Three weeks ago, Trump signed five Presidential Determinations under Section 303 of the Defense Production Act, one of which classifies transformers, transmission lines, substations, high-voltage circuit breakers and power electronics (essentially Končar Group’s products) as resources essential to U.S. national security. A week later, the EUR 50 billion Pantheon project was announced – a gigawatt-scale AI data center to be built in Topusko. On top of that, Končar Group companies delivered strong Q1 results across the board, so it is worth asking how the Group can position itself on both sides of the Atlantic to capture as much of these tailwinds as possible.

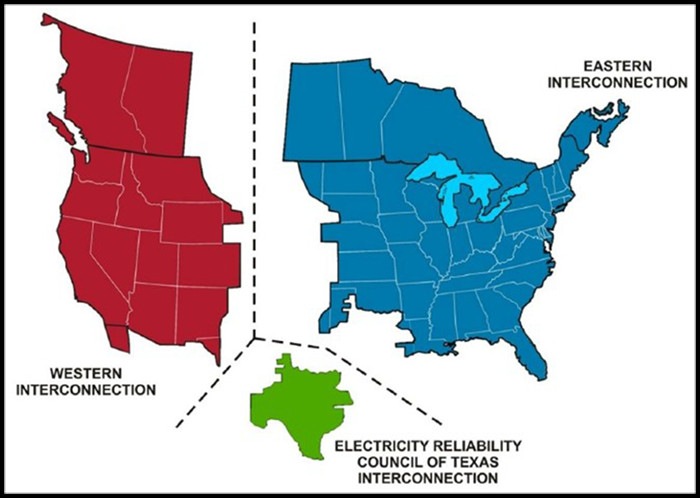

Starting with the US market, we first have to understand why and how the US grid is structurally vulnerable. The US does not have a single national power grid – it has three near-independent synchronous grids – the Eastern Interconnection (east of the Rockies, roughly 700 GW of generating capacity), the Western Interconnection (Rockies to the Pacific, roughly 250 GW), and the Electric Reliability Council of Texas (ERCOT), which serves 90% of Texas as a separate island.

The three major interconnections of the US electric power grid

Source: North American Electric Reliability Corporation, InterCapital Research

Texas deliberately built its grid to avoid federal jurisdiction, which gave it its own market design, faster generation build-out, and no federally imposed capacity requirements. Winter Storm Uri in February 2021 – when ERCOT came within minutes of total collapse and could draw only ~800 MW from neighboring states – was the most expensive demonstration yet of what that trade-off actually costs. The isolation problem is now compounded by the surge in load from data centers and crypto miners.

The Eastern and Western Interconnections are joined along a “seam” running roughly along the Wyoming-Nebraska border, with seven back-to-back HVDC stations that allow a transfer of at most 1,320 MW between grids whose combined capacity is around 950,000 MW. Relative to their size, the two are effectively walled off from each other. Studies consistently put the benefit-cost ratio of strengthening the seam at 2.5 to 2.9, against an estimated capex of roughly USD 50bn for a true US macrogrid.

On top of that, transformer lead times have multiplied – large power transformers now run three and a half years from order to delivery – and blackout frequency could rise sharply without meaningful capacity and grid expansion.

Building on earlier programs such as the DOE’s Speed to Power initiative and SPARK funding, Trump signed five determinations under Section 303 of the DPA, covering: grid infrastructure and supply chain capacity; the development and deployment of large-scale energy infrastructure; coal supply chains and baseload generation; natural gas transmission, processing and LNG capacity; and domestic petroleum production, refining and logistics.

The most relevant determination for Končar, and the one at the center of today’s topic, formally classifies the following as national-defense resources: transformers, transmission lines and conductors, substations, high-voltage circuit breakers, power control electronics, protective relay systems, capacitor banks, and electrical core steel, along with related raw materials and tools. The list reads almost line-for-line like the Group’s consolidated product portfolio.

That said, the DPA fund is small relative to the need (USD 323m for 2026) making it more a signal of intent than capital. Also, Biden invoked the DPA specifically for transformers back in June 2022, and four years on, lead times have barely shortened. Therefore, the DPA alone is unlikely to fix a system that structurally lacks production capacity, qualified labor, and grain-oriented electrical steel.

What remains uncertain is how the grid problem will be tackled, and on what timeframe, but not whether it will be tackled at all. The energy bottleneck has to be resolved if the US wants to keep building out AI capacity while protecting its strategic interests.

Many of the key beneficiaries are likely to be domestic players, in line with the Trump administration’s protectionist stance. Across transmission and advanced conductors (PLPC, Valmont Industries), substations and HV circuit breakers (Powell Industries), transformers (SPX Technologies, Canadian producer Hammond Power Solutions), and electrical core steel (Cleveland-Cliffs), all stand to benefit from this wave of investment. Beyond the North American names, global players like Hitachi Energy, Siemens Energy, Mitsubishi Electric and Hyundai Electric are bound to take their share, and it is increasingly plausible that Končar joins them, in relatively smaller amounts but still meaningful upside.

Končar Group and GRID ETF price development (% change since 1 Jan 2025)

Source: Bloomberg, InterCapital Research

At present, the Group’s primary exposure to the US market is KPT, a non-consolidated JV with Siemens Energy, while the Americas and Australia segment combined has historically accounted for only 2–3% of sales. The clearest signal that Končar is taking concrete steps towards the US was last year’s technical partnership with Sanmina Corporation, which includes the co-design of custom medium-voltage, distribution and instrument transformers, as well as switchgear. The move points Končar in the right direction and gives it first-hand visibility on further US opportunities, but the financial impact remains immaterial. So, the partnership is best read as a market-entry vehicle rather than a revenue stream.

We have spent a lot of time on the US, but on this side of the Atlantic the bottlenecks and investment needs are much the same. The Pantheon data center in Topusko stole the headlines in the last couple of weeks, but the largest investment project in Croatia’s history still has to deliver more detail and firmer commitments before the effects on the local economy and the companies involved in the buildout can be properly priced in. The 1 GW capacity is enormous by European standards, let alone Croatian ones, and the energy constraints alone mandate significant investment in supporting infrastructure. To that end, Končar Group and Dalekovod have both announced signing a Letter of Intent for the construction of the energy infrastructure segment and a portion of the data center works. New substations, 280 km of new transmission lines, transformer equipment and other key electrical components are expected to be in scope – a multi-hundred-million-euro contract that could become a flagship project for several Končar Group companies, further building their credentials and opening new doors. The US counterparty, Pantheon Atlas LLC, adds another name to the list of US partners.

Končar Group Q1 2026 vs Q1 2025 headline financials (EURm)

Source: Končar Group, InterCapital Research

The Q1 headline numbers show Končar doing the right things, in the right place, at the right time, successfully riding the electrification mega trend. The targeted 70/30 split between export and domestic sales, and the primary focus on EU markets, are unlikely to shift materially – but a real and growing chance to benefit from US grid capex, alongside Middle Eastern exposure that is currently out of the spotlight due to regional conflicts, leaves Končar in a strong position and reinforces the case that Croatian products, industry, people and innovation are competing on a global stage.