New Croatian paper is fairly valued at MS+55bps? We beg to differ – and we have numbers to back it up. It might take a bit of time, but the wall of bond liquidity will likely flip the SLOREP€-CROATIA€ spread back into positive. What about Balašević in this whole story? Well, to figure that out, continue reading this blog.

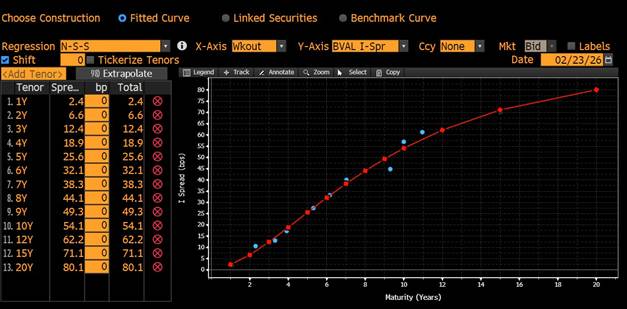

Following Slovenia, Poland, Hungary and Slovakia, Croatia finally tapped the international markets for a 2.0bn EUR placement of CROATI 3.25 02/25/2036€, a new 10Y benchmark that was placed at MS+55bps (99.597, 3.297% YTM). When the books opened Wednesday morning, the syndicate indicated MS+80bps, but investors quickly understood that the actual pricing was going to move far tighter than that. We estimated FV at MS+50-55bps, with a large caveat that will be discussed a bit further. Namely, the FV was calculated based on the CROATI€ curve that’s submitted below.

CROATI€ curve

Source: Bloomberg, InterCapital

If we use the CROATI€ curve as the starting point for our valuation, new CROATI 3.25 02/25/2036€ is a bit cheaper and is currently valued at some 2bps above the curve. From our understanding, domestic accounts were lacklustre on the auction, mostly because pension funds’ appetite was quite low since there wasn’t a pending Eurobond maturity this year whose proceeds would then be funnelled into new CROATI€ placement. The 9.0bn EUR orderbook (4.5x bid-to-cover) came from abroad, and it seems that foreign accounts couldn’t get enough of it. Nevertheless, the paper trades a bps wider compared to reoffer, mainly because the syndicated banks ended up with sizeable chunks of paper that they need to offload before the spread can tighten further. This morning, CROATI 3.25 02/25/2036€ is benefiting from a safe haven bid, but the spread is not moving down.

So why are we bullish on the paper? Because we were looking at the pricing based on the existing CROATI€ paper, while the comparison with similar countries paints a more rosy picture. Once the international bond placement was disclosed (that was early January), Street dealers froze their bids, and CROATI€ wasn’t following CEE€ or semi core countries once the yields started dropping. To get a glimpse of the situation, check out the spread between CROATI 4.0 06/14/2035€ and SLOREP 3.125 07/02/2035€ (submitted below).

Spread between CROATI 4.0 06/14/2035€ and SLOREP 3.125 07/02/2035€

Source: Bloomberg, InterCapital Research

Most of last year, the spread was positive, meaning that Slovenian paper was trading at higher yields compared to Croatian paper. Then in January 2026, the premium of Slovenian paper vanished without a trace – and even flipped into negative. Now, how did that happen? Take a closer look at the chart, and you will notice that the Slovenian yield felt the gravity of the German Bund, while the Croatian paper seemed a lot lazier to follow. We believe the laziness of Croatian paper came from dealers unwilling to add more CROATI€ on their positions in the anticipation of new placement.

Could the sudden reversal in the spread be explained by fundamental differences between the two countries? We beg to differ. Although the two countries have similar 2026 fiscal deficits, Slovenia has a pending general election on March 22nd and the frontrunner, Janez Janša, could expand Slovenian public spending a bit further (You have to win the election somehow). On the other hand, Croatia won’t be looking at the general election any time soon, even with the current reshuffling of the governing coalition.

In other words, the CROATI€ curve was frozen in time since the first disclosure about the new Eurobond and hence missed the first leg up of cash bond prices. With the domestic bid starting to get active, the PMs worksheets will start red-flagging the Croatian curve as cheap, and the spread will start to narrow down below Slovenian levels. The keyword is gradually.

The day following the bond placement (Thursday, 19th) marked the fifth anniversary of the famous Balkan songwriter Đorđe Balašević’s passing away. In his seminal piece, Nevena, Đole mentions the famous patient figures of inevitability (in original strpljivi prsti neminovnosti) – the same force that affected the life of song’s protagonist Sale Nađ would be the same force driving the CROATI€ spreads narrower. Patient fingers of inevitability.