Since S&P500 recently turned positive YTD, we decided to present you with an updated analysis of how correlated have been CROBEX and S&P500 since the beginning of the year.

If you have been following the Croatian and the US equity market since the beginning of the Covid-19 crisis, you might have seen certain similarities in the movement of CROBEX and S&P500. Therefore, we presented you already with a brief analysis of how correlated the movements are the movements of CROBEX and S&P and have concluded a solid correlation between the indices during the crisis.

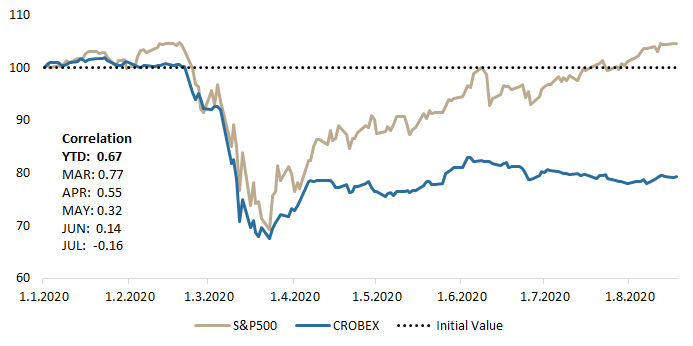

Today, we decided to revisit the analysis given that S&P500 recently turned positive YTD. Currently S&P500 is up 4.9% YTD, while CROBEX is still 20.6% down. There are many reasons for such a difference in performance between indices, but it is worth pointing out that technology companies which have benefited to some extent in this pandemic account for roughly one fifth of S&P500 (such as Microsoft, Amazon, Google etc.). Meanwhile, many CROBEX heavy weights were quite affected by the Covid-19 crisis.

YTD Performnace of CROBEX and S&P500

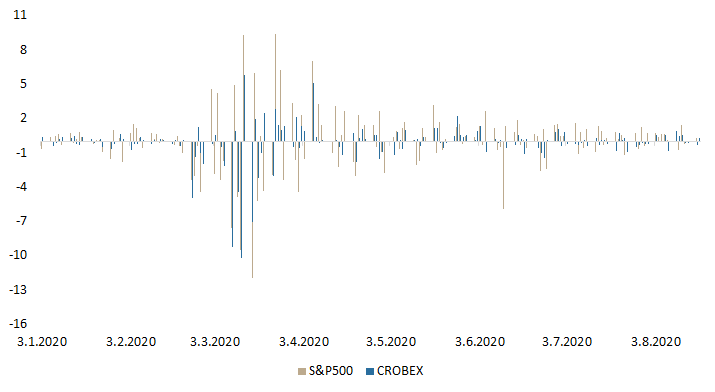

If we were to take a closer look at daily movements of the indices, one could have observed an interesting correlation during March and April, which is visible in the graph below. Since the Covid-19 outbreak, one can notice that almost every time in March and April when S&P500 recorded a sharp daily increase or decrease, the same movement of CROBEX was observed . This can be also confirmed when calculating the coefficient of correlation of YTD daily returns of both indices, which amounts to 0.67, showing a solid correlation between the movement of the indices. This has not been historically the case (to such extent) as the coefficient of correlation for the same parameters since 2015 amounts to 0.42, while since 2007 amounts to only 0.37.

Such a correlation could imply that since the outbreak of the Covid-19 crisis many investors in the Croatian equity market were not necessarily basing their investment decisions on fundamentals or the local news, but rather on the global sentiment. This would not surprise us as many fundamental parameters were and are still in a very unknown territory such as the end of the Covid crisis, or the impact on the macro picture across economies.

YTD Daily Change of CROBEX and S&P500 (%)

However, since than the situation has quite changed, which can be seen when looking solely at the correlation between the indices since May onwards (for each month individually).

To be specific the correlation between the indices in May amounted to 0.32, June amounted to 0.14, while in July it amounted to -0.16. Such figures show that the indices were not as correlated during the partial bounce back as they were during the drop. It is also worth noting that as more fundamental parameters become clear in the local market, it is reasonable to expect a lower correlation then the current (on the YTD basis).

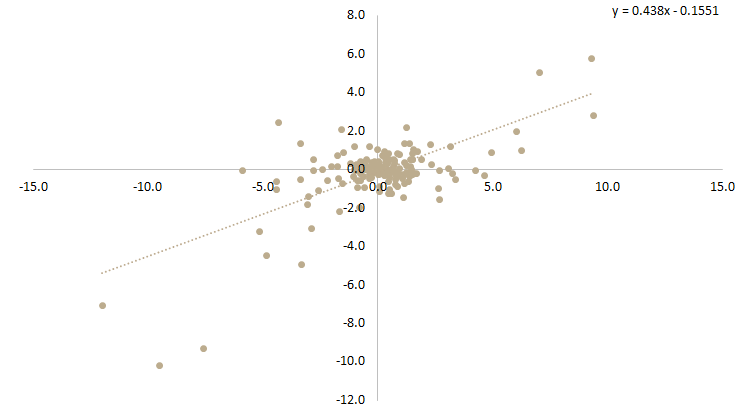

If we were to run a regression of YTD daily returns of CROBEX and S&P500, the slope of the regression gives us additional information of relative volatility of CROBEX. In the graph below, you can see that the slope of the regression amounts to 0.44 indicating that CROBEX has been roughly half as volatile as S&P500. So for example, an increase of 10% of the S&P500 would indicate a 4.4% increase of CROBEX.

Regression of YTD Daily Changes of CROBEX Against S&P500