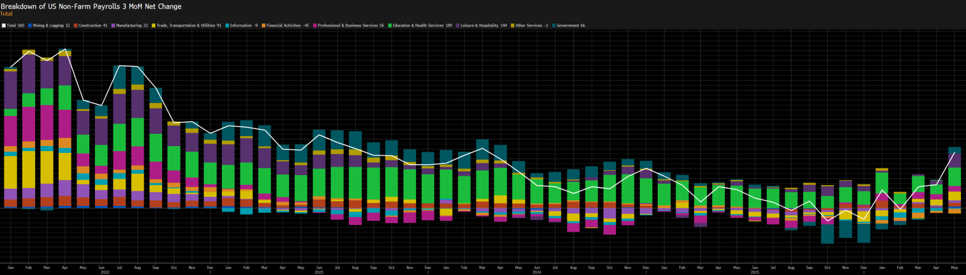

Despite the uncertainty around tariffs and elevated oil prices, US job growth remains strong and points to a reacceleration of the economy. The non-farm payrolls data released on Friday, June 5th came in well above expectations, signaling far stronger employment growth than previously thought and pushing yields higher particularly at the front end, with the market now pricing in two rate hikes over the next 12 months.

US non-farm payrolls printed at 178k versus a consensus of 65k, lifting the 2-year US Treasury yield to 4.15%, with further upside pressure as renewed hostilities between Iran, the US, and Israel flared up over the weekend. Strategic crude and refined-product reserves are being drawn down rapidly, with several analyses pointing to operational storage minimums potentially being reached as early as August or September. The situation continues to deteriorate as a deal with Iran looks increasingly remote. Both geopolitical risk and a healthy labor market keep pushing yields higher over time, driven by inflationary pressures and the potential for wage gains amid resilient job openings (JOLTS).

The first Fed meeting on June 17th will reveal how Kevin Warsh intends to shape policy. Initially, Warsh struck a dovish tone on short-term rates, favoring no change or a modest cutting bias, while leaving the door open to QT. Given the significant inflationary pressures, however, too many variables remain in play, and his first meeting will be pivotal for the predictability of monetary policy going forward. Fed communication may also evolve, with officials potentially offering less forward guidance. Many unknowns should be clarified in the near term. The pricing of rate hikes may create an opportunity to go long the 2-year US Treasury, but buying the long end could prove the better trade as the curve continues to flatten and front-end rates stay elevated. Should hikes materialize, the narrative could shift toward recession à supportive of long-term yields (the 30-year is currently just above 5%). On balance, buying longer-dated bonds looks like the more attractive opportunity given the uncertainty around Warsh’s debut, where he could surprise a market that broadly expects steepening (long 2Y on cuts, short 30Y on QT). Ultimately, the economy is far more than the S&P 500, whose volatility remains suppressed as earnings boom.

In the event of a deal with Iran, the calculus changes entirely: the 2-year US Treasury — along with the German Schatz — becomes the best long idea. Long-term yields, meanwhile, remain under constant pressure from rising Japanese bond yields, which have climbed steadily for the past several years as capital repatriation grows increasingly attractive relative to foreign bonds and equities.

The setup heading into the June 17th meeting is defined by competing forces: a resilient labor market and persistent oil-driven inflation argue for higher yields, while the risk of a policy-induced slowdown and an eventual Iran resolution argue the other way. With Warsh’s intentions still unclear and consensus leaning toward steepening, the asymmetry favors caution over conviction at the front end. Buying the long end offers the cleaner risk-reward in the current environment, while keeping the 2-year — and the German Schatz — ready as the primary long should a deal emerge. Flexibility, not a fixed view, is the right posture here.

Source: Bloomberg, Intercapital