Bitcoin’s demand story in 2024 was dominated by ETF inflows. In 2025, corporate treasury buying arose along ETFs. In 2026, STRC or “Stretch” became the dominant source of marginal demand, a perpetual preferred stock issued by Strategy. For Bitcoin traders, STRC’s price relative to $100 has recently become single most important signal for near-term flows. For STRC holders, the question is simpler: how long can an 11.50% yield on a Bitcoin-backed credit instrument hold together before rates, sentiment, credit risk or the issuance cap forces a repricing?

STRC has been listed on Nasdaq since July 2025. It pays a variable monthly cash dividend – currently 11.50% annualized – on a $100 par value. The rate resets monthly in 0.25% increments to keep the price near par. Per Strategy’s SEC filing, the adjustment framework is rules-based: a monthly VWAP below $99 triggers a recommended 25bps hike; below $95, a 50bps or larger increase; above $101, a rate cut. The framework is non-binding – Strategy may change or suspend it at any time in its sole discretion. The rate has been raised seven consecutive times from 9% at launch; it has never been cut. Strategy takes the proceeds and buys spot Bitcoin. Also, Strategy retains the right to redeem STRC at $101 plus accrued dividends, capping holder upside. A “clean-up redemption” is permitted if outstanding shares fall below 25% of total ever issued. In practice, this gives Strategy an exit valve in both directions: if rates fall and STRC trades above par, the company can retire expensive obligations at $101 rather than continue paying an elevated dividend. In a stress scenario where STRC trades far below par, Strategy could buy shares on the open market at a discount, and once outstanding shares drop below the 25% threshold, force-redeem the remainder at par, retiring the obligation cheaply while cleaning the balance sheet, while secondary market sellers bear all the losses.

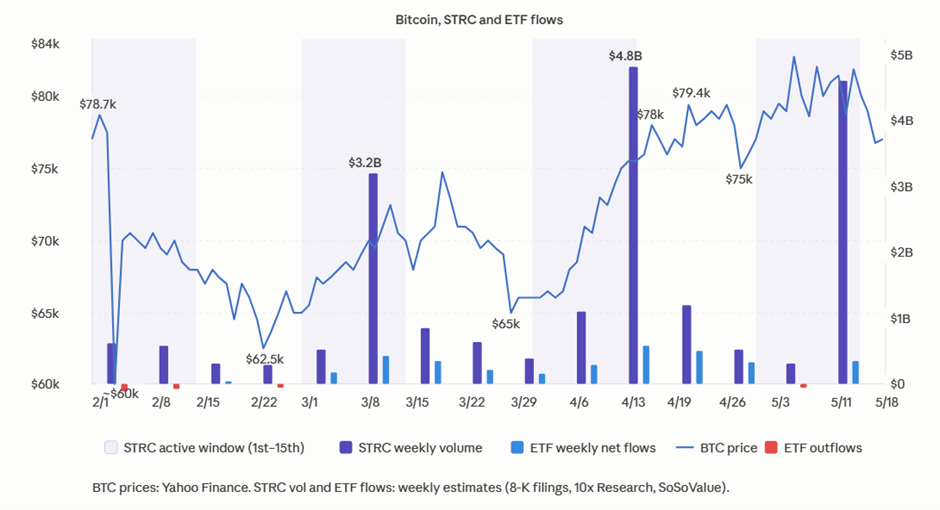

The ex-dividend date falls on the 15th. Investors accumulate STRC beforehand, pushing the price toward $100 and activating Strategy’s ATM. After the ex-date, demand fades, STRC drifts below par, and issuance stops. ~80% of STRC holders are retail, per CEO Phong Le, a base more prone to ex-date clustering and drawdown exits than institutional holders. Strategy proposed a semi-monthly dividend amendment (shareholder vote June 8th) aims to dampen this cyclicality by splitting one concentrated window into two.

STRC is perpetual, no maturity, no principal repayment. The only exit is the secondary market. In a liquidity crunch, that bid may not exist near par. The dividend has no floor – Strategy can cut it as easily as raise it. During the Q1 2026 earnings call, Saylor stated the company would likely sell Bitcoin to fund dividends, framing it as a signaling exercise. Total annual obligations across all preferred series and debt stand at roughly $1.5 billion (per CoinDesk), translating to ~$80–90 million per month – or approximately 0.18% of holdings monthly if funded through BTC sales. Saylor argued this is sustainable if Bitcoin appreciates above a 2.3% annual breakeven rate.

The credit behind STRC is Strategy’s balance sheet: 818,869 BTC (cost basis $61.8 billion, market value ~$66 billion), $2.25 billion in cash reserves, and ~$490 million in annualized software revenue – against ~$1.5 billion in total annual obligations across all preferred series and debt. On the Q1 2026 earnings call, Saylor stated the company would likely sell Bitcoin to fund dividends, estimating ~0.18% of holdings monthly, sustainable above a 2.3% annual BTC appreciation breakeven. The scenario math shows how risks compound. Today the market accepts ~700bps over risk-free rates given $66 billion in BTC coverage. A 20% drawdown to ~$65,000 pushes holdings below cost basis (~$53 billion), materially weakening the credit. High-yield preferreds in similar stress have historically repriced 200–400bps wider; at 14% required yield, STRC trades near $82. Each percentage point hike adds ~$83 million in annual cost. A 40% drawdown to ~$49,000 puts holdings $21.7 billion underwater, entering territory where dividend sustainability is in question and the reflexive loop activates: STRC breaks par, the ATM stops, Strategy’s buying disappears, removing Bitcoin’s marginal bid, deepening the drawdown. Higher risk-free rates/rate hike cycle could compound the pressure – mechanically raising the yield STRC must offer while simultaneously pressuring Bitcoin as the opportunity cost of holding a non-yielding asset rises. A dual squeeze: the floor moves up and the credit spread widens on top.

For holders caught below par, recovery is slow. The dividend pays $11.50/year on par regardless of market price – at $80, full principal recovery through dividends takes ~8.7 years. If Strategy cuts to 9%, that extends to ~11.1 years, and the cut itself depresses the price further. There is no maturity guaranteeing a return to $100, or a guarantee that Strategy would keep paying during stress. The fundamental question for holders is whether 11.50% compensates for infinite duration, single-asset credit risk, rate sensitivity, pro-cyclical funding mechanics, and an approaching $28.3 billion issuance cap – all in an instrument that has existed for less than a year.