More than three weeks into the U.S.-Israeli joint venture war on Iran, or as Trump would put it – an excursion, there is one question hanging over every trading/portfolio-managing related question, and that is how long does this last? It was supposed to last three-to-four weeks, and it was ostensibly over two weeks ago according to Trump. But as it is becoming clearer every day, he is not the one solely deciding when it will end as the Iranians will have the final say whether they have inflicted enough damage to the U.S. and their allies to avenge the death of the former Supreme Leader. The answer to the question is an unwelcome one – nobody knows. And that uncertainty is the primary driver of the jumble across every asset-class right now.

There is a common denominator that currently influences virtually every asset-class, and that is the price of oil. Before the first strikes landed on February 28, Brent crude was sitting near $70 a barrel. As of the previous week, it has settled comfortably above $105. Dubai crude, the benchmark most exposed to the Gulf transit, briefly pierced $166. The Strait of Hormuz is effectively shut down for normal commercial traffic. Cheap Iranian drones and mines do not need to physically blockade the waterway, the mere threat of them is enough to reroute tankers and keep insurance premiums so high that travelling the Strait becomes economically unviable.

The problem is not just the current price. It is the total absence of clarity when the production and the ability to traverse the Strait freely will normalize. Production infrastructure across the Gulf has been hit. Saudi Aramco’s Ras Tanura facility is offline, Qatar declared force majeure on its LNG exports and the aftermath of the recent strikes showed that their exports would be approximately 15% lower for three to five years, and Iraqi and Kuwaiti fields are being forced to shut in as storage fills up. Even if a ceasefire were announced tomorrow, restarting these operations could take weeks or months depending on the damage.

For consumers, the math is stark. Gasoline and diesel prices are surging. Every dollar spent at the pump is a dollar not spent elsewhere. Higher oil and gas prices will unavoidably increase the costs of food as fertilizers and transport costs will rise as their direct input costs climb. This will either lead to demand destruction as households will have to ration their spending or for those that refuse to cut back on their outlays, their savings (investments) will have to absorb the hit. Either way, the consumer is weaker coming out of this than going in.

Gold is an interesting case study in this episode. It is getting crushed even though inflation and geopolitical risks are ramping up, and equities are selling off. In practice, gold markets are governed by flows, not narratives. We are witnessing a typical deleveraging event where investors in need of cash, sell their most liquid holdings to raise it. A stronger dollar (a consequence of higher oil prices as everybody needs them to buy energy) and rising Treasury yields are compounding the pressure. With 10-year yields above 4.40% after previous week’s Fed presser, and another round of escalations this weekend, the opportunity cost of holding a zero-yield asset has increased meaningfully. If the war picture starts improving, gold will likely revert to all-time-high levels that were reached a couple of months ago.

Into this maelstrom walked Fed Chair Jerome Powell on Wednesday for what may be his penultimate press conference before his term ends, when he might stay on as a Governor. The Fed held rates as expected, but the tone was anything but dovish. Markets heard the message and interpreted the conference as rate cuts are off the table for the time being. Some economists are quietly beginning to whisper about hikes.

If Powell’s hawkishness was the appetizer, the ECB served the main course on Thursday. The European Central Bank held its deposit rate at 2.0%, but sources with direct knowledge of internal discussions told Reuters that policymakers may need to begin discussing rate hikes at the April 29–30 meeting and could tighten policy as early as June. The ECB’s own baseline projections assumed Brent at $81.30, a figure that sources described as hopelessly outdated with the actual price sitting above $110. Market pricing has shifted accordingly, April cut is fully priced in, and the total number of hikes sits north of 3 until year-end.

For now, markets are updating their assumptions in real time, as one analyst described it. Every headline is a potential inflection point. And until the fog of war lifts, every asset from crude oil to gold to the S&P 500 will continue to trade on the same binary question: does this end soon, or does it lead to prolonged and deep economic crisis? To paraphrase the immortal Jeremy Irons’s portrayal of John Tuld in Margin Call: “I’m here to guess what the music might do a week, a month, a year from now. And writing this blog post this morning, I’m afraid that I don’t hear – a – thing. Just… silence.”

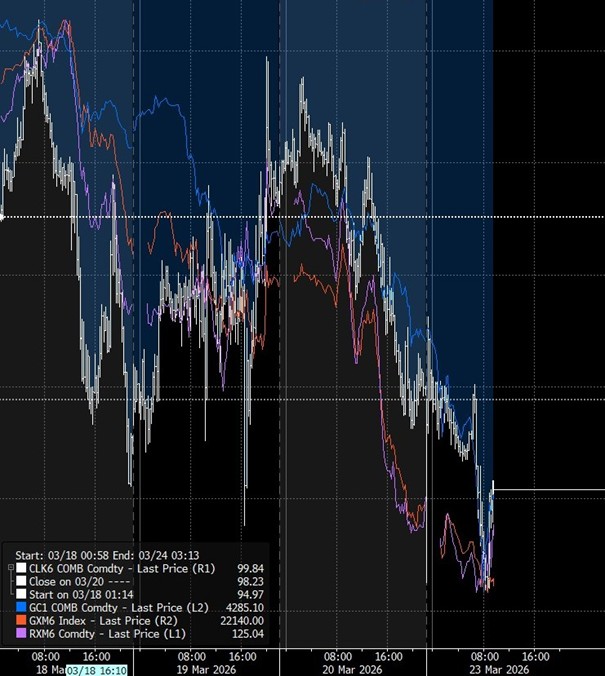

Cross-Asset Price Action (18-23 March 2026)

Source: InterCapital, Bloomberg