Gold is one of those assets that you can find in almost every portfolio that considers itself a well-diversified one. It usually gets bid when everything else is selling and has a really low correlation with the rest of the widely traded assets. However, when the famous diversifier decides to act like the equity market in times of crisis, it is a good time to ask: did something fundamentally change, or are we looking at a one-off event?

To understand March, we need to go back further. Gold, alongside all other metals, was the positive story of 2025, rising more than 65% in price, crushing all record highs. This holds true by any measure, including inflation-adjusted terms. The rally started more than a year before and just kept going. Central banks were buying aggressively and accelerating their purchases. Poland alone added 102 tonnes, China’s PBOC reported 14 consecutive months of purchases, and Chinese retail investors poured a record $15.5bn into gold ETFs during the year. Confidence in US assets was falling, and the debasement trade was a strong narrative throughout the year, with many convinced that metals were the only protection against money supply expansion and a rising debt-to-GDP ratio.

Gold price chart (last two years, in USD)

Source: Bloomberg, InterCapital

Near year end, things turned hysterical. Metals were rising in high single-digit and low double-digit percentages daily. Dealers were reportedly reluctant to buy physical metal. The Shanghai premium soared. It was classical retail FOMO behaviour. The first major liquidation came on January 30th, when brokers raised margin requirements for gold and silver futures, triggering a wave of forced selling. Gold fell the least, but even its biggest drawdown was “only” 21% from the highs above $5,600/oz.

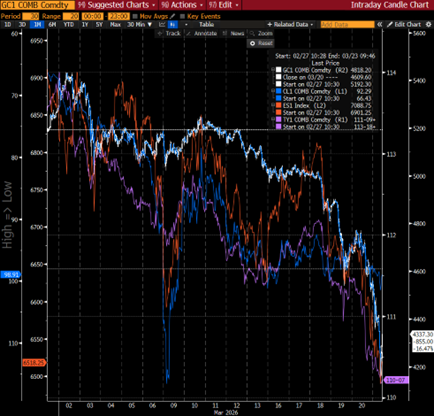

In February, as geopolitical risks began stacking up, gold did catch an initial safe-haven bid, almost retesting its previous highs, and spiked over 1% when hostilities began. But once the Hormuz crisis flared up, gold fell harder than equities and bonds. The fall continued throughout March, with gold showing high positive correlation to equity and bond markets and a strongly negative correlation to crude oil. It was a classic “correlations go to 1” pattern we see in most crises, where liquidity stress overwhelms all other factors. On most days, the market ran just two trades: long crude oil and short everything else, or the reverse.

Gold was a convenient asset to sell for the managers who had ridden the rally up. According to the World Gold Council, North American ETF holders alone recorded $13bn in outflows in March, the largest monthly outflow on record, ending a nine-month streak of inflows. A rapid repricing of interest rate expectations, from multiple Fed cuts to potential hikes, driven by inflation fears, made things worse. Higher real yields reduce gold’s appeal. The final blow came from systematic funds and CTAs forced to sell once the trend flipped negative. Together, these forces pushed the price probably further down than the fundamentals warranted.

March in one chart: long oil, short everything else (crude oil scale inverted)

Source: Bloomberg, InterCapital

March 23rd marked the local bottom, with gold touching below $4,200/oz intraday. Since then, it has recovered steadily, supported by improving news from the Middle East and a reversal of several negative March factors. COMEX open interest dropped 33% from January peak, indicating the speculative excess that had built up during 2025 has been largely purged. The remaining positions belong to longer-duration holders who are not sellers at current prices, some even bought the dip with Asian gold ETFs adding $2bn during March. Once again, ETF flows turned positive across all regions, central banks are still buying, and even though inflation fears have returned, central banks appear reluctant to raise rates.

Both the bull and bear cases remain open. The price reset during the crisis was real, but anyone who bought gold in 2025 is still in the green, up at least 10% even from 2025’s highs. The question worth watching isn’t price levels: it’s whether gold continues to behave as a risk asset or reclaims its role as a risk-off anchor. March was a reminder that the answer is never permanent, at least in the short-term.