Regulatory sanctions, such as limitations on dividends, bonuses, and distributions, come into play. Moreover, resolution authorities may step in to ensure banks take necessary actions, like raising capital or issuing eligible liabilities, to bridge any gaps.

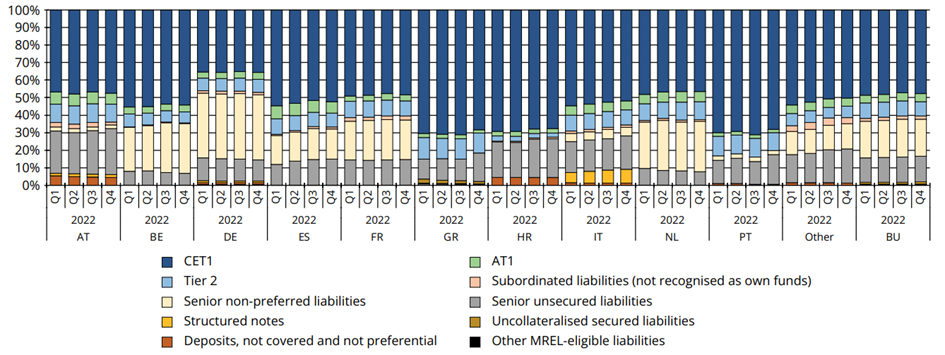

MREL development during Q4 2022

The average MREL target for banks under all strategies and tools rose compared to Q3 2022. Overall, the level of own funds and eligible liabilities (MREL resources) remained broadly stable compared to the previous quarter, while being slightly higher compared to Q4 2022. Also, the composition of MREL instruments remained broadly stable compared to the previous quarter and the previous year. However, the share of senior unsecured liabilities increased as a result of the issuance activity during the quarter.

We note that senior unsecured liabilities accounted for 15% of the overall MREL resources, while the share of senior non-preferred liabilities amounted to 21% of the total. Finally, it should be emphasized that non-covered non-preferred deposits continue to account for <1% of total MREL resources. Nothing major occurred in this category, which should offer some reinsurance.

Regarding maturity, almost 50% of total MREL resources are of a perpetual nature, while 40% with residual maturity between two 2 and 10 years.

MREL composition by country

Source: SRB Publication May 2023, InterCapital Research

MREL is an essential part of a broader regulatory framework designed to bolster the stability of the banking sector. It works hand in hand with capital adequacy requirements, liquidity standards, and stress testing. These regulations collectively strengthen banks, inspire investor confidence, and safeguard the wider economy from the risks associated with bank failures.

To sum up, MREL’s regulatory framework ensures banks have the necessary tools to weather storms and recover without resorting to public funds! By maintaining a robust level of own funds and eligible liabilities, banks contribute to a resilient financial system that can stand firm in the face of challenges. So, the next time you come across MREL, remember the two pillars: own funds and eligible liabilities.