Before tackling today’s blog topic, bonds, we will first state the obvious. Over the weekend, the U.S. and Israel conducted a series of bombing campaigns aimed at eliminating Iranian leadership. Although early reports confirm that Iranian leader Ali Khamenei has been successfully eliminated, it remains to be seen whether the conflict will drag on and escalate further. As of this writing, WTI crude oil stands at $72, an increase of about five points from the previous close, while the U.S. dollar has strengthened and currently stands at 1.1705.

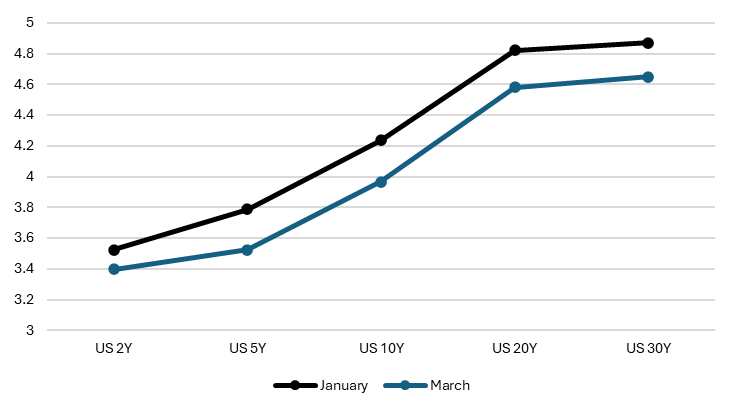

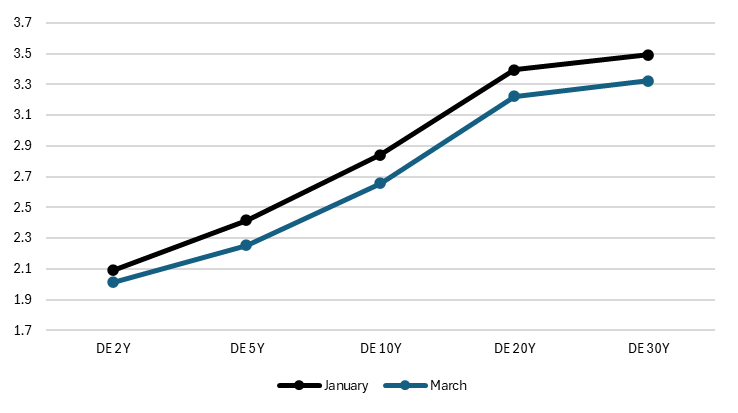

Now, on to the actual topic. Record bond issuance hit the market at the beginning of 2026, as EU countries sought to roll over existing debt and tap new tenors. Markets were positioned for Dutch pension fund flows and were increasingly betting on a steeper yield curve overall. The narrative supported this view: “fiscal spending will increase” and “countries will need to issue more debt on the back of defense spending.” However, the momentum did not last long. February arrived with a slow but steady curve flattening, forcing the market to reconsider its positioning. Currently, the Schatz (German 2Y) stands at 2.013%, while the Bund (German 10Y) is hovering around 2.656%. Overseas, the U.S. 2Y sits at 3.3974% and the 10Y at 3.9678%. In the figures below, we can see the difference between the respective yield curves in January and today. U.S. 10Y yields have tightened by 26 basis points, while their German counterpart has tightened by 18 basis points. The U.S. 2Y yield has tightened by 12 basis points, and the Schatz by 8 basis points.

US Yield Curve – Jan vs. Mar – (Selected Maturities)

Source: Bloomberg, InterCapital

German Yield Curve – Jan vs. Mar – (Selected Maturities)

Source: Bloomberg, InterCapital

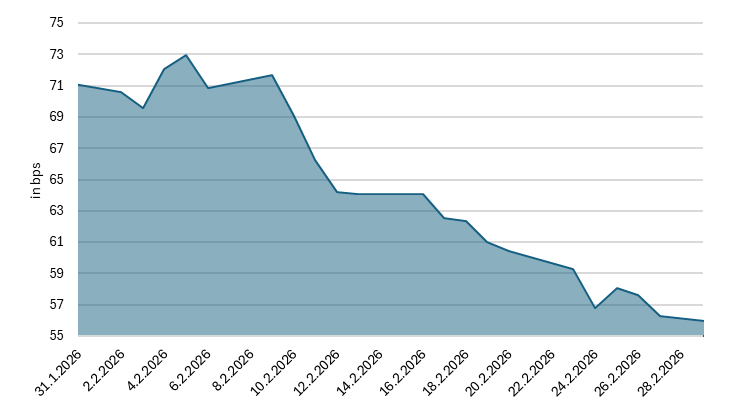

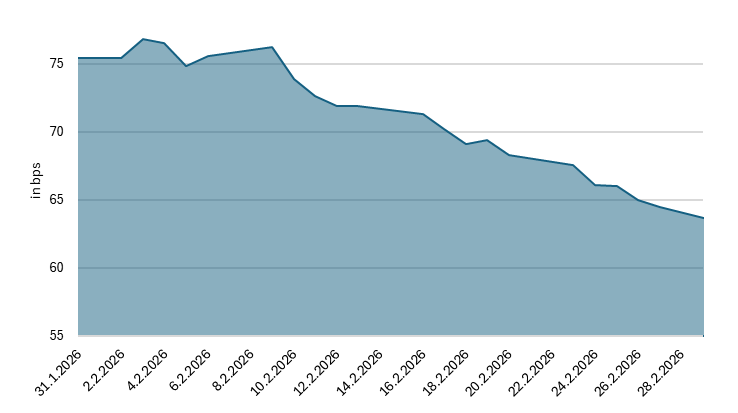

When we look at the spreads between the 2Y and 10Y tenors (as seen in the graphs below this paragraph), we can clearly see that longer-dated 10Y yields have fallen more than shorter-dated yields; that is, the spread has tightened. But why is this the case? Despite the persistent concerns about fiscal deficit in the U.S. (which is indeed a problem) and additional government borrowing in Germany, incoming data has been cooler than expected. U.S. CPI came in slightly below expectations at 2.4% YoY (0.2% MoM), compared to 2.7% the previous month, and preliminary Q4 GDP was reported at 1.4%, versus the 2.8% that had been forecast. Eurozone data continues to cool, and although there are some signs of a pickup in economic activity in Germany, we remain far from a fully-fledged economic turnaround. Even the concerns about abrupt Fed rate cuts once Mr Warsh takes office were not enough to reverse the trend.

US 10Y vs. 2Y Spread (bps)

Source: Bloomberg, InterCapital Research

German 10Y vs. 2Y Spread (bps)

Source: Bloomberg, InterCapital Research

Going forward, in the U.S., we will need to pay close attention to several factors. First, the question of Fed independence remains unresolved and will be a key issue until Mr Warsh is firmly in the driver’s seat. In this regard, a Supreme Court ruling in the case of Lisa Cook, if it favors the Trump administration, could introduce even more uncertainty about what the Fed might do this year. Finally, we will have to monitor how the data evolves. Are we moving toward a cooling economy, or will inflationary pressures reignite? In Germany, one key question remains: how quickly will we see a meaningful economic and industrial recovery?

On that note, this week we will be closely watching the Manufacturing PMIs on Monday (today). On Thursday, Jobless Claims will be released, while on Friday, we will receive Retail Sales, Non-Farm Payrolls, and the Unemployment Rate.