Just three weeks after the signing of the MOU between the US and Iran, we have seen the ceasefire fail, with Iran firing at shipping in the SOH, and the US responding with strikes inside Iranian territory. It was, by any reasonable definition, a re-escalation of the largest oil-supply disruption in modern history.

West Texas Intermediate initially rose 4.4% to around $73.50, while Brent settled near $78. For context, the first Hormuz shock earlier this year had pushed crude above $120. The renewed conflict barely registered in the barrel this time.

The bond market had a more serious reaction. The 10-year yield climbed roughly ten basis points across two sessions to about 4.6%, back at levels last seen in May. A similar reaction was seen in German Bunds, who once again broke 3%, almost reaching 3.1%.

A crude move that couldn’t break $74 was still enough to send yields back to highs. If you were watching only WTI or Brent, the two numbers that lead every energy segment and anchor every news story, you would have concluded that not much happened.

But the real story is somewhere else. While crude has retraced significantly from the peak of the conflict, refined product prices have refused to follow.

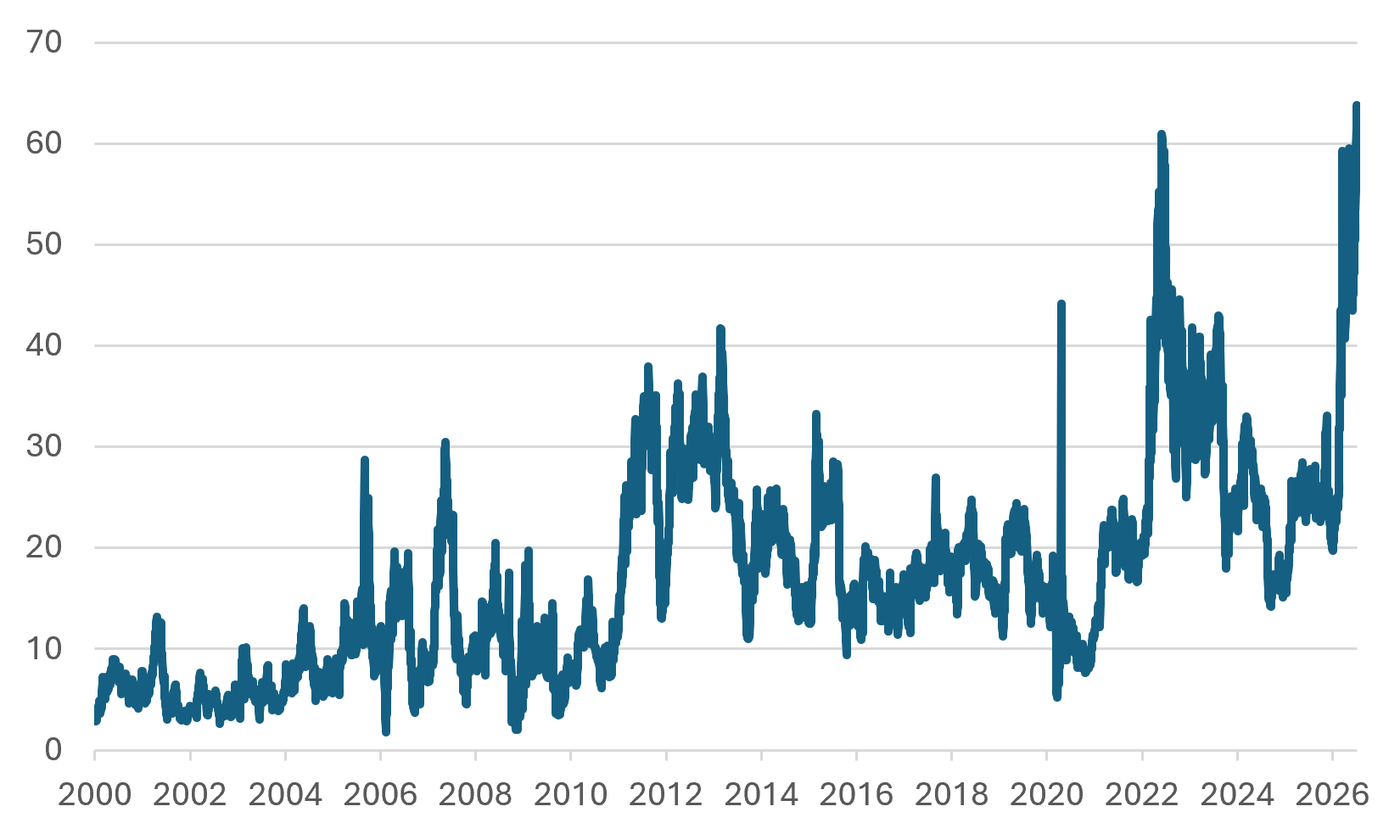

You can see this easily by observing crack spreads, the difference between what a refiner pays for crude and what it earns selling the products. A normal “healthy” 3-2-1 crack spread runs 10-20 USD per barrel; while anything above $30 signals stress. In March 2026 it hit $55.78, territory historically reserved for Hurricane Katrina, the 2008 aftermath, and the 2022 Russia-Ukraine shock. Months later, with crude having cooled, the crack is topping $65.

Nymex First Month 321 Crack Index

Source: Bloomberg, InterCapital

When an input and its output stop moving together, the correlation itself becomes the story, and right now, crude is falling while products stay stubbornly, painfully high. It is obvious why this is a much larger problem than crude itself. Products feed more directly into inflation because they are the prices actually paid by consumers and businesses, whereas crude oil is an intermediate input whose price is filtered through refining costs, taxes, transportation, margins, and regional supply-demand dynamics before affecting final price.

The University of Michigan’s year-ahead expectation was 4.6% in June, down slightlyfrom 4.8% but far above the 3.4% reading from February, before the conflict began.

The link between crude and products has already been weakening up to the conflict. The EIA’s own accounting is the cleanest proof. Over the previous decade, the crude oil used at US refineries accounted for a little more than half of the retail gasoline price, on average. For 2026 and 2027, the EIA now expects crude’s contribution to fall below 45%.

The mechanism behind the decoupling is a lag plus a ceiling. Product prices follow crude with a one-to-three-week delay, so a sudden crude move opens a temporary margin window refiners capture. But the more durable driver is capacity: US refineries have been running flat-out, at near 100% utilization. There is essentially no spare throughput to convert extra crude into extra fuel. That single fact is why a crude release, or a crude glut, does not automatically become cheaper gasoline. The bottleneck isn’t barrels of oil. It’s the ability to process them.

Refining shift

When Hormuz choked off Middle Eastern jet fuel and diesel, and Ukrainian drones took out swaths of Russian refining, the margins on middle distillates blew out. In March, the jet fuel crack peaked near $74 a barrel while gasoline sat around $35, a gap of more than 40.

Refiners, being rational, did the obvious thing: they reconfigured the barrel to make the product that paid best.

The reallocation was historic. US jet fuel production crossed 2 million barrels per day on a four-week average for the first time on record in early May, and stayed above it for four straight weeks, another first. To get there, refiners robbed the rest of the barrel. By April, national jet yields hit a record 12.5% while gasoline yields sank to 43.5%, the lowest since the pandemic. Gasoline’s share of combined gasoline-diesel-jet output slid toward 50%.

It is a bidding war between products for space in the barrel. Gasoline wins one round, then jet raises the stakes and takes the yield back. And it compounds seasonally: summer gasoline requires morecrude per gallon than winter blends, so any swing back toward gasoline for the driving season must be stolen from jet and diesel, meaning one product’s relief is another’s squeeze. Global refiners note the easy optimization gains are largely exhausted, and as attention turns to winter diesel from late in the third quarter, capacity will get pulled toward distillate again. The squeeze doesn’t end. It rotates.

Inventory evidence

If crude and products had truly decoupled, you’d expect their inventories to move in opposite directions. In the week ending July 3, they did exactly that, in the same report.

Crude inventories rose for the first time in eleven weeks, up 3.0 million barrels, all the while gasoline stocks fell to their lowest seasonal level since 2012. Distillate stocks slumped 5.0 million barrels to a four-year low, roughly 12% under the five-year average.

And the diesel tightness isn’t purely a war artifact. US distillate inventories fell 17% in the first half of 2025, nearly double the normal seasonal draw, driven partly by permanent refinery closures. Seven major US refineries have shut or converted since 2019, removing more than 1.2 million barrels per day of processing capacity for good. The geopolitical shock landed on top of a structural, multi-year erosion of the country’s ability to make fuel.

Export bans

Russia banned diesel exports outright in early July, extending an earlier partial ban to producers, after Ukrainian drone strikes disabled, by some estimates, more than 40% of its refining capacity. Russia supplied roughly 11% of the world’s diesel last year. Its ban is a global product-supply shock stacked directly on the Hormuz one.

In the United States, the mirror image is playing out as debate. Legislation to ban gasoline exports during high-price periods has been proposed, and while the administration says it has no plan to restrict exports, we expect the idea to gain traction if pump prices continue climbing.

The reserve built for the wrong war

Which brings us to the deepest structural point: the United States built an enormous strategic buffer for a problem that has largely stopped being the problem.

The Strategic Petroleum Reserve holds crude, hundreds of millions of barrels, more than a month of national crude consumption. It is a magnificent tool for a 1970s-style shock: an embargo, a blockade, a field shut in, anything that cuts off the input.

A crude reserve cannot fix a refining-capacity shock. When refineries are already maxed out, adding crude to the market produces no additional fuel, there is nowhere to process it. The danger, if a refinery goes down, is not crude, it’s literally jet fuel, gasoline, and diesel.

What to watch

The takeaway isn’t that crude no longer matters. It still sets roughly 45% of the pump price, and a genuine crude-availability shock would still bite. The takeaway is narrower and more useful: during supply-side shocks, and we currently have two independent ones stacking, Hormuz and the Russian refinery war, the crude-product link reliably breaks, and the barrel becomes a bad proxy for inflation.

When that happens, the honest dashboard is not WTI or Brent. It’s the crack spreads (are refiners being paid to make fuel, and which fuel?), product inventories (gasoline at 2012 lows, diesel at four-year lows), refinery utilization and yields (move toward jet), and the forward-looking financial gauges.